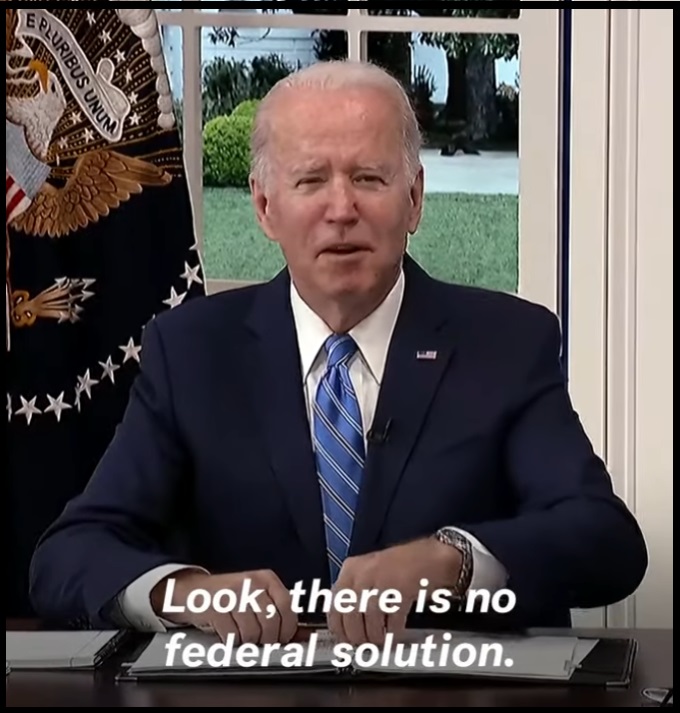

It’s worth paying attention to where and when Joe Biden is standing when he makes his ridiculous economic claims today about Russia being the cause of the energy policy from the White House.

Do not let it go unnoticed that it’s June, the last month of the second quarter for economic data. Do not let it pass your reference that Joe Biden is speaking from the Port of Los Angeles (POLA) as he spins his nonsense about the inflation, he alone is responsible for. And do not overlook the attendee mentioned in this subtle statement, “And, John, I can’t thank you. You’re — you’re the real deal. Anybody — well, I won’t get into — get you in trouble, but thanks for sticking up for me.”

Do not let it go unnoticed that it’s June, the last month of the second quarter for economic data. Do not let it pass your reference that Joe Biden is speaking from the Port of Los Angeles (POLA) as he spins his nonsense about the inflation, he alone is responsible for. And do not overlook the attendee mentioned in this subtle statement, “And, John, I can’t thank you. You’re — you’re the real deal. Anybody — well, I won’t get into — get you in trouble, but thanks for sticking up for me.”

“John” is the White House Port Envoy John D Porcari. A severely partisan former Obama official who was selected by Joe Biden to lead the fraudulent effort to improve supply chains when the White House was under assault in the fall of 2021. Porcari was the person who designed “operation hide the ships” to give the illusion of port efficiency improvement, and it is almost a certainty that it was Porcari who leveraged his influence with the POLA to hold back the December 2021 import data in order to try and improve the GDP statistics. {GO DEEP}

A recession is defined as two consecutive quarters with negative GDP growth. The first quarter of 2022 was -1.5% as detailed by the Bureau of Economic Analysis. That means if April, May and June 2022 are also negative GDP then we are factually in an economic recession. That makes this month, June 2022, critical for Joe Biden. The White House will do anything to avoid that label appearing on their economic policy when the reporting is released at the end of July.

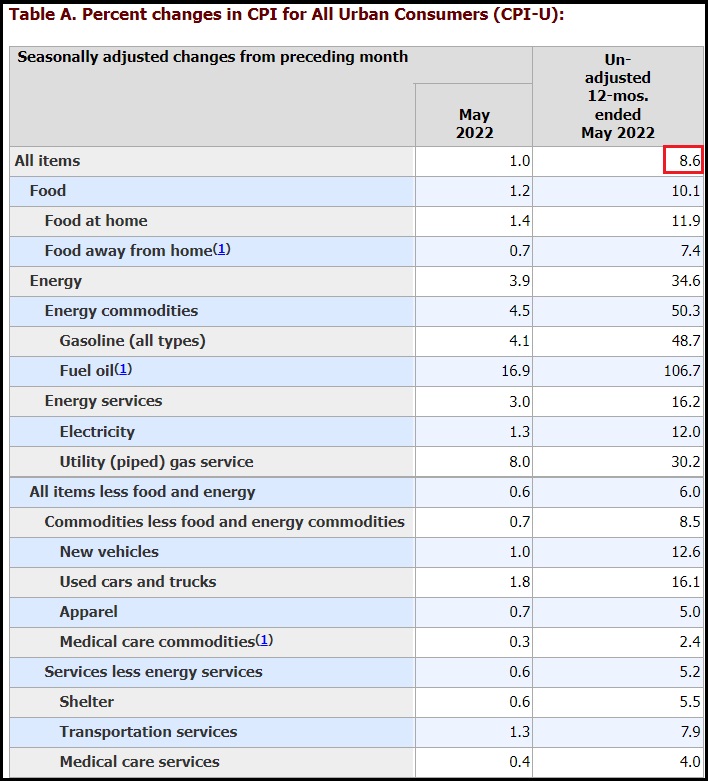

This month of inflation data is particularly important because it cycles through the May 2021 calendar comparison from last year when the first wave of massive inflation first triggered. The current year-over-year 8.6% rate of inflation now lands atop twelve months of massive increases in prices.

This month of inflation data is particularly important because it cycles through the May 2021 calendar comparison from last year when the first wave of massive inflation first triggered. The current year-over-year 8.6% rate of inflation now lands atop twelve months of massive increases in prices. On the front side of the justification, the people in control of the Biden administration, claim that current and future increases in energy prices are likely to do severe damage to the economy and the lives of all Americans. However, in the background of the issue, this is the ‘never let a crisis go to waste’ phase of an energy crisis the administration has intentionally created.

On the front side of the justification, the people in control of the Biden administration, claim that current and future increases in energy prices are likely to do severe damage to the economy and the lives of all Americans. However, in the background of the issue, this is the ‘never let a crisis go to waste’ phase of an energy crisis the administration has intentionally created.

Beyond all the obfuscation, denial and continual pretending, the reason for the gasoline shortages is related to this forcible shift in energy policy that is underway in Europe and the United States. It’s not a shortage of oil, it’s the new era where the Green New Deal is the policy priority. The people within the Biden administration do not care about the consequences, Biden is pushed in front of the camera as a useful idiot to take the blame.

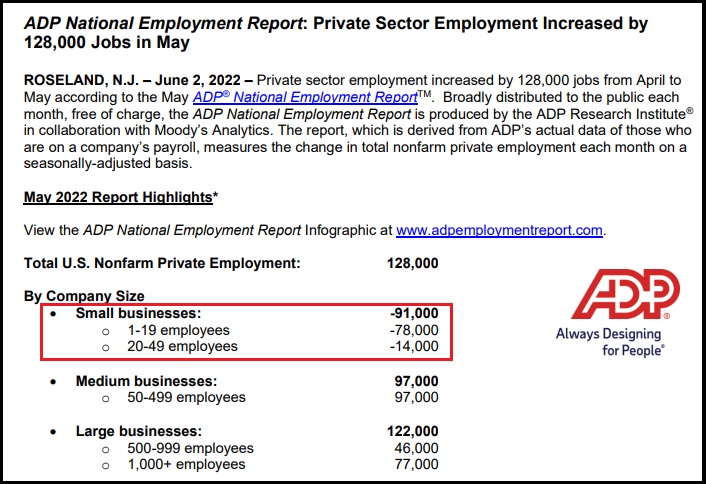

Beyond all the obfuscation, denial and continual pretending, the reason for the gasoline shortages is related to this forcible shift in energy policy that is underway in Europe and the United States. It’s not a shortage of oil, it’s the new era where the Green New Deal is the policy priority. The people within the Biden administration do not care about the consequences, Biden is pushed in front of the camera as a useful idiot to take the blame. Keep in mind the data is national & skewed toward low estimations as represented by (+).

Keep in mind the data is national & skewed toward low estimations as represented by (+).