As higher interest rates continue to put pressure on borrowers, the ability of the average person to afford a mortgage diminishes. Higher mortgage rates lead to downward pressure on residential home values as fewer borrowers can afford higher payments. Simultaneously, commercial real estate is dropping in value as vacancies continue increasing.

Put both of these issues together and already tenuous banks holding mortgage bonds as assets can become more unstable.

Put both of these issues together and already tenuous banks holding mortgage bonds as assets can become more unstable.

This dynamic creates the continual tremors in the background of an economy already suffering from high inflation and low consumer purchasing of durable goods.

A perfect storm starts to realize.

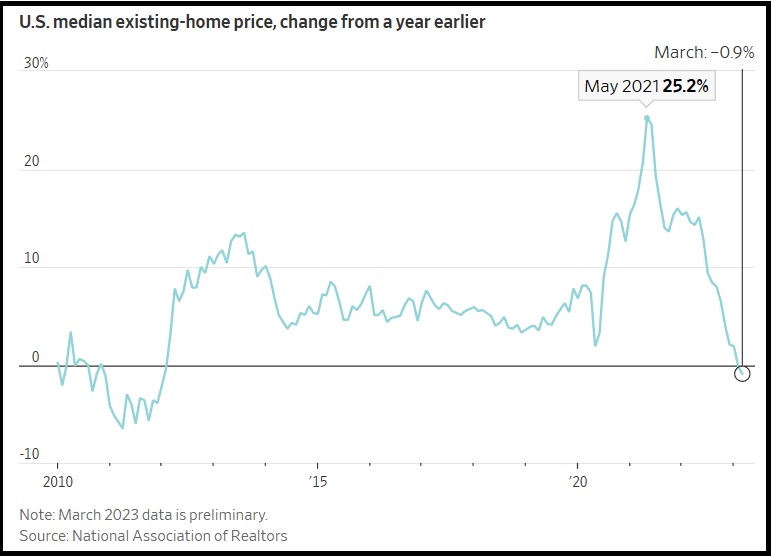

(Wall Street Journal) U.S. existing-home sales decreased 2.4% in March from the prior month to a seasonally adjusted annual rate of 4.44 million, the National Association of Realtors said Thursday. March sales fell 22% from a year earlier.

March marked the 13th time in the previous 14 months that sales have slowed. The housing market had a surprisingly strong February, when sales rose a revised 13.75% from the previous month. But after mortgage rates ticked higher, March sales resumed the extended period of declines.

The housing market’s slowdown is now starting to weigh on prices, which have fallen on an annual basis for two consecutive months for the first time in 11 years. The national median existing-home price decline of 0.9% in March from a year earlier to $375,700 was the biggest year-over-year price drop since January 2012, NAR said.

Median prices, which aren’t seasonally adjusted, were down 9.2% from a record $413,800 in June. Home prices in the western half of the U.S. experienced some of the biggest gains for many years but are now falling the fastest.

[…] Housing starts, a measure of U.S. home-building, fell 0.8% in March from February, the Commerce Department said this week. Residential permits, which can be a bellwether for future home construction, dropped 8.8%.

The housing market slowdown shows one of the main ways that the Fed’s aggressive interest-rate increases are rippling through the economy. Housing is one of the most rate-sensitive economic sectors, and high housing costs have been a big contributor to inflation. (read more)

Before looking at today’s graph showing median existing home values, remember me saying this in 2021?:

“I said in June, at a macro level home prices had reached their peak (last two weeks of May, first two weeks of June was apex). Obviously, there are some geographic home value increases still happening as COVID related regional issues and work opportunities are shifting populations. There is also a lag and ripple effect that takes time to work through the economy. The macro-apex will not be visible until next year.”

When I said that in 2021, people said I was wrong. Well, with hindsight now visible within the data as it is reflected, look at the result:

May and June 2021 was the peak of year-over-year percent of change in median home value increases.

So, what was going on?

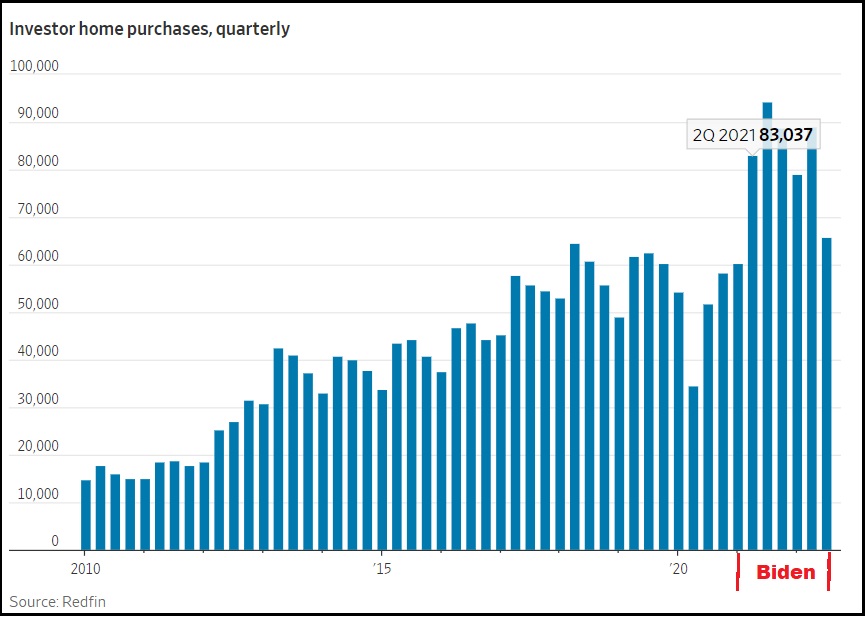

As CTH outlined in 2022: If you look closely at the timing (keep in mind the data reporting lag) what you will notice is that financial institutions began a big surge in purchasing hard assets, specifically real estate, as soon as Joe Biden took office (Jan ’21), and the economic policy became evident. Intangible financial instruments became an immediate risk as the professional financial control groups recognized energy policy would drive inflation (supply side) and devalued money would fuel it (demand side).

As an offset to predictable inflationary policy (the insiders’ game), institutional money (Blackrock, Vanguard etc) was moved into hard assets with tangible value.

This shift in asset allocation, institutional sales, helped fuel a false surge in home prices and their valuations. CTH was writing about this in 2021, and sounding alarms as it took place. 25% of all real estate purchases were being made by institutional investors.

We The People got screwed.

The dynamic was predictable. The Biden administration economic policy, energy policy and monetary policy, was going to cause massive inflation. CTH was shouting about it in early 2021 and warning everyone to prepare for waves of price increases that would naturally surface first on high-turn consumable goods, and then embed into longer-term durable goods.

Despite claims to the contrary, this 2021 inflationary explosion had nothing to do with the pandemic or supply chain shortages. It is entirely self-created by western governmental policy; the collective ‘Build Back Better’ agenda. You can see now from the background moves within the financial sectors, they too knew the reality and their money shifts reflected that despite their ‘transitory’ pretending they were mitigating their own exposure.

We the People were yet again going to be victims of specifically intended monetary, regulatory, energy and economic policy.

We the People were yet again going to be victims of specifically intended monetary, regulatory, energy and economic policy.

The investment class rulers of the WEF assembly shifted assets to avoid the pain that we would feel. We “would own nothing and be happy,” and their shifts would position them to own everything and be in control.

Overall govt spending and regulatory controls drove inflation for these past two years. The ‘demand side’ was blamed, despite the lack of demand. I will be proven right when history is concluded with this. Interest rates were raised by central banks in an effort to support the policies that are driving ‘supply side’ inflation, not demand side.

Energy policy was/is crushing the consumer by driving up the cost of all goods and services. To support the overall goal of changing global energy resource and development (a false and controlled global operation), central banks raised interest rates. Various western economies, including our own, have been pushed deeper into a state of contraction by central banks crushing consumer demand, and eliminating investment via increased borrowing costs.

In short, the goal was/is to lower energy consumption by shrinking the economic activity. This, according to the BBB plan, was needed at the same time as energy development was reduced. These economic outcomes are not organic, they are all being controlled by collective western government agreement.

Within this control dynamic, there was always going to be a point where the reaction of the people to their economic reality means the financial control elements need to shift direction. They will always maximize profit and minimized risk, while knowing what the larger objective remains.

Just like every other durable good, housing demand contracts as prices and costs become unaffordable. The loss of equity within your home is damaging to your own value or ability to borrow against it.

From the perspective of an institutional asset, that same equity drop is an investment loss. However, the investment loss is not materialized until the sale of the lower valued asset is completed. Retaining declining real estate on investment books, creates an artificially high appearance of the investment result; unless and until the real estate is sold at a diminished value.

As mortgage rates rise, just as a consumer would pull back from the housing market, so too will institutional investment groups now control the slow dumping of the asset to remove the equity they pumped into it. Much of the investment housing will be retained as rental housing, with the monthly rents being part of the returns on the investments. However, as this dynamic unfolds further investment purchases of houses stop, because the asset overall is declining in value. This halt of investment activity also worsens a steeper drop in home values.

Notice this line within today’s WSJ article: “The housing market had a surprisingly strong February, when sales rose a revised 13.75% from the previous month.”

What happened in February? The BIG CLUB [Blackrock, Vanguard, Citadel, etc.] moved liquid assets out of banks into hard assets (real estate), to avoid a predictable banking issue which surfaced a month later in March. They knew what was going to happen in banking, they moved their own assets to avoid it.

Uh hmm. Wondered why it was late before you posted today.

Was beginning to worry you got raided and everything seized.

LOL 😂😎

My name must be Phillip Ive been screwed so many times..

My sympathy, me (not to crow) but not too much.

The 2009 financial crises, me n mine wouldn’t have known about, if we had cut the cord; I LOOKED, HARD and could see no way in which we were adversely impacted.

The current financial storms also, for us are off in the distance,…its like hearing about a hurricane or tornado, happening somewhere far away.

I have sympathy and empathy for those effected, but me n mine,…aren’t.

Got off the credit merry go round, 20+ years ago, got off the health insurance and medical industrial complex, years before covid was a gleam in Fauxis eye,..

If doing “what every body ELSE does” (like using credit, and health ins. etc.) keeps biting you in the butt, perhaps you need to consider going 180 degrees from “what everybody does” and try something DIFFERENT?

I have gone to ground since 2010.. Just trying to live out the life I want, earned and hope lasts til I die..

I’m interested what you do instead of having health insurance. Concierge medicine? Take vitamins and supplements?

For me it is living a life knowing some day will end and making peace with that.

Me, too, I want to know these things.

Congratulations!

Those that have contrarian attitude tend to do very well.

They are often much maligned but often proved to be very wise.

The last 15 years or so have been surreal…in essence “ free money” was abundant.

0% financing on new vehicles..variable residential mortgages at 1% or so..utter madness.

Our own 31 son, a successful young businessman struggled to accept our warnings from 18 months ago.

Warnings that included maybe the tripling of his residential mortgage interest payment.

Well he listened is now extremely relieved.

Cheers to all, and if possible get out of the “debt prison”

😎

Romans 13:8 Owe no man anything, save to love one another: for he that loveth his neighbor hath fulfilled the law.

Those who bought hard assets like real estate, especially those who borrowed to do it before the massive real estate appreciation, cleaned up and made millions and billions. To be leveraged on an asset that appreciates during inflationary times is very profitable.

Say you put $100k down on buying $1 million in real estate in 2021 when Biden came into office and made inflationary policy moves. Interest rates on even investment real estate was in the 4%’s. The real estate rents cover the 4% mortgages and expenses plus cash flow. Then rents and values start to increase with inflation. The mortgages amounts and fixed rates stay the same, so you get more cash flow, plus more net worth on paper. Real estate in the West where I am (and where I invested) went up 30+%. That’s $300,000 on my $100,000 investment over two years, plus the cash flow, tax benefits of depreciation against my income, and principle pay down. I sell and I’ve more than tripled my money in two years. Mostly because I wisely chose when to owe a bank $900k and use only $100k of my own.

Timing of real estate sales and purchases matters BIGLY. I down sized. Sold high end at the high and bought lower end cash with a cushion for improvements. Very glad I made the move, although tough on my over 65 yo body. I halved my RE taxes without losing my homestead exemption. My 450/month HOA is now 30/month water and 80/month on lawn care, plus what I spend to combat ants and fertilize. I was not using the pool or the cable tv channels and now I do my own landscaping. My garden provided a ton of greens and tomatoes and now cucumbers and green peppers. The monthly savings have purchased tools, landscaping rocks and planters that will last many years.

Direct Primary Care practices are the medicine of the future, with some small major medical policy needs.

Most people would do just fine with a $100 monthly fee for a DPC membership, and kids, too.

Do they still sell major medical or as we used to call

it just hospitalization. I thought they did away with that

with Obamacare?

Yes, Obamacare did away with policies that were major medical only insurance. After I retired, I had cobra for 18 months, then, another 18 months of a major medical policy until they were no longer allowed. Then, I went without insurance for a year to 18 months (I forgot) until I qualified for medicare.

This is the way it used to be. You went to the doctor, you paid the doctor.

Wasn’t one of the world’s richest men on the Titanic when it sank? IDK, maybe he was the richest man in the U.S. at the time. Regardless, his wealth and status didn’t save him.

Plenty of smart people, and rich people, will survive the country going down in flames. IDK, perhaps that’s all that matters. I’m old so what do I know.

My family fought the Bolsheviks before they saw the red blood writing on the wall, literally, and escaped. I’ve nowhere to go so we’re gonna do a dance to God. Money is a cruel master. God bless.

I think there was someone on board who was planning on torpedoing the creation of the Fed.

John Jacob Astor the world’s richest man. A german immigrant who did no college.

More than one of those.

Some people think that that was intentional because the Titanic held all the prominent men who were against a Federal Reserve bank.

Wise people and adaptable people will survive this until the Lord returns. Maranatha.

I’ve got a friend who works for cash and is as independent as one who files tax returns can be. He had no health insurance because he was healthy and chose to take the risk – he was fined nearly $6000 under Obamacare’s forced coverage.

The real estate market will bifurcate- all cash institutional grade go up, and residential financed by mortgage will decline as interest rates stay high.

The young will all rent. Sad.

SD is a genuius!!!!!!!! In all things!!!!!!

Biggest transfer of wealth…ever. Hussein promised he was going to ‘spread the wealth around’, but he left out that while spreading it, it was only being spread to the top tier. My heart goes out to the younger generation.

Mine doesn’t , they voted for this.

Perhaps…but they’ve been brainwashed and programmed. They’ll never know ‘freedom’.

They voted?

Another reason to despise Boomers…and I do despise them. Fortunately their days are drawing to an end.

Wow! Sounds like Oprah.

Sounds like an ignorant hater.

Oh.

Yeah, I guess that would be Oprah.

Definitely not a lover of God. (1 John 4:20)

Yep, I’m one of them and roundly disappointed in my generation. God be with you.

It’s very satisfying to know your kids and grandkids will feel the same about you. Carry on.

IDK, I never got the impression mainstream youth blamed the greatest generation for the violence, assassination, economic malaise, political chicanery and, oh my, Carter. I certainly didn’t.

However, I did often debate with my parents about them taking responsibility for ‘going along to get along’ instead of being more revolutionary. IDK, perhaps the war (WW2) zapped some of their zeal. Used it up. Or they were brainwashed.

I was a skeptic at an early age and it brought a lot of trouble to my doorstep, including violence. One can see that skepticism in this sub-thread, where I show disappointment in my fellow boomers for likewise being focused on personal ‘getting ahead’ without any apparent larger concern for the country going down in flames and the impact on those progeny. Oh, well, personal choice. Smoke while you got ’em.

Singling out a particular age group among the dozens who have lived during the dominance of the western civilization rulers is just stupid and ignorant.

Your descendants will eventually curse you in just the same way.

Boomers did not vote for this!! You got the wrong generation.

We had as much control back in the day as conservatives do today. I remember when Reagan was governor of the state I lived in back when I never dreamed of returning to Florida. Politicians have been bought for decades if not centuries.

Hussein wasn’t talking about spreading his wealth around only ours!

Looks like more to come on this:

Homebuyers with good credit scores will soon encounter a costly surprise: a new federal rule forcing them to pay higher mortgage rates and fees to subsidize people with riskier credit ratings who are also in the market to buy houses.

The fee changes will go into effect May 1 as part of the Federal Housing Finance Agency’s push for affordable housing, and they will affect mortgages originating at private banks across the country. The federally backed home mortgage companies Fannie Mae and Freddie Mac will enact the loan-level price adjustments, or LLPAs.

Mortgage industry specialists say homebuyers with credit scores of 680 or higher will pay, for example, about $40 per month more on a home loan of $400,000. Homebuyers who make down payments of 15% to 20% will get socked with the largest fees…

Joe Biden to hike payments for good-credit homebuyers to subsidize high-risk mortgages – Washington Times

Yes…I saw that. Once again, they punish those who did the right thing. They worked hard, paid their bills, kept a good credit rating…and now they have to pay.

IS. 5:20 Woe to those who call evil good, and good evil;

Who put darkness for light, and light for darkness;

Who put bitter for sweet, and sweet for bitter!

Social Justice. 🙄

As we’ve all known, it’s simply injustice to the just.

There’s also apparently something on the horizon in CA where the state becomes a partner with low income buyers, injecting cash into the deal and extracting it later upon sale. Can’t recall the details but it seems like they’re moving in the same direction.

I saw that.

I think it was essentially 20% down from the state, no interest on the down, no payments on the down, whenever the home is sold the state recoups their down payment plus 20% of the total capital gain realized in the sale.

It’s going to ruin the housing market completely.

He who stands closest to the money printer gets most of the…

Live your life to the best of your ability!

We know that bad times have been arriving slowly throughout the decades, but they have quickly worsened as of November 2020.

All of this is and has been predictable: the inflation, the shortages, the increase in crime, the distortions in the labor market, and on and on.

The goal is to destroy you and to destroy America economically, politically, psychologically, and spiritually!

Do not panic and e.g. sell your house for a loss, or start selling stocks at a loss!

Keep living the best and happiest life possible, despite setbacks and constant bad news.

Because our enemies – not opponents any more, enemies! – want us to panic, to be demoralized, and to surrender to The Deep State.

Keep throwing that sand into the gears of The Deep State.

In a poem from 70 years ago, German writer Gunter Eich advised something similar:

“Seid Sand, nicht das Öl, im Getriebe der Welt!“

“Be Sand, not the Oil, in the gears of the World.“

I’m thinking of down sizing alot.

Its not panic but if things keep on going like they are

I can’t keep pretending that I will be able to do what I want to!

Explains why I couldn’t find much housing for sale for less than $250,000 in central Maine last year.

Ones that weren’t a remodeled manufactured home built in the 80’s/90’s maybe with a fraction of an acre.

Handmaiden to Blackrock et al…all is well, all is well.

WSJ is part of the problem.

It is not the same paper it was 20 years ago. Much of the business reporting is nonsense. Many of the reporters must either not understand economics or “pretend” not to understand.

It would have been fantastic to be around to read it in the 70s, when Bartley and Wanniski ran the place. One can only read recollections such as those of Bartley in his book, The Seven Fat Years.

I remember it being delivered to the house but was too young and ignorant of the nuances to appreciate it. I was more interested in cars and girls. My dad worked for .gov and was into all that investing and economic stuff.

Diminishing equity.

That the funny noise coming from the attic.

I interpret the image of the guy with his fingers crossed behind his back,…differently.

THEY, the barstids that want us DEAD, are attempting something that has never (successfully) been done before (own the World) and are attempting to achieve that in a WAY thats never been tried before.

Hence, their has to be some crossed fingers, or even looking out thru splayed fingers “I can’t look!” sorta thing.

They can’t have confidence of KNOWING it will work, and the consequences TO THEM (which is ALL they care about) IF it fails, are truly horrific.

Hence the crossed fingers, symbolic of their own hopium.

Remember that are attempting to “own the World” are in fact psychopaths. They have no human empathy and believe themselves to be unstoppable, infallible, omniscient, and soon to be trans-humanly immortal. In other words they believe themselves to be “as gods”. Fortunately or unfortunately, depending on the point of view, their Tower of Babel has been constructed on a foundation of the Sodom and Gomorrah they have recreated.

They are murderers. A Crime Cabal is running the world.

Well Sundance, City Hall has not got the message, just got my updated assessment and my value increased by 12% in the north Dallas suburbs from last year. Gotta pay for more drag queen shows and less algebra.

Tarrant county same. Taxing unrealized capital gains and “wealth”. And ours is a Red county now.

Or should I say ” Red”.

Ditto here.. I’m back to the high it was before.. coastal suburbs here. I’ll keep my 2.99% and turn it into a rental in 10 years when I retire if I’m lucky.

remembergoliad: Lucky you! We experience the same thing in Los Angeles, although drag queens are nothing new, here.

Feel sorry for young people who bought at the high. Wonder how many are underwater.

I’ve been watching home foreclosures in our socialist rag for over a year now. A year ago foreclosure notifications filled half a page; two weeks ago there were more than 2 full pages of people who were losing their home.

Ya, a lot of home prices skyrocketed at that time, I remember it well. Some of it was driven by the riots and people fleeing the big cities and a lot of those cash buyers were either the big investment firms as Sundance points out or foreigners..

Now the next game is to knock all the people that bought high prices with high interest rates so they lose their shirts.

How are they going to do that?

The same same old sub prime loan scam is incoming.. but this time they are going to charge those with a higher credit score more fees ($40 more per month for a loan of $400K) as a way to insure those that won’t be reliable. Then they plan to buy up the rest with profits from the fee’s as the rest of the masses lose their homes.

They deserve a lot of things.

Being tarred and feathered then run out of town on a rail is one of the most merciful ones.

I know I shouldn’t be surprised that they are screwing over those with good credit and substantial down payments, but I am.

“When I said that in 2021, people said I was wrong.”

Horses to water, sir.

You did what you could, and that’s all anyone can ask.

Well done. Well done, indeed.

“I worry, frankly, that there’s a tension here. The more people, in my judgment, exaggerate a threat of safety and soundness, the more people conjure up the possibility of serious financial losses to the Treasury, which I do not see. I think we see entities that are fundamentally sound financially and withstand some of the disaster scenarios.”

-FBF

History rhyming.

Seems that Blackrock, Vanguard, Citadel etc bought the wrong hard asset. They are now going to need to sell a depreciating asset into a declining market. Doesn’t seem like a winning strategy to me.

With inflation the usual trade is to lever up into real estate. With interest rates on the rise that was not a good idea.

I’m enjoying their pain because I have no doubt they’re feeling it.

Starting May 1 Biden to Hike Payments for Good-Credit Homebuyers to Subsidize High-Risk Mortgages

Homebuyers with good credit scores will soon encounter a costly surprise: a new federal rule forcing them to pay higher mortgage rates and fees to subsidize people with riskier credit ratings who are also in the market to buy houses.

The fee changes will go into effect May 1 as part of the Federal Housing Finance Agency’s push for affordable housing, and they will affect mortgages originating at private banks across the country.

.

https://www.washingtontimes.com/news/2023/apr/18/joe-biden-hike-payments-good-credit-homebuyers-sub/

That’s probably so the institutions can sell their real estate to the next mark at a higher price.

BINGO!!!

When do we start flipping these money lenders tables, who have preyed upon all of us?

Some of us already are but such things aren’t to be discussed here.

I’m satisfied reminding folks that this isn’t ‘stuff happens’ and ‘economic cycles’. Nope, it’s specific humans who’ve made specific choices and used the force of law and threat of imprisonment and death to damage and destroy citizen’s lives.

Never forget. Any of them. Individually.

Lord knows,the limits of my patience.

I tire of trying to do the right thing and continually having the figurative rug pulled out from under me while the unscrupulous prosper.

I haven’t given up yet, I just fuel my resolve some more.

They call it insurrection and throw you in prison.

In numbers we can work with that and go kinetic. If not one’s castle, then what hill I ask?

We heard the warning sundance gave and by July 2021 we sold our comfortable Las Vegas home while that market was high. We were also worried about the impending water crises in the desert and the rising crime.

Took those profits and bought a roof with 4 walls on 5 acres where it gets over 80 inches annual rain with no more mortgage.

Northern WA on the coast 10 minutes to go clamming and surf fishing. Our own woods for meat and heat and made our gardens.

It was so worth it to lower our ‘standards’ on housing to gain a different life.

Thank you Sundance for the warning that gave this pair of old seniors the push to just do it.

Interesting…I head down to Blaine Washington every week or two to buy gas.

As you will know the Bay has Canada to the North..and Blaine to the south.

Our “ dirt” is insanely expensive driven by massive immigration and migration from eastern Canada.

Over the “ 49” fabulous “ dirt” is available.

I believe those counties are as Americans say “ Red” and far away from Olympia and Seattle.

Cheers!

You drive to Blaine vaxxed or unvaxxed? I assume the vaxx rules still apply?

Yep, I am still a pure blood.

Never taken the poison..we are never asked.

Cheers!

Oh very red county indeed as Olympia is 1.5 hours away. Those folks in Seattle have more money than sense.

We were in Lynden for a President Trump rally, it was all President Trump country.

Burlington too…

Great memories!!

(Posted this again, this time to Dekester directly because I don’t know if people who replied to the original comment made by Liqueda get the other reply notifications.)

Praying you are all staying safe out that way. Not trying to provoke fear, just genuine care and concern. Upon reading your comment a few minutes ago, for some reason, it made me remember hearing years ago about the Cascadian fault line, and so I just looked it up to see if I was remembering correctly if that was the one up your way, and it just so happens,

When I did a search a few minutes ago, two articles dated today, came up about the Cascadian fault/subduction zone up that way doing some things they haven’t seen before. I don’t know if that is cause for concern, but wanted to at least let you know in the event nothing was reported in your area. I put the links below.

Lifting yours and Liqueda’s family, and all others in the area up to God for safety and guidance and that you have “ears to hear” if/when required. God bless you and take care!

https://www.sciencedaily.com/releases/2023/04/230411105851.htm

https://www.sciencedaily.com/releases/2023/04/230411105851.htm

Praying you are all staying safe out that way. Not trying to provoke fear, just genuine care and concern. Upon reading your comment a few minutes ago, for some reason, it made me remember hearing years ago about the Cascadian fault line, and so I just looked it up to see if I was remembering correctly if that was the one up your way, and it just so happens,

When I did a search a few minutes ago, two articles dated today, came up about the Cascadian fault/subduction zone up that way doing some things they haven’t seen before. I don’t know if that is cause for concern, but wanted to at least let you know in the event nothing was reported in your area. I put the links below.

Lifting yours and Dekester’s family, and all others in the area up to God for safety and guidance and that you have “ears to hear” if/when required. God bless you and take care!

https://www.sciencedaily.com/releases/2023/04/230411105851.htm

https://www.sciencedaily.com/releases/2023/04/230411105851.htm

Just in time for the Biden Rule on mortgages to go into affect.

Straight up Communism!

“Homebuyers with good credit scores will soon encounter a costly surprise: a new federal

rule forcing them to pay higher mortgage rates and fees to subsidize people with riskier credit ratings who are also in the market to buy houses.”

homebuyers with credit scores of 680 or higher will pay, for example, about $40 per month more on a home loan of $400,000. Homebuyers who make down payments of 15% to 20% will get socked with the largest fees.

Nobody is going to make down payments going forward. More will pay cash or go without. Those who can not pay cash, but can pay the extra fees will do so until they can pay it off. This is going to make it much, much more difficult to sell anything. Right when seniors need to down size and young families need bigger homes. This makes it much harder on everyone.

How bout some happy news? Under Joe The Vigorous new scheme: Middleclass ( White) home buyers will be subsidizing lower income( non White) homebuyers by paying higher mortgages. Ok thats not so happy. But at least when your living at a pay- by -the -week cheap motel you can bask in the warm glow of happiness that an illegal invader is living in the house that you could have bought. Ok thats not so happy either. Just be happy you have some greasy take out chicken to eat. K?

You think they are going to let you eat meat?

Except chicken is spelled Chick-In because it’s made from Chick Peas and Insects.

But yet the Appraisal Districts in Dallas and Hidalgo Counties in Texas are hitting me with a max value increase on my houses every year, hammering me with property taxes. (One is my mom’s and in probate so I don’t own it, am just responsible for it as executor.)

Yeah, i live in Kaufman county just east of Dallas and they just increased our valuation again the max legally. Housing is booming here and cities are putting out lots of bonds. My taxes have doubled…. Time to get out. The schools are bankrupting us and they suck .

Wife and I bought a new house in 1981 for $99,000. We had a 14% mortgage. Wife stayed home with our two young children. Stagflation was all around. That situation too was created by an energy shortage. National debt today is unsustainable. The WEF options are dwindling.

When do Lamp Post Ornaments become Great Again?

There are many Traytors out there just begging to be displayed!

The Democrats are willing to destroy the economy of the United States and put millions of people out of work in furtherance of the insane Climate Change Hoax. It shouldn’t be a surprise because they did the same thing with the Covid-19 Hoax!

The Climate Change Hoax is a pretext to take totalitarian control. The destruction of the economy is essential because then the narrative will be that capitalism and conservatism destroyed it and only the Great Virtue Signalers can save you through a basic income payment to your digital currency account and relinquishing all your basic rights and accepting Gubmint as your god.

The “Climate Change Hoax”, “Covid-19 Hoax”, and even the “Conflict in Ukraine Hoax” are means to an end. They are not ends in and of themselves. Also remember that “republicans” are just the other branch of the political machine being paid by the same business for pretending to be the opposition.

I work the foreclosure markets at county courthouses monthly. There has been an unusual amount of higher end houses and average houses marked for sale the last 3 months or so, but they have been able to pull them out at the last minute and the sales thus cancelled. So, there’s been more than usual, but masses of people are not walking away from their mortgages in disgust…yet, but I am seeing some birth pangs. In 08 you had walkaways that walked away because they were sorry, and you had walkaways that walked away because they were upside down.

Looks to be accelerating more in certain major metro areas:

https://finance.yahoo.com/news/more-americans-losing-homes-foreclosures-140140828.html

If running into the bottom feeders that comb the notices of default and trust deed notices, please implore them to stay off the properties. Out my way that’s a good way to get your brains splattered all over the pavement.

I had a few bottom feeders on my place during the last crash, mistaking it for a neighbor’s property and they were lucky I didn’t kill them. I was far more peaceful back then. Wait for the sheriff. That’s my advice. I’ve already heard the gunfire and the sheriff’s cars speeding by, far more in the last month or two than in years if not decades. IDK how it is in the city but just stay off ag land if a bottom feeder/opportunist. You’ll live longer.

Headline: …Month-over-month…

“Year-over year” …”the National Association of Realtors said Thursday. March sales fell 22% from a year earlier.”

A home across the street and on the corner of 2 main streets in my subdivision (but still not that busy) went on the market 4 days ago and went under contract yesterday. It was a rental. $250K for 1317 square feet, 3 bed, 2 bath, 1 car garage being sold as is. It was built in 1976 and based on the pictures in the listing, the kitchen is original except for the appliances. I hope whoever buys it will be living in it but I’m not getting my hopes up.

Other, more updated homes are selling for$285-305K recently so we haven’t gotten hit with price drops yet.

A friend of mine widowed mother pasted away. She lived in the house for 55 years. Hardly any renovations during that time. They put the house up for sale in March and had an offer within 2 days. “An investment firm” bought the house.

The scam these investment firms run in housing is they buy up a bunch of houses in one area, then they over pay for a few of them causing the median prices to increase on the books. Then they can take out bigger loans on the houses, which basically equates to free money for them.

Every realtor, since forever: “Now is a great time to buy a house.”

I think it is premature to explain the February activity as a result of “Big Club” purchases. These same institutions can see the commercial property market begin to fall away.

I do not believe that knowing this they would deepen their residential holdings.

I keep waiting for the economy to collapse as it must someday but tonight on the news I hear that the travel industry is gearing up for a huge summer vacation season. Apparently those who plan to buy expensive airline tickets haven’t gotten the word yet. In fact I haven’t seen any indication of a collapse at all except for what I read here. Since this website is one of the few that I trust for honesty it makes me wonder just what is going on. Why aren’t we seeing the results of Biden’s abysmal policies yet?

We’ve been waiting for gold and silver to start going up, but it too seems to be artificially held down by someone or something.

Makes no sense in this economy that is slowly emploding.

Gold broke 2000 and it is not backing down, they drop it below, it bounces back up. This is its new floor. Previous breaks above 2000 were not this robust, they were able to drop it below 1900/1800 in a few weeks. Not this time. This is mostly how gold has been working since 2008 when it broke out t0 900 from 600 per ounce. Gold and silver are heavily managed. In 2008, the premium for a stamped coin in any metal was $50. Now, you can’t touch an eagle for less than a $200 premium. A little less premium for a buffalo or a Maple.

Credit.

Watch for the rise in credit card debt.

Sooner or later those that are maintaining their current lifestyle are going to max out their credit.

I am also watching closely the unemployment numbers.

I think of it like a snowball going downhill.

Debt is an effective economic weapon. PDJT used it, both as POTUS and privately, to leverage power and business. Corporations use it every day and they have little compunction about walking away from it if the numbers indicate they should. Corporations aren’t AI, rather individual humans making individual. choices. They choose to do what they do.

We can too, but somehow we’ve been brainwashed and cowed by the moneychangers into a narrow line of thinking. I view economic war as one step down from kinetic war. History tends to agree with me. Boston Tea Party anyone? Blockades on Japan? IDK, open your history books and find the examples. They’re out there.

Some of these foreclosures and walk away are due to layoffs, as well as over spending on housing. My area, housing is still very tight. There is not enough inventory and we have growing industries.

Yep,

Hotels are outrageous..$200-300 per night..Air BnB houses $500 per night.

Geesh!

Excellent analysis. Top notch. From a historical perspective there have been numerous attempts to steal the land/real estate of the public throughout American history. Not a tale typically told. But, oh so true.

Capital mobility of the rich is always more liquid than the lower classes to provide for these schemes and entrapments.

America’s greatness differentiating it from other nation states was the strength and size of our middle class.

The regulatory capture of the public via the buying of govt. is disassembling that middle class at an astonishing rate .

Computerization of currency has been a hallmark of this in ways I could have never imagined, say even, 15 years ago. And, I write this as someone educated at Duke in Economics, Political Science and History.

I hope and pray Sundance’s analysis can spread to the greater public, the body politic, and that they would understand

We all need to be shout these messages with conviction from our Treehouses. We don’t have long to turn this ship.

Congress are unusually prescient when it comes to timing their stock buys/sells…

Until rates cause prices to drop nothing will change.

An infinitesimal sign of price pressure is, of late, like in the last week or two, a huge retailer, Amazon, has markedly been marking down ‘deals’ on food items, as well as doing coupon promotions on same, of a food basket of a few hundred items I’ve been tracking since Covid started.

In some cases, the prices are now below what they were when the ’emergency’ began and many are below what they were a year ago. Granted, that’s one retailer and one person’s food basket but to my eye that’s significant. Lower demand may be having an effect.

Just to say i consider myself REALLY lucky to be a subscriber here, where Sundance analyzes what is going on and explains it in a way I understand. Just a short post to say thank you.

SD…as I have mentioned before… your need to separate Red and Blue States in your analysis. All Real Estate is local.

Yes… higher interest rates are hurting consumers yet Red States are still rocking…as a result of diminished supply of homes and demand from people fleeing Blue States coupled with companies moving out of Blue into Red. I don’t hold a lot of hope for folks in Blue States…taxes, crime, poor schools etc.

Builders and or loan outfits are buying down rates in order to satisfy monthly mortgage payment requirements of the borrowers. Yet this “buydown” is being added to the back end of the mortgage balance…in some areas (Red) appreciation of the home will occur over time and the possibility of a refi to a “hopeful” lower rate will benefit these borrowers.

One aspect is occurring…higher costs for steel and pipe or the lack of availability of it is causing the costs of homes to increase and construction of new homes…while pre-pandemic was approximately 140 days is now double to 280. Labor is plentiful…(Red) …but it is causing a lack of supply for homes. Land Costs in Red States is still high. I expect Construction costs to subside later in the year which will help builders (Red) adding to supply.

Please refine your analysis in future discussions…

MAGA 👊👊🇺🇸🇺🇸🙏🏻🙏🏻

I wish I could put a PDF in here or photo so you could see locally what is going on in the housing market.

This is for March 2023

This would be me!

Wait for the next shoe to fall when the combination of surging recession-triggered job losses and plummeting inflation-robbed disposable income drive people into “Communal Living” with multiple-resident and multiple-family homes!

Yep, I remember.

Houses never dropped as much as they should of in 2008.

And they won’t this time, unless a lot of banks are allowed to fail. Then you’ll have true valuation.