Officials in the state of Texas are worried the emergency measures taken Wednesday to avoid blackouts may not be enough. The utility operators urgently need the wind to start operating the windmills or things might get worse. Reuters News has more:

(Reuters) – Texas’s power grid operator on Wednesday took emergency measures to avoid rolling blackouts as soaring electricity demand threatened to outpace available supplies amid a stifling heatwave.

(Reuters) – Texas’s power grid operator on Wednesday took emergency measures to avoid rolling blackouts as soaring electricity demand threatened to outpace available supplies amid a stifling heatwave.

The Electric Reliability Council of Texas (ERCOT), which operates the grid that serves more than 26 million customers, initiated a rarely used emergency program that is triggered when supplies fall below a critical safety margin.

Earlier, ERCOT had urged residents to cut power use during the hottest hours of the day and warned of a risk for rolling blackouts. Residents were asked to turn up thermostats, defer the use of high-power appliances and turn off swimming pool pumps.

The emergency notice came after ERCOT began paying suppliers an average of $5,000 per magawatt hour to keep generators running. That price is the highest the grid operator pays. “They were pulling a lot of levers to avoid going into emergency operations and rolling blackouts,” said Doug Lewin, president of consultants Stoic Energy LLC. (read more)

Call me Captain Obvious, but in addition to the population migration, it looks like Texas imported California’s energy policies. The sustainable energy isn’t sustainable. However, on a positive note, their state ESG score is improving.

(more…)

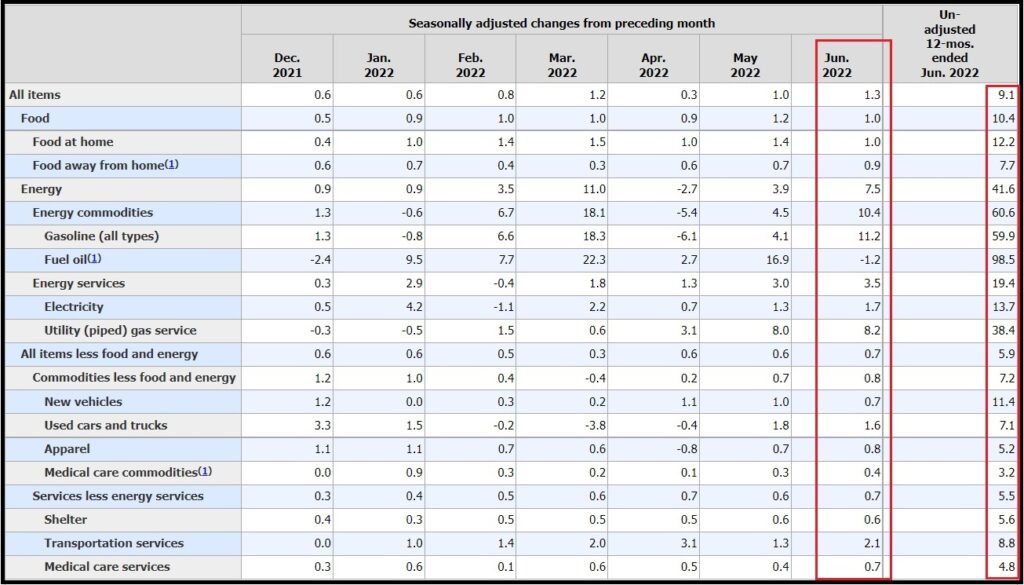

Seriously, it’s stunning, yet oddly not surprising, that the same multinational forces who created the global inflation crisis as a result of following the World Economic Forum spending agenda, are now claiming the global economy is simply too hot, too successful, there is just too much demand, and that justifies their raising of interest rates:

Seriously, it’s stunning, yet oddly not surprising, that the same multinational forces who created the global inflation crisis as a result of following the World Economic Forum spending agenda, are now claiming the global economy is simply too hot, too successful, there is just too much demand, and that justifies their raising of interest rates:

First, the larger ‘layoff‘ issue is going to be more prevalent as the economy contracts and consumer demand declines. There is almost no expanded investment going into any Main Street business that sells non-essential goods.

First, the larger ‘layoff‘ issue is going to be more prevalent as the economy contracts and consumer demand declines. There is almost no expanded investment going into any Main Street business that sells non-essential goods.