Stop looking at the Washington DC Potemkin village; start looking at the financial system behind it that controls it.

You may recently have seen this story:

You may recently have seen this story:

WASHINGTON DC – Homebuyers with good credit scores will soon encounter a costly surprise: a new federal rule forcing them to pay higher mortgage rates and fees to subsidize people with riskier credit ratings who are also in the market to buy houses.

The fee changes will go into effect May 1 as part of the Federal Housing Finance Agency’s push for affordable housing, and they will affect mortgages originating at private banks across the country. The federally backed home mortgage companies Fannie Mae and Freddie Mac will enact the loan-level price adjustments, or LLPAs.

Mortgage industry specialists say homebuyers with credit scores of 680 or higher will pay, for example, about $40 per month more on a home loan of $400,000. Homebuyers who make down payments of 15% to 20% will get socked with the largest fees. (read more)

If you focus on the DC Potemkin Village, you view this move through the prism of Biden’s FHFA creating a policy to favor low-income (nonwhite) voters by punishing stable credit worthy borrowers. That’s what the powers who control the levers, and create policy, want us to focus on. That’s not what is going on.

Biden doesn’t control anything. Biden is a puppet to the multinationals that control DC policy. When Biden was installed, the people who control the money and wealth (Blackrock, WEF assembly etc.), the people behind the Potemkin Village, knew what the larger economic agenda would create.

Biden doesn’t control anything. Biden is a puppet to the multinationals that control DC policy. When Biden was installed, the people who control the money and wealth (Blackrock, WEF assembly etc.), the people behind the Potemkin Village, knew what the larger economic agenda would create.

{GO DEEP}.

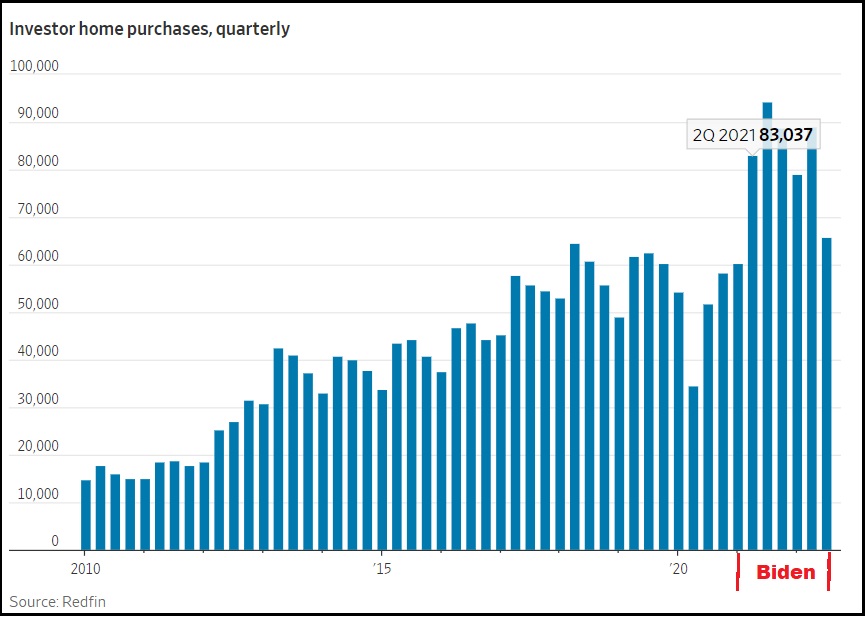

They knew BBB, or Green New Deal policy, combined with excessive govt spending would generate inflation. They moved their money from inflation sensitive liquid and paper assets, into real estate. Inflation raged, liquid assets depreciated, real assets (real estate) surged. 25% of housing was bought with investment dollars by institutional investors, housing prices skyrocketed – their investments increased accordingly.

The financial control operators avoided the consequences of the government policy they controlled.

Now, those same institutions need to turn those appreciated real estate assets into capital outcomes. They need to sell the real estate. However, the assets are now at maximum appreciation and dropping as a result of the central banking moves to raise borrowing rates.

How do they exit the investment? They need a mechanism – a new policy to create the financial instrument that transfers the increased investment wealth back into their hands.

They need buyers.

How do they get buyers? They create new policy.

That’s what is behind this new FHFA rule. Fannie Mae and Freddie Mac will create a new category of buyers that allows the investors to sell the real estate assets at higher appreciated values and exit their investment. They will transfer the depreciating loss of the asset to the new buyers, like a game of hot potato.

Learn to look behind the Potemkin Village to the institutional financial operators who control the laws, rules and regulations. This is all a continual game of wealth transfer and redistribution. There are trillions at stake.

Look at who moves the money around and how they position govt policy for the shifts into and out of the financial system they control. All of this is being controlled, and Joe Biden has no idea what is happening beyond the talking points that are put in front of him.

The evil continues to overwhelm like waves on a shoreline.

The evil has always been there. Never forget what kingdom rules the earth.

HINT: It isn’t the Kingdom of God.

The evil continues, and will get much worse, until the people doing the evil stop doing it. How that happens is the ten million dollar question.

they aren’t going to stop

until someone stops them

so far no takers

My bet is on the Second Coming.

I got stupid how does making it harder to buy make it easier to sell expensive assets???

Even with a free six pack of bud light would I take 7% mtge and buy anything right now

Why? Serious question.

You aren’t the primary buyer here. Your lender is, with your income/productivity as the collateral.

And, you get to pay for both ends of that deal. Compound interest on an an inflated and depreciating asset. Best not to sign on that mortgage contract.

You think like me on this.

We’re selling two pieces of property. Zero debt.

I never used think leveraged real estate was a prob.

It is now.

It’s because the market runs in cycles…I started over at 55, 2004, got a low-end condo I hated, but it gave a small, safe, well-located place to live while getting established.

By w007. I was doing well. Desperate to get out of there, but I kept looking at the market, thinking something was just “not right”. I had seen the bottom drop out of the housing market in 1986.

So I stayed, watched the market. And was oh so glad I had stayed, as it enabled to retire early. And even buy a second unit at a distressed price, which became a rental unit.

Harder for middle class buyers of more expensive properties. Harder for financially responsible people.

Easier for risky, lower income people buying (relatively) cheaper homes.

2008 Great Recession deja vu.

I just posted the same. How do we divest from these GolboCorp. bastards?

It will be worse then that, most likely worse then the great depression of 1929 , but longer. So do not worry it will not matter what your credit score is in the bread lines.

The people with good credit will absorb the extra $40/month and buy anyway. The people who couldn’t afford to buy before will now be able to. So sales go up. When the economy tanks, as it will due to all this bad economic policy, it will again be the poor left holding the bag, as inflation and job loss forces them out of their new homes.

Which has the future benefit of making the foreclosures easy to scoop up at discounted prices. Rinse, wash, repeat.

THIS!!!!!!

That’s what happened in 2008. Many poor older blacks who had worked and paid off their homes over the years, were talked into refinancing their homes, couldn’t repay, and lost their homes.

Very, very sad. These were people who had “done the right thing” their whole lives, and got screwed by it.

Exactly, how do low income buyers, buy expensive properties? The dummies at the controls! This sounds like the beginning of another financial collapse!

And gazillion dollar bailouts for the well connected.

We bought 3 homes with subprime loans BUT we paid the payments!! We now have 400000 equity in those homes.

It makes homes available to an entirely new group of people who previously could not afford to buy. But your question is still valid.

Like the NINJA* loans of the 2008 crisis, they gave loans to people who couldn’t afford them. When they could, duh, no longer afford them…they were foreclosed on.

In 2008 the banks didn’t take all of the losses from those foreclosures the taxpayers did.

What they are proposing is kind of the same thing they did then, having the good subsidize the bad. Banks packaged their good loans in with some losers and sold them as a package deal on the secondary market.

Everyone was happy because they got their fees to set up the loans and the foreclosed homeowners and taxpayers took the losses.

*NINJA no income, no job, no assets.

The Calvinball economy…

If I’m understanding this correctly, it reminds me of creating new financial instruments to make money explained in both “Margin Call” and “The Big Short.”

How do they get away with…” homebuyers with credit scores of 680 or higher will pay, for example, about $40 per month more on a home loan of $400,000. Homebuyers who make down payments of 15% to 20% will get socked with the largest fees. ???

It sounds illegal to me. Is there no way to stop this grift?

My daughter who works for a large regional builder, says it’s illegal. Doesn’t mean they won’t try.

Of course it’s illegal. Congress would have to approve it!

Illegal. Probably, but illegality means nothing to the Biden admin and those that enable it like the judiciary.

Perhaps more importantly, this concept based in Marxism, can be applied to many other things to harm the productive and reward the elite and non-productive.

Exactly. Illegal only matters when there are consequences for doing the illegal thing.

Like income adjusted utility bills in CA…

Like the eviction moratorium.

“They” will claim it is equity. It seems to me they are trying to lure poor financial risk buyers to purchase real estate in a high interest rate market which will result in a flood of defaults which will result in another too big to fail bailouts for the big club. It perpetuates chaos which is what “they” want. It’s upside down and inside out. Lower rates to higher risk borrowers. Another attempt to crash the US economy. I don’t get it.

I bought my first home at 10% and that was considered a deal at the time of 15%+ interest at the time but people had higher moral standards and the country wasn’t flooded with illegals and wasn’t a rust belt yet.

They make money on the crash.

And create more renters once they are foreclosed on

The Grift stops when there is no more gullible people left to grift upon.

But then i think that’s when the truly scary stuff happens

Sucker born every minute.

Well that depends which side you’re on. There are no laws for the left and Uniparty. JustUS

It would no longer be illegal if the regulations/laws are re-written.

Just like non-vaccines became vaccines when the definition of vaccine was adjusted to fit the reality represented by the non-vaccine.

Getting democrats out of power!

Importing and taking care of third worlders is the most useful and lucrative business for multinationals. Combined with CDOs to make non-performing loan losses disappear into teachers union bonds, it truly is a system rigged against the traditional thrifty American. I mean, who would a bank rather have for a customer, somebody who never bounces a check, or somebody who’s good for three or four a month. Think of the fees

I understand that the flow of $$ is tight right now. Do banks want customers who are always bouncing checks? Will they get their fees when the account is empty? How much do they have to pay someone to acquire the fees for them?

Don Lemon Doesn’t Know How to Respond: Vivek Ramaswamy Joins CNN’s This Morning – Video

https://commoncts.blogspot.com/2023/04/don-lemon-doesnt-know-how-to-respond.html

Just one more thing we subsidize.

The $40 is not some number derived from emperical data. I’m sure actuarially, they have determined that $40 the “sweet spot” of minimal complaints. Naturally, 3 digits would put off some folks buying and $40 is less than half of that.

It’s a tax so weasel Justice Roberts will like it.

Chieftain: That’s exactly what I was thinking.

For now.

If you steal a million from someone, they will hunt you down. If you steal a nickel from everyone nobody cares.

$40 a month is $480 a year of a new “tax” on not just the wealthy, but any regular Joe with credit in the 600’s or above, which is basically every responsible person. My 19 and 22 year olds have credit in the 700’s.

In other words, it’s a lot of money to bail out the banks when they lend to what my businessman dad used to call the “Slow Pay, No Pay” crowd.

Once again the Dems subsidize bad choices and call it fairness and empathy.

Mines about 840. I don’t get many offers for cards, etc, because I pay them off at the end of the month.

(Fill in the blank)

Anyone that buys a home now is a ______ .

Remember the last time the “liar loans” were the rage?

This is a tax hike. It’s being foisted the same way OCare was foisted. Both are tax hikes to pay for their mistakes.

Except these are NOT mistakes. They are trying to collapse everything.

Kind of reminds me of when some Dem states started taxing electric vehicles ( tried ) on milage used, since EV’s were avoiding gasoline taxes at the pump. Gotta love taxes.

“…Joe Biden has no idea what is happening beyond the talking points that are put in front of him.”

Joe has no idea what is happening anywhere with anything other than who is changing his diapers when it happens.

If I were buying a house right now I would be pissed at having to pay for slobs who forever want a handout.

But I guess they were always around, and their free handout was just called something else.

” peace, land, and bread..”. Lenin. 1917

Yep. It was called rent control, rent stabilization and a slew of other fancy names that all mean “make the landlord subsidize the deadbeat”.

It means that even though you own the title to your property, the state controls it.

By increasingly telling you what you can and cannot do with it, they obtain control.

Why buy a house right now at the top of the market when the actual downturn has begun?

Wait it out and rent until the bottom hits and things are at auction.

It is easy for people who put zero down to walk away from a house that is now underwater and can not be sold in a falling home market.

Rents are through the roof..1200 for a one bedroom..1500-2500 for a house.

But if you were selling a modestly priced home this would help move it..

Seriously concluding the U.S. may have a stupider dictatorship than Canaduh

I think we need to view Canada and the US as one and the same. Biden and Trudeau have the same masters. Yes. Here in Canada we are further along the socialist/communist timeline, but probably not by much.

I actually don’t view government officials anymore as having any influence over policy. What I see in our Canadian three party system is exactly what we see in the US uniparty. There are forces at work that are infinitely more powerful and planned than Trudeau who is more than happy to sacrifice the lives of Canadians for his overlords.

It is soul sucking to watch.

DD

It’s all the same all over.

How many people are aware that the “US” government is trying to pass the “Restrict Act,” the “UK” government is trying to pass the “Online Safety Bill,” and the “Canadian” government is trying to pass an “online harms bill” simultaneously.

I will bet a thousand dollars that Australia and New Zealand are also “debating” similar legislation.

And there is similar collusion on CBDCs, carbon emissions, green energy investments, nitrogen use, bug protein diets, gender identity politics, reparations, pandemic controls, and many, many other topics which give the lie to the concept of representative government and national sovereignty.

Bingo!

Ours is really stupid, and arrogant.

However we do no not have the same challenges the U.S. does.

For all its many flaws, and there are many. Other than the refugee scams.

Our immigration policy attracts money, albeit much of it dubious.

Our Punjabi, Korean, Chinese, European and others value home ownership.

All around us luxury homes and upscale condos are being built.

We don’t have your inner city “ issues” yet. Although we are getting a bit closer.

Also back during the last “ crash” 2008 our government kept our banks more or less out of the fray.

Dekester. I’m working on North York. Chinese money is unimaginable. High end cars everywhere.

Saw a Lamborghini today and Googled the cost. $369 000 used!!!

We don’t quite appreciate how wealthy are the Chinese, and how much they own.

Hope all is well in the great west.

DD

D.D.

It is as you say unimaginable.

Lamborghini, Aston Martins, Jaguars, Ferraris abound.

Teslas are common place..

Chinese are the big players..

Sixties built homes on our street, a street without curbs or sidewalks sell upon listing at about $1.7 million.

A Chinese syndicate owns the house to the south of us..they get $4,000 per month for the dump.

They just park their money in “ dirt”

Punjabis build and “ flip” for the Chinese.

It’s quite the thing to watch.

My Chinese neighbour directly across from me, ( a pleasant guy, but slick) has 3 vehicles none are under $200,000

He told me about the five tiers in the Chinese banking system.

Cheers!

God has this..

“God has this.” Thanks for that, Dekester. A great mantra to calm my nerves. 🥰

Dan Dale: The smart Chinese in North York drive Zambonis.

😂😂😂

So if investors will “sell the real estate assets at higher appreciated values and exit their investment”, how can they if the housing market is depreciating?

They bought before the appreciation and interest went off the wall.

Exactly and will retain some to rent out

Remember the bailouts? Too big to fail. Worked once, why not try again?

The entities (Blackrock, etc.) holding these assets have helped push home prices to their peak.

In order to realize cash profit, they now need to sell as the glut of housing is beginning to put downward pressure on prices.

The greedy bastards bought low, plan to sell high, and now plan to sell to unqualified buyers using lower lending standards.

The idea being to help move the glut of unsold properties at much higher interest rates.

Of course, we the taxpayers will inevitably pick up the tab for the future losses when the bottom falls out once again.

9.1.2022: B of A offers zero down payment mortgages in special places…….

Special products for preferred citizens (and others that look like them) in special places.

When I first heard of this, I thought that these people were being set up for bankruptcy. 7 months later we see this new plan for not special citizens.

How to keep special citizens on the plantation?

https://www.cnn.com/2022/09/01/homes/bank-of-america-zero-down-mortgages/index.html

They are exiting and taking their gains.

If you bought a stock which appreciated and you think it might drop, or not appreciate further, you’ll want to sell it and park your money elsewhere. But you need buyers.

Is there a shortage of qualified buyers? Is the market dropping? It doesn’t seem like it just yet.

I don’t know. Maybe this is just a way to keep banks happy. The interest rates are so high right now that nobody who has a home will move unless they have to. Why? They will get less home due to the high interest rates.

It seems to me, that housing prices are, for the moment not going down, because there is limited supply. This is due to the fact that people are putting their house on the market.

This limits apply and thus currently keeps the prices inflated.

They’re Making NINJA Loans (No Income, No Job, No Assets? No Problem!) Great Again!

How else are 50+ million illegal aliens gonna live that American Dream, comrades?

We’ll all be asked to give over any spare bedrooms to an illegal. It’s the patriotic thing to do doncha know.

All those tired and huddled masses, yearning to be free. It’s “who we are”, “our values”, blah, blah…

Wait for it.

I’d burn my house down before I submitted to quartering a third world parasite.

One step closer to that in the UK:

https://www.breitbart.com/europe/2023/01/27/migrant-crisis-private-landlords-asked-to-house-illegals-as-hotels-reach-capacity/

“What does that mean for the rents for everybody else because that’s an amount of housing which has disappeared and not available to the indigenous group?”

I have been telling my neighbors it would happen soon.

Dr. Zhivago.

Yep, NINJA loans until they get around to just confiscating your property that you obtained through white privilege and give it to an obviously more deserving oppressed refugee.

That’s actually happening in South Africa.

South Africa and Rhodesia are their models.

Practise makes perfect.

It’s Dr. Zhivago whether you actually house them, or, you have to help pay their mortgage.

Great movie with Omar Sharif.

I think about that movie a lot lately. I should watch it again, or maybe read the book before it is banned.

We watched it a few weeks ago, this time purposely looking for the commonalities between then and now, there and here.

And sometimes late at night when I can’t sleep I inventory what I’ll keep IF we end up living in one room of our own house.

I am not worried about it at all, just trying to be prepared for what may come through Satan and his demons.

This is little different than the 2008 fiasco- zero down mortgages also pushed up the price of homes and brought lots of buyers into the market that didn’t belong there.

The real difference is that they’re loading the risk partially onto higher income people.

The overall problem remains. With inflation and energy prices still shooting up along with food and car prices, and now with job losses accelerating, the defaults will still come for all these marginal people who can’t afford these houses in any capacity.

Until the government suddenly gives a dang and bails them out?

We were in Palm Springs in 2009 and 2010 decent 1 bed condos could be had for $40,000.

It was incredible..we had heard similar units were $160,000 or so just a few years earlier.

If true…wow!

Machiavellian, as usual.

Kevin McCarthy asleep at the wheel or what?

Right hand on the wheel, left hand out the window.

Palm open.

Don’t have to pay a $40 fee if you don’t have any debt…

I personally did not invite a single 3rd world invader into this nation. I couldn’t care less where they squat as long as its not in the rural areas where they couldn’t afford to buy even with government gifts like this bs.

I have an 800+ credit score but carry almost no debt. Suck it, Obama.

Ditto

My wife always compares us to the same aged couples in our neighborhood. She can’t understand why they all buy anything they want. And we know based on their jobs they don’t make more then us.

I always have to tell her, being in NOVA it’s one of two things. Tons of debt, or their mommy and daddy still fund a lot of their life. The latter is very common In the DC metro area.

I’m proud that I don’t take anything from either of our parents. We do everything with our own money and we don’t add debt. The only time we take on debt is if it’s to buy something where they give you a significant discount for signing up for their lending to make the purchase. And we do that, and then I stroke a check and pay it off after the first month. We don’t do that often, but when we have a situation like that arise, and the discount is extreme, that’s exactly what I do.

She naturally wants to spend like all the other families when she sees it, but when I lay out our financial position and where it puts us when we retire, I always say “we can do it this way, which affords us plenty of things, we just don’t do the dumb stuff these people do. OR we can act like them, but add 12 years on to our retirement age.”

Then I ask, is what we have and do so bad that getting that BMW or Lexus SUV will change everything? Is that worth 12 more years of working when you’re already in your 60s? And she always agrees with me and says no it’s not worth it.

And I always do offer and say we can do it, I just want you to understand what it will lead to. And she recoils and says no we don’t need it. And that’s why I married her! She’s no dummy!!! But I totally understand why she some times gets sucked in by seeing everyone eat out every night and drive fancy cars. It’s just silly to me.

But I’m also the type that turns down gifts. I hate when people buy me gifts for Christmas and my birthday. Anything I get in life I want to get myself. It’s just how I’m wired. Now and days when people try to buy me things on those days I ask them to please by her gifts instead or our kids. They will enjoy it so much more. And I enjoy watching them get excited.

I can’t state how much I dislike people giving me gifts. Even when my coworkers surprise me with a party on my birthday. I always complain to them. In a comical way, but I’m serious. I don’t like getting gifts and I don’t like being celebrated.

You’re a mean one, Mr. Grinch, LOL!

Personally, I would find your arguments compelling. But then I’m a member of the over-the-hill gang and my moments of fiscal insanity are dust in the rear-view.

But how about maybe teasing her with that old joke about a Lexus? How can you tell the difference between a porcupine and a Lexus? ANS: on a porcupine, the pricks are on the outside?

Ditto

That was before they froze your bank account.

‘The wheels on the bus go round and round

Round and round, round and round

The wheels on the bus go round and round

All through the town.’

I follow the logic SD is laying down…basically the risky mortgages composed by borrowers who are actually professional renters, will return and it will be like 2008 all over again.

So this is a way for banks to scoop up housing? In the area where I live, there’s a program advertised on TV where you can sell your house to a company and then rent it back. How do you think that will work out?

I think, in addition to other “benefits”, I think this may be a grift to help banks recoup all the lost loan initiation fees they are not receiving due to a massive decrease in mortgage applications.

In addition to people not being able to afford houses at the high interest rates, the market for people in real estate who want to move up is stagnant.. What’s the point of moving up when you’re locked into a lower rate? You will just be spending more for less house.

Banks are already teetering, and loan originations are a BIG source of income.

Maybe this is a way to give the banks more loan initiation fees. They don’t care many of these low credit people will default because the banks don’t take those losses. The banks’ money is made in the fees earned from making loans. They don’t really care what happens after that.

Rule? This is a tax! It’s not legal unless Congress votes for it.

How passé. What do you think “Justice” John Roberts is for ?

The Chinese Communist Party make the rules now.

Wealthy communists. They seemed to have lost the meaning of communism, or only intend their philosophy for their useful idiots to fleece them. The wealthy communists sure love their money. Equality is only for the unwashed inferior peasants.

The communists are egalitarian and highly materialistic.

ALL Chinese love money, and intelligence. They are a very capitalistic people.ao trying to impose poverty on his people never sat well with them.

Most of our Congress Critters are happy not to have to deal with “laws”. We had better be on their asses about all these tyrannical “rules” that are implemented by diktat, and demand that those lazyass CC had better start standing up to this tyranny.

I am part of a small group of Christian’s that meet weekly and everyone prays for our country, loved ones and many other needs. Perhaps if more people would go to God and ask for guidance, forgiveness and anything and everything else to bring this great country back to what it once was 70 years ago, our country will make a turn from the direction it is headed now and turn it back to the great place it once was all those years ago. When things look the darkest and all hope is lost, He is our ONLY saving grace. It costs nothing but spending time w/God!

George Washington prayed but he also took action. His divine wisdom gave Washington the plan to defeat the Hessians at Trenton which changed the direction of the war in his favor. Praying without a plan of action will not accomplish much. God only helps those who help themselves.

I am not sure I follow this logic; a fee on good borrowers is transferred to poor credit borrowers?

I love this site, but I am not getting it.

You Will, Comrade. You certainly will in the ending. BOHICA

Ordinarily a low credit score buyer pays a higher interest rate. The fee in theory allows the bank to subsidize those bad loans to let the bad borrower to get a lower interest rate.

The reason it is stupid is that those bad borrowers do not suddenly become good borrowers. They’re still stupid with money and will struggle to make payments and default. it’s unlikely to draw more buyers into the housing market. Because stupid people do not become smart people by giving them $40.

who are your sub-680 credit score “buyers”?

recent college grads with no money who have too much debt to buy a house anywaypeople who frequently miss ROUTINE monthly payments like utility bills and rents.IMO what is really going on is that people with higher credit scores take on less debt and are more likely to pay it off early. So the banks need a way to recoup their lost interest charges and this fee funnels money to them. Notice that big down payments – bad for the banksters because they can’t charge as much interest – will pay the highest fees.

We got a construction to perm loan last year at 2.625% for the first 10 years. Then the rate floats in year 11-30. Our solution? After we built the house, we sold the old house and took all the money and put it into the new house. The bank allows an annual recast, so our monthly payment plummeted. If we focus on paying off the house first, our 30 year mortgage becomes a 10 year mortgage at 2.625%…which is basically free money at 8% inflation. The bank will lose out on tens of thousands of dollars of interest charges.

Although this new fee I think is for new loans, by paying the house off 20 years early, we avoid Obama’s “fee” and save ourselves 20x12x$40 = $9,600 in fees. (On top of the interest savings.)

They hate good credit scores because people with good credit scores are getting around the traps set for stupid people in the banking system.

People with high credit scores are being targeted because they’re not generating enough revenue for the banks. So they get slapped with a fee to “help the poor” – people who don’t have the money to buy a house anyway and who will likely default.

I’m pretty sure the fee is collected by the government (under the guise of the “independent” Fannie and Freddie). The bank doesn’t get any of those fees. Likewise the bank doesn’t shoulder the risk of default, these loans will be absorbed by Fannie and Freddie (you and me) when they go bad.

The higher risk borrowers will absolutely be drawn into the purchase market, they’ve been told for years that this is the American dream, that they deserve it, and that rents are “too high”.

On top of that, the stated income loans have been back in the system for a few years already. They are called something else and are set up specifically to attract foreign-born buyers. One type of these programs is that the buyer is allowed to state that there are other people such as extended family members who will also live in the house and contribute to pay the mortgage. The income of those people is not verified, there are no leases nor are those other people signing on the note. In short, stated ability to pay, but not the buyer’s income (ability to pay), some other people not even named who will pay.

There are other programs of course. Freddie has Home Possible that requires minimal written assurance that someone pays rent to the borrower. There are mortgage loans available based on Section 8 vouchers.

WTF?

Yessss…

Wealth

Transfer

Fee

Perhaps but those buyers real wages have fallen to a point where they can’t afford those appreciated assets.

Those fees and rates will also have a negative effect on prices.

People with sub-680 credit scores are generally younger people just starting out and those who struggle to make routine monthly payments. They’re not going to suddenly enter the housing market over a subsidy that drops their mortgage rate from 7% to 6.875%. And they’ll probably default if they try.

The government party hates people with good credit because people with good credit know how to evade INTEREST and how to minimize their tax exposure. People who are good with money also tend to quickly spot the latest bank and government scams. So they must be punished.

People with good credit are freer that people with bad credit. That makes us a threat.

I hope President Trump is mad enough by the time he gets back in the white house that he will finally light the fuse the powder keg.. tired of keeping it dry. Let R Rip! put them all on military tribunals.

OMG! And dumping this much real estate on the market at the same time as rising interest rates is going to cause a steep decline in value of housing.

I think this is the goal of the CCP. Also known as The World Health Organization. Also known as The United Nations.

Isn’t this what caused that last housing crash???

Too many people getting homes they couldn’t really afford and then within years they were under water.

The sub-prime debacle was worse because the government was threatening banks with lawsuits accusing them of racism. So they went bonkers handing out bad loans.

These fees won’t do anything to draw sub-680 borrowers into the housing market.

I take it that the equal opportunity housing program has concluded.

Thanks SD. I did see this news and noted some of the same culprits who also have a hand in the ESG scoring, assigning “wokeness” points to businesses as a means to determine investment potential- Black Rock and Vanguard- another strategy to tighten the vice.

” The Beatings Will Continue Untill Morale Improves “, Comrades

genearly.substack.com

Merriam-Webster will have to add additional definitions for “equity” when used in relation to a mortgage. Sharing your financial irresponsibility with those who don’t know what it’s like to be financially irresponsible. Pay up, sucka!

‘Fannie Mae and Freddie Mac will create a new category of buyers that allows the investors to sell the real estate assets at higher appreciated values and exit their investment.’ – Sundance

This same exact thing happened at the previous real estate peak in 2006, as corrupt Hahhhhhvid lawyer Franklin Raines, former CEO of Fannie Mae, offloaded overpriced houses onto unsuspecting minority buyers:

‘the expansion of easy credit to home buyers with a lesser ability to pay them back was one of the major contributing factors to the subprime mortgage crisis. Raines himself stated before Congress, “In 1994, we launched our trillion-dollar commitment, a pledge to provide $1 trillion in financing for 10 million underserved families before the decade was over … In 2000 … we launched a redoubled new pledge … to provide $2 trillion for 18 million underserved families before this decade is over. … we are one of the best capitalized financial institutions in the world, when compared to the risk of our business … these assets are so riskless that their capital for holding them should be under 2 percent.’

https://en.wikipedia.org/wiki/Franklin_Raines

Right – shortly afterward, Fannie Mae was effectively bankrupted, along with the last clueless minority borrowers who got suckered into Raines’s nothing-down, subsidized-payment scheme.

And now, sickeningly, it’s all happening again, right out of the same old playbook.

George W regime

Biden is going to have to give them down payment money soon:

DR Horton sales order backlog just fell by 44% YoY.

All my life, I have tried to be less sucessful, so that I could qualify for free stuff, but, no matter how hard I try to be unsuccessful, nothing works.

Life isn’t fair.

But of course, not noticing precisely the group which is vastly overrepresented in the string pullers is mandatory

If you do get a mortgage, screw them over by making extra principal payments and pay the loan off years early. Put as much as you can towards the principal. Don’t buy that case of budwieser, put it towards the principal, don’t take that vacation to disneyland, put it towards the principal, don’t buy that new outfit at target, put it towards the principal, don’t donate to act blue, put it towards the principal, cut the cable and put it towards the principal.

You can shave a dozen years off of your mortgage by continuously making extra payments to the principal.

I did that…on my house and on my car. It was amazing the time that came off and the amount of the savings.

I wouldn’t do that because after I buy a house I can’t afford, the govt will need to come up with another program after I stop paying the mortgage. I will effectively be a squatter and the govt will protect me.

Yes, help yourself and screw the woke corporate cabal out of profit.

Who is John Galt? We control our own destiny even acting as only one

They gave mortgages to people who couldn’t maintain them back under Andrew Cuomo’s tenure at HUD, and it resulted in the crisis of 2008. This might be a little better in that they are making the mortgages more affordable, but when the economy crashes and jobs are lost, that will be little comfort. It’s all politics, and big money is behind the policies.

All this talk about “affordable housing” brings me to ask, ummm, what’s the latest definition of “affordable”? I’m thinking that home prices are going to sink at a rate substantially slower than they spiked in recent years. Add to that the complexity of other government goons sticking their fingers in the mix. Just found out about some new building codes that went into place as of the beginning of 2023 over in Tax-a-chusetts. Plans are in place for all new homes to soon be all electric, fossil free, with heat pumps doing the temperature control year-round, taking the place of oil and gas furnaces for heat. Even if you have a gas furnace the homes are to be wired in preparation for all electric. Won’t be long now before fireplaces and wood stoves are outlawed, I guess. All the new homes are to be wired for an electric car charging station, too. All this fancy new stuff, whether you need it or not, only adds to the price of the house. I’ve heard some estimate there’s at least $50-75K tacked on to the price for this year alone for these changes. Well, at least we’re all going to be “green” soon……….’cause we’ll all be living under an “affordable” log out in the woods.

resolute: “Affordable housing” simply means that someone else is paying for it.

There goes the neighborhood.

SUB2 (subject to) – a way to “buy” at 3% rates – he who holds the title “owns” the property.

Liberal Housing Policy for Dummies:

It’s important to get more new home buyers into houses they cannot afford.

It’s important to get more new home buyers into houses they cannot afford so that by the time they accept that they can not afford the purchase they’ve already dumped a substantial amount of money into it. Along comes Mr. Bankster to foreclose on the property, thus allowing those liberal housing types to scoop up the remains at a bargain basement price. During the last housing crash, err, market correction, I think the buzz word for it was a “short sale”. The ones who can’t afford it are putting in the money to finance the downward price trend.

And collect on the full amount of the mortgage insurance on default. Remember how AIG went under?

This is fascinating for me on a personal level. My daughter has an excellent credit score; she is ready to close on April 24 on a property of $300,000+ in a beautiful rural red state area and her payments are less than the rent she is currently paying .in/near a city area.

I’m going to share this article with her but I believe she really got lucky on her mortgage and rate with a closing before May 1st.

Not everyone will fall into the snookered zone, not unlike what we experienced in the 70’s with interest rates north of 10%.

Stay Frosty.

And the bonus is financial operators offload depreciating assets to buyers who probably can’t afford these loans, and end up buying them back at foreclosure/fire sale prices.

My stomach literally clenches up when I think of the depravity of some of our species.

Christ Jesus! This is ’08 all over again!

Prett good overview of this crazy policy:

What could possibly go wrong? Another 3 trillion bailout in 3…2…1…

Do you think for one second the government was going to give all those stimulus bucks and not take it back with interest? Higher prices for autos results in increased money to the government via sales taxes. Same with houses. School taxes are based on property value. Higher prices of food, rent, shoes, clothes, you name it, means more revenue for the government.

Here in Bel Air, MD (a suburb about 40 minutes northeast of Balt, I am competing with people who are paying cash, over list price, and waiving inspections. These are $400K+ houses sold in hours and days. People and companies are swimming in money. People are paying cash for $80K cars. Just too much money floating around out there. I watch idiots pay $9 for a dozen eggs. I watch idiots spend $150+ on a dinner for two. I watch idiots pay $9 for a chicken sandwich.

The government printed $13 trillion the past few years. Inflation was inevitable. To get inflation down, the economy has to grow or the government has to remove the $13 trillion via taxes.

So many people locked in rates of 3% on their mortgages. They can’t sell because they would have to spend more for what they have now and at a higher interest rate.

The reason why some of the richest counties in the US are around DC. Was manufacturing hubs, now it’s big gov$!!

Great post!

There are many folks sitting on piles of cash.

Inflation is real, twenty year old Hondas and Toyotas with 180,000 miles on them are going for $4500.00 (Can)

Two years ago they were closer to 3K

GS was $1.40 per litre two years ago.

Here in Greater Vancouver today it was $1.90.

Canada is swimming in oil, yet they charge you obscene amounts for gas. I visited my relatives in the Horseshoe Bay area in the 80s and I thought gas and beer was expensive then!