Stop looking at the Washington DC Potemkin village; start looking at the financial system behind it that controls it.

You may recently have seen this story:

You may recently have seen this story:

WASHINGTON DC – Homebuyers with good credit scores will soon encounter a costly surprise: a new federal rule forcing them to pay higher mortgage rates and fees to subsidize people with riskier credit ratings who are also in the market to buy houses.

The fee changes will go into effect May 1 as part of the Federal Housing Finance Agency’s push for affordable housing, and they will affect mortgages originating at private banks across the country. The federally backed home mortgage companies Fannie Mae and Freddie Mac will enact the loan-level price adjustments, or LLPAs.

Mortgage industry specialists say homebuyers with credit scores of 680 or higher will pay, for example, about $40 per month more on a home loan of $400,000. Homebuyers who make down payments of 15% to 20% will get socked with the largest fees. (read more)

If you focus on the DC Potemkin Village, you view this move through the prism of Biden’s FHFA creating a policy to favor low-income (nonwhite) voters by punishing stable credit worthy borrowers. That’s what the powers who control the levers, and create policy, want us to focus on. That’s not what is going on.

Biden doesn’t control anything. Biden is a puppet to the multinationals that control DC policy. When Biden was installed, the people who control the money and wealth (Blackrock, WEF assembly etc.), the people behind the Potemkin Village, knew what the larger economic agenda would create.

Biden doesn’t control anything. Biden is a puppet to the multinationals that control DC policy. When Biden was installed, the people who control the money and wealth (Blackrock, WEF assembly etc.), the people behind the Potemkin Village, knew what the larger economic agenda would create.

{GO DEEP}.

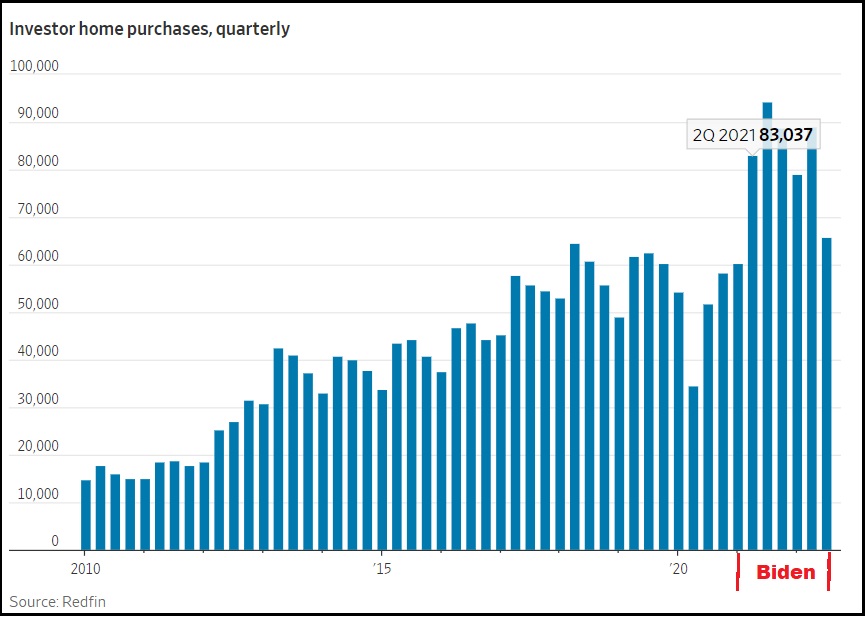

They knew BBB, or Green New Deal policy, combined with excessive govt spending would generate inflation. They moved their money from inflation sensitive liquid and paper assets, into real estate. Inflation raged, liquid assets depreciated, real assets (real estate) surged. 25% of housing was bought with investment dollars by institutional investors, housing prices skyrocketed – their investments increased accordingly.

The financial control operators avoided the consequences of the government policy they controlled.

Now, those same institutions need to turn those appreciated real estate assets into capital outcomes. They need to sell the real estate. However, the assets are now at maximum appreciation and dropping as a result of the central banking moves to raise borrowing rates.

How do they exit the investment? They need a mechanism – a new policy to create the financial instrument that transfers the increased investment wealth back into their hands.

They need buyers.

How do they get buyers? They create new policy.

That’s what is behind this new FHFA rule. Fannie Mae and Freddie Mac will create a new category of buyers that allows the investors to sell the real estate assets at higher appreciated values and exit their investment. They will transfer the depreciating loss of the asset to the new buyers, like a game of hot potato.

Learn to look behind the Potemkin Village to the institutional financial operators who control the laws, rules and regulations. This is all a continual game of wealth transfer and redistribution. There are trillions at stake.

Look at who moves the money around and how they position govt policy for the shifts into and out of the financial system they control. All of this is being controlled, and Joe Biden has no idea what is happening beyond the talking points that are put in front of him.

Shades of the 2008 financial crisis looming on the horizon again. We so need a purge of certain entities from their position of power.

Yes… it’s a vise.. They are on both sides and we’re in the middle.

Currently, low credit/ low down payment loans are about .5% higher in rate than great credit/ high down payment loans. These loan level price adjusters are the mechanism “points” added to each mortgage coupon to give a higher/lower rate. In effect, what will happen is that todays 6.25% 30 year would become 6.375% for the best buyers and the not so good buyers would then become 6.625%, coming down from todays 6.75%. So instead of a .5% spread, it would only be .25%. There is still an incentive to be good credit and high down payments, but not as much.

I have not seen the new llpa price adjustments yet, so this is just a guess from me.

Interesting….

This morning Alex Christoforu YouTube— the first story was a clip of Citibank CEO talking about how Ukraine had to win.

Capital Investments………

I saw his video as well. “…we have to win…” We?!

Saying the quiet part out loud. I’d love to be a fly on the wall when they learn “they didn’t win.”

Meanwhile all of the Biden’s laugh all the way to the bank. Then they give Obama his cut and he laughs all the way home.

Spot on! 🤬

How about,…no one cares.

And that’s the reason they get away with it.

So, once again, the people that are responsible – have good credit, want to put 10-30% down – take it in the pooper again from people that apparently have no responsibilities whatsoever.

Exactly! Except I would say they’re taking in the “ass” again!!! Bend over good credit middle class people we’re from your government and this jab up your ass is for the greater good!

I recall, during the last crash, acquiring some ‘no responsibility’ tenants who got sucked in by the easy money period and lost their upside down house and their ability to borrow. So, they took their stable jobs and very substantial income, downsized, and I used my history of reading credit reports on loan committee at a financial institution to read between the lines and give them a hand up.

They took a like new home I’d refreshed for tenancy and, three years later when they were ready to buy again, left it in essentially the exact condition I’d provided it in. I wrote their deposit check on the spot and did nothing to the house, didn’t need to, and sold it shortly thereafter, seeing the storm clouds gathering in CA at the time regarding tenants and landlords.

This underscores a point I make here repeatedly, that the current situation, economically, runs far beyond ‘irresponsibility’ to government and industry fascism and collusion to damage and destroy the fabric of our Republic for their own nefarious reasons and goals. Sundance posts regularly on this aspect. It’s not ‘stuff happens’. It’s not an ‘economic cycle’. It’s purposeful.

There are plenty of ‘responsible’ people caught up in it and/or damaged by it. Until we learn to work together to defeat the enemy we will continue to lose. We are losing. Dividing and conquering is working. Some of us, myself included, will continue to fight, to the death if necessary. Others will make their own choices.

If you don’t yet own a house, your only problem is that you aren’t being tapped to pay for the Perpetual Dependency class.

Those of us who labored for years to pay off our mortgages, improve our houses, and be good neighbors are paying the equivalent of our mortgage payments 20-30 years ago in LOCAL PROPERTY TAXES. Seriously! We bought a house at way under “how much house we could afford,” with a 40% d/p (first house for both of us, in our 40s), fixed it up, watched our assessments skyrocket and our taxes along with it…and the money all goes to paying for services for people who hate us and want to take our stuff (in their tiny minds’ view of “equity” etc.).

So now what they’re saying to aspiring home owners is, if you are competent you will start paying those taxes early, while your house gains value (in their model).

Meanwhile our very stupid Democrat and GOPe neighbors are all preening about how much their house is “worth” on Zillow. We’re trying to hold down the “value” of our house so some young nice family can afford it some day (we still have the 1980s kitchen–it’s very Comfy and farmhousey, and I hope someone appreciates it not being all that crappy Obama Era grey/metal). There are so many things we dreamed of doing to this house when we bought it, being very tool skilled, but we did none of them because of what the taxman would do in return. We were going to build outbuildings, an addition, etc. Nope.

The entire system is geared to enslave and farm the most competent, hard working, forward thinking, and orderly…and redistribute everything we work for to those who run around wanting to get houses the way they shoplift stuff from WalMart.

This is the same concept for home insurance in the Fl state-backed insurance system.

Citizens Ins. came about after the 04/05 hurricanes, many of the “name brand” companies dropped their buyers here.

Citizens has become very popular, in fact too popular. The “name brands” started crying louder and louder in Tallahassee.

Starting next year many will be dropped by Citizens and have to return to the “name brand” companies if they are with in a set percentage of being higher priced than Citizens.

The sweet kicker is get this,,, Citizens will now have less income so they have sent a letter saying that even though your are not insured by them, you will still be billed for some amount just because you have a home in Florida with a mortgage.

It is looking like it will be best to pay off the mortgage and go naked on insurance.

Just sent in the quarterly payment and looked over coverage, only the structure is covered, no belongings, they want receipts for everything. Not any receipts for antiques, and if the structure fails you couldn’t find them anyways.

The deductible for hurricane damage is $ 30,000 that’s quite a hit to the wallet after paying $ 8,000 a year in premiums.

The thing is for the most part the ins companies don’t pay diddly, have a long time friend that is a long time adjuster I’ve sat with him as he was writing claims, he submits as much as he can/thinks will be accepted, some go through some not, he gets paid on percentage so it is best for him the more he can get approved.

Recent talks with multiple friends are all the same, they are going naked on ins, taking the money that would go to ins company payment and putting it away.

We’ve had many storms here on the east coast and luckily most homes have had mainly minor damage, Andrew being an exception, much of the damage is from tree limbs than needed to be trimmed for many years.

Been doing the ‘naked’ thing for eight years now with this huge symbol of God right outside the window to remind me.

Yep, live in the forest with huge trees around and no insurance. No regrets. Even back in the 60’s my dad, who worked for the state selling workman’s comp (insurance), told me insurance was a ripoff. He wasn’t wrong.

Would take a direct hit by a tornado to damage that tree. And in a forest you will have no tornado…..Rest easy friend.

We often get hurricane force winds on the coast and, normally, being the forest is a huge fire danger as well but coastal rainforest in the PNW is so wet it’s hard to start dead wood with gasoline.

It’s a calculated risk. Everyone is armed, crime is low, if one stays on top of safety and maintenance fire is of very little risk. Enemy action, sure, but then we’ll be at war and everything is on the table then and insurance doesn’t generally cover acts of war anyway.

One thing I like folks to do is add up all the insurance they buy every year. All of it. Including what’s withheld from their paycheck if employed and the value of whatever is provided by their employer. Eye opening.

> if one stays on top of safety and maintenance fire is of very little risk

Where I am, even 20-30 miles outside the urban centers there are stoned/doped hoboes and antifa setting fires in the summer woods, sometimes malevolently. Some follow the I-5 corridor, others have the gumption to get on other roads. There is a degree of malevolence here that absolutely qualifies as demonic.

We get Pacific cyclones in the coastal PNW that are hurricane force, but not named that b/c they come off the Pacific rather than Atlantic. Inland, things get very dry and droughty in the summer, and with the antifa types and hoboes allowed to run free, fire is a bigger problem.

The biggest problems is when the CA and other urban carpetbaggers move in (muh bugout), buy 5-10 acres, and clearcut them to plop down their 5,000 sf McMansion in the middle (complete with 50 million candlepower lights, because they’re afraid of the dark). The patchy clear cutting amplifies winds and creates swirling drafts that cause chaos all around, for literally miles. Solidly layered healthy rainforest can absorb an incredible amount of wind, and what comes down in a 70-120 mph wind is generally old old growth ready to feed the soil.

Here is Alabama Insurance is king…….been without insurance for about 15 years and you are right the deductible is so high you would end up paying out of pocket anyway. Been through 10 Hurricanes in my home. Flood is another rip off. After Hurrican Ivan the insurance companies left in droves. They have slowly come back. I carry fire and theft only and get ripped off as well. Switch companies for a reasonable rate only to have them increase year ly around $200 . It has become a game. Alabama has done nothing to control them. The 2 counties closest to the water pay for basically the entire state in premium increases. Had a study done almost 10 years ago showing most of the claims money wise are paid out north of the 2 counties that are covering the losses.

For how many centuries did ‘insurance’ not exist on the land that’s been on the planet for billions of years.

How many of us have spent hundreds of thousands over the decades and never made a claim? I raise my hand.

One benefit of not having a mortgage is not having to buy insurance. It’s a choice. Why are people afraid? They’re afraid the legal system, the most corrupt system in the Republic, is going to bankrupt them. That’s how effective the lawyer scum have become. It’s nothing more complicated than that. Lawfare aimed at draining the assets and sweat of everyday people under color of law, with bankruptcy, imprisonment and death as the ‘sticks’ to ensure compliance.

Make different choices. Give them and their ‘enforcers’ the finger, and more. Someone famous , or perhaps infamous, once said a little revolution now and again is a good thing. Was it one of our founders? I don’t remember.

I agree, and for many, Insurance is a lot like Credit; people think “Well, you just HAVE to have it, EVERYBODY does!”

START with what “everybody does”, go 180 degrees, and it gives you a good starting point, and this applied to many major life decisions.

I am “naked” on health ins., although I have part A only medicare, cause can’t opt out, and costs me nothing.

On auto, paid cash for vehicles, so carry only required minimum liablilty, but type of vehicle and my driving style make it HIGHLY unlikely I will get in an accident, even more unlikely if I do that it would be deemed my fault, and extremely unlikely that I or mine would be injured.

I pay less for Insurance on my two vehicles, per year than my neighbor pays per month, for his “newer” vehicles he is still paying on, and so required to carry “full coverage” insurance.

I have $ truly ‘left over’ every month, and $ “in the bank”, for him? Flat broke the last week of every month, and our incomes are comparable.

Think “outside the box”, be creative and recognise you don’t HAVE to do “things” a certain way, just because “its what everyone ELSE does!”

If people realise the premium they pay for the ILLUSIONS of prosperity, security and convenience, and not only in terms of $, but in terms of STRESS, they would make very diffferent decisions.

YouTube is promoting this video about the homeless in CA.

The suspicious in me says that they’ll be pushing for “Public Housing”.

That’s how they operate, create a problem, make it worse and then, present their solutions.

The reason for the all of the Homeless in Ca. is and has been the result of having DEMS control that once beautiful State. Until they get rid of the incompetent leadership in that State it will get worse.

And they’ll move them into the suburbs with the illegal immigrants

Whom Ronald Reagan brought in, turning CA blue forever.

Massive Section 8 housing projects and mass transit are the Democrats solution for every housing crisis/problem! Pack them in tight and restrict their travel options via mass transit! Viola freedom of movement is gone!

I remember, after Covid started, Newsom had a bunch of new travel trailers brought to CalExpo and set up for the homeless. Funny how few if any stories about any homeless moving into them ever surfaced. It all just kind of went away.

Same with a jail in Oakland that was converted, supposedly, to homeless housing. Big hoopla, then no follow up with smiling homeless getting a nice climate controlled room with all the features of home. Whenever I checked, zippo.

Homeless IME are often that way by choice. They hate the system and anything having to do with conforming, whether they’re mentally competent or not. I worked among them back in the 80’s and that was my takeaway and I doubt much has changed.

I was asked to join the Homeless Commission in N. Marin County. I said yes. Providing that we spend no money on people who had intractable drug habits, and would not deal with them. I wanted to help those who just needed a hand up … Usually families.

Of course, that was ignored, the commission was filled with very wealthy “Do-gooders” who would never actually go to meet the homeless.

I gave up after a couple of useless years. Sigh.

Wait, my brain can’t absorb this level of evil. So they are purposefully targeting low-income Americans to buy homes they know will depreciate in value in the near future? Those poor families!

Not the first time we’ve seen evil in the industry. Last time around there were low down payment/no down payment notes written to get people into the game. And for those already paying a mortgage there were the home equity loans at 100% to 120%+ of the home’s value – the home’s value at that moment, that is. One burp in the market and Mr. and Mrs. Homeowner are so far underwater they have no choice but to walk away if there’s any glitch in their income. Any equity is lost, but more importantly what’s also lost into the system is all that interest paid on the note that the banks get to keep.

That was a system playing on the mortal sin of greed. Anyone who was greedy in that feeding frenzy got themselves in trouble.

SD’s current piece is about taxing the competent, forward thinking, hard working borrowers to pay for the worst possible base of house buyers–those who can’t even manage a checking account and credit card, and have no hope therefore of the complex and disciplined activity required to own and maintain a house.

Well at least they don’t do that with cigarettes and lottery tickets.

Not poor, lazy and stupid. And you’re excusing it with this comment.

Anyone can learn the basic arithmetic behind this stuff. But people who spend more time posting ‘dos and kicks on social media aren’t going to have or take the time to learn very basic facts.

My dad had only an 8th grade education but sat me down at age 10 to show me how mortgages–and all interest-based debt–worked. And he was way poorer than today’s low-income Americans who have all sorts of gibs, from air conditioning and smart phones to free training, schooling, transportation, food programs, etc. What he taught me about how interest works, and why debt can be enslavement, served me my entire life. Of course he was one of those dads who actually bothered to raise his own kids, and be there at night to teach them things.

I smell the MBS tranche bundling (fraud anyone?) all over again, where people who couldn’t even speak english were allowed to obtain a mortgage w/o their signature…. lawlessness is always abt wealth xfer. Illegal much?

Not so sure about SD’s analysis. These are mortgages, not outright sales. The lenders are still holding the risk of an underwater loan to a risk+indifferent borrower.

Maybe that would be stage 2 where (just like Clinton & Janet El Reno did) banks will be forced to make, sure to default, mortgages under threat of criminal indictment by the G man.

Not really. They bundle the mortgages in with good loans and sell them on a secondary market. The risk of individual foreclosures in the bundle is diluted. Once they sell off the loans, their risk is zero.

I have one question how are they going to transfer the wealth back to them selves when they are destroying the very people that are going to buy the house or apartment.

They are creating massive unemployment along with devaluating the currency, so how exactly are they gonna get people to buy the houses?

I think it’s called a bailout from the Fed government! The “too big to fail “ argument! It’s all rigged they won’t lose but the middle class will!

This will lead to federally owned housing…. we’ll all end up becoming renters…..this first….then they go after existing homeowners. Then we all become renters with Uncle Sugar in Mordor-on-the-Potomac as our landlord.

That’s the goal.

Federal Housing

Federal transportation

No homeowners

No car/truck owners

EVs will be too expensive, so government transportation will be the “only answer “……

Stalin will seem like an angel compared to these commie-pinkos in the WEF-controlled Republicrat (or is it Democrublican) party.

Yup! That’s the “equity” part of DEI! Liberals are the most miserable people on this earth! They want us all to be equally miserable like they are!

an employee poll just posted by a large recruiting firm shows that 55% of workers believe DEI to be divisive… get woke, go broke. It shows that with this in place, stress has increased daily while productivity has decreased.

Think USSR before the wall fell. That’s how the majority of Russians lived….mostly the middle class.

Yeah, it was pretty rough to see educated, hard-working people living in comparative abject poverty. Saw it first hand in the early-mid 90’s in the FSU.

Will we be as resolute if/when Communism, 21st Century version, takes full effect here? IDK. We’ve had pretty easy lives for the most part.

Somehow, at SOME point, THEY will have gotten as far as they can thru incrementalism and “soft tyranny” and will have to figure out a way to transition to HARD tyranny.

This applies to 2A, and everything else they are doing.

As near as I can see, this CBDC is the path they HOPE to use, in order to have the tool they need to force compliance, and maintain control.

After all, if they CAN simply turn of your “ability” to engage in any commerce, they can, or THINK they can, force you to comply with ANY mandate they impose.

WE must fight CBDC, every bit as much as we fight for 2A, it must be our “line in the sand”, and any moves we can take now, in our lives to withdraw from the system, set aside (stockpile) means for surviving without commerce need to be explored.

My consolation is, NOBODY has EVER attempted what they are now attempting, certainly not the WAY they are attempting it.

I am not at all confident THEY can succeed, and I don’t think THEY are, either. They can NOT stop, slow down or reverse coarse at this point; THEY must proceed “full speed ahead” even though while they know what they want their destination to be, they are unsure of EXACTLY how to get there, and the path is full of many hazards; one mistep, and they are doomed.

A bit hyperbolic in tone, but I agree in principle/framing. A rentier economy–revived serfdom–is EXACTLY what Globo wants. And the only way to get it is to destroy anyone who has the intelligence, work ethic, discipline, etc., to build wealth as free men.

This is a literal war on everything my Revolutionary War (and prior) ancestors hoped to build with this republic: a place where people like us could come and be free of the Dolt Wranglers and their Clod Farming operations, overseen from their gilded towers.

The State becomes “the Company store” model.

State is your landlord, employer, banker, and “you will OWN nothing and be happy” or else.

Has a familiar “ring” to it, like a repackaged version of the Conmunism of the Soviets.

It is NOT ozero. He was never that smart or capable. Sundance ID’d them: the institutions that control the money and wealth.

This is a great point. Unlike a Bond Villain… the real evil in our society stays quietly in the background, never directly showing their faces, and uses puppets to front their work (and take the gallows should they go a little too quickly).

And so it will remain until the Biblical end of days.

Yes, and Obama was selected, in part specifically to BE a figurehead, that so many would mistakenly focus their anger on, thereby failing to see the “man behind the curtain”.

Just like the scene from Oz, a big head, with lightening bolts, loud commanding voice, all an artifice to keep anyone from noticing the little man behind the curtain.

Sundance is like Toto, pulling back the curtain.

Despite Sundances detailed analyses, “bringing the reciepts” to expose whats behind the curtain, we still see FAR TOO MANY comments from people who allow their EMOTIONS to overwhelm their logic, and so harping on “its ALL OBAMA!”

In a fight for your life, emotions get you KILLED, not ‘MAY”, not ‘CAN’, but 100 percent and every fricking time WILL get you KILLED.

The proverbial “man behind the curtain”

Friends of Obama.

“Born in Kenya” Obama was no stranger to shenanigans in the real estate and mortgage crises and the $11.6 Trillion stimulus bailout that he created.

In the 2008 mortgage and financial crisis it was said that Democratic Party + Fannie Mae/Freddie Mac x Obama + ACORN = financial meltdown

https://www.americanthinker.com/articles/2011/12/obama_and_the_financial_criminals.html

… It is now known that Fannie and Freddie, the government-connected mortgage-packaging giants, threw out the qualifications to allow home-ownership for all, an idealistic social goal pushed by Democrats — from Jimmy Carter via the Community Reinvestment Act of 1977 to Bill Clinton in the 1990s, who enlisted ACORN to badger banks to make bad loans to minorities, and then to Rep. Barney Frank and his fellow travelers in the 2000s, who put the full weight of the Congress behind the creation of bad mortgage loans.

The large investment and commercial banks saw an opportunity and concocted securities backed by dicey “sub-prime” loans, in which borrowers paid higher interest based on questionable credit. These mortgage-backed instruments were a hot item, yet when the banks learned that the underlying values had vanished, they lent money to mortgage origination firms to gin up even more bad loans at higher and higher interest rates to shape into even more mortgage-backed securities to sell to their customers — and each other.

Right there criminal fraud is manifest, contradicting Obama’s claim that the scam was legal. But there was more. The banks, knowing that the instruments were worthless when they sold them to their own clients, purposefully bought “insurance” (credit default swaps) against their own products, thus doubly swindling their customers. And they made millions doing it — first on the commissions from the sale, and then from their short position as the securities tanked. In 2008, the house of cards came tumbling down, taking with it the American economy.

Then enters Treasury Secretary Hank Paulson, formerly chief of Goldman Sachs — the ubiquitous investment banking firm that has left fingerprints all over the meltdown — who insisted that we must save the hides of the big banks (his compatriots) with the stimulus bailout to “rescue the financial system.” Originally stated to be $787 billion, the total, according to Bloomberg research, reached $11.6 trillion — all secured by American taxpayers. The result was the near-destruction of the consumer sector, which represents 80% of the economy, all to save the criminals who committed the illegal acts that brought down the economy. But worse, commercial and community banks are still burdened with bad real estate loans and investments. Consequently, they are under orders from banking regulators not to lend, which further exacerbates the decimation of the middle class and small business owners who cannot find loans to recover and grow.

… Obama and his cohorts — like Paulson, now replaced at Treasury by Timothy Geithner, another investment-bank rent boy — have not only failed in their approach to the recession, but they may be the architects of an economic calamity more painful than the Great Depression when all is said and done. The European Union debt crisis is just one of the continuing manifestations of the global economic crisis set off by the American financial scandal. Add in the inability of real estate values in the U.S. to recover, and unemployment figures that boggle the mind, and the worst is yet to come.

Remember….those that bought and got caught up in all the foreclosures…..many willingly stopped paying notes because their investment lost 50% …..why keep paying? The Banks refused to wright down the principle to make up for their caused loss. The Banks prefered to go through the foreclosure process than work with the buyer…Meanwhile the taxpayer bailed the banks out.

Sounds like taxation without representation ang highly illegal.

With selective interpretation and enforcement and ‘discretion’, anything can be legal, or illegal. Pretty cool, eh?

Looks similar to redlining in reverse.

It is reverse redlining. Earlier this year biden had low income areas getting lower rate loans in certain parts of the country. Even though the areas were 90-95% black, he was able to say it was not race based as he made it for the area, not the color of the skin.

These policies are coming from same the people who call appraisers racist for using comparables in the neighborhood when appraising. They have actually suggested that when appraising in poor black areas that one needs to go outside the neighborhood to white areas to get comparables for the appraisal.

That’s in complete violation of appraisal rules! And ESPECIALLY FHA/VA appraisal rules! Wow!

I’m shocked. So, the people who’ve worked their arses off to keep those great credit scores by paying their bills on time and being responsible are now to be punished.

One of the first things that came to mind was they are still trying to stop The Great Migration from blue states to red states. They had to get creative. As I recently shared, people are still moving from blue states to Tennessee, in droves, which is keeping prices up and inventory low. I know this because the well driller told me they are busier than they’ve been in 30 years.

The only way to purchase without being penalized is to pay cash or to purchase far below your means that the extra fees won’t hurt. Although, people “with money” won’t care about the stupid fees – they just want out of the crime ridden, high taxation, states.

.02

There are no red states.

Just states where people like us go, and Globo eventually catches up. Because Globo cannot create anything on its own, can only parasitize what the likes of us create.

Everything they do is about the destruction of anyone that works hard and is responsible. They can’t wait to get the entitled and irresponsible in to the suburbs and rural ares. They drool at the thought of spreading the Democrat inner city blight to the safe and clean areas.

When the real estate assets are sold, where will the money be parked? The reason the big boys went into real estate in the first place still exists.

You’re brilliant in these financial matters, in following the money. God Bless you, Sundance, and thank you.

The next logical step in a shell game like this would be to manipulate another sector of the economy to receive the funds from the sale of real estate. This must already be under way if money is being moved out of real estate.

So I’ll just start buying everything I’ve ever wanted so i can dump my credit score below a 680. Done.

I can spend and be irresponsible as well as the non whites out there. What happens when all the responsible people don’t the same thing,…

D u h

If this isn’t treason to this country, i don’t know what is. Purposely breaking the middle class is an act of war. NEVER did i think something like this could happen here.

Where were you in the 1950s when middle class Americans were being forced at bayonet-point to accept the demographic invasion and monetary redistribution policies of their overlords?

Where were you in the 19-teens to 1940s when middle class American men were being genocided via the war drafts so that Globo could flourish with its wars and resettlement schemes?

All cash buyers, wealthy foreign and domestic individuals, will not pay this tax?

All on the middle class households .

They will be able to buy a home but will not be able to maintain it.

The homes will fall apart,

grass and trees will not be maintained, car’s parking on the lawn in numbers, and property in these neighborhoods will upset and called racist against poor people of all races because they care about their neighborhoods and don’t mow their neighbors grass when the cars are not parked in the yard out selling drugs or protesting.

Just another hidden tax on the middle class. The rich either pay cash or buy homes with LLCs.

Yes, it is the people in the shadows. It is always the same people. This is a win/win for them. They get what they want monetarily as usual and more

Important for them, it drains white people of wealth and redistributes it to non-whites. The parasites love their money but they love destroying white countries even more.

Question …if they moved their money out of liquid and into real estate …because of inflation…..where would they put their cash out of the real estate? Inflation is worse now. I thought their goal was renting their properties.

Despite the Loud protestations of “We will make sure this never happens again” when they passed the Barnry Frank legislation after 2009, many pointed out the legislatiin did NOTHING of the kind, anf just made the TBTF banks bigger.

These “new rules” are simply reestablishing the same conditions that caused 2009: banks giving out loans to people that could not possibly afford them, and the results are easily foreseeble.

They are working really hard to destroy “The American dream” of ownership, and replace it with “You will own nothing and be happy”.

I see no way for individuals to avoid this trap, they are building into the “game” other than to refuse to play.

Signing on to CREDIT, is like signing yourself into a mental institution; you can enter any time you like, but you can never leave.

Except you CAN. For a long time, a relatively small # of borrowers, have used credit “responsibly”, paying their balances every month, etc.

Credit companies refer (internally) to these customers as “deadbeats” as the credit card companies make nothinh off them, getting all of their profits off the “pay the minimum balance” majority.

Now, as in other areas, THEY are once again looking to screw those who “do the right thing”.

“In the BIG picture” I have no idea what “the answer is”, frankly.

On a PERSONAL, individual level, getting off of the credit trap, like getting the hell out of the big cities, just seems like a sensible, self-interest survival instinct move.

Both require a basic adjustment in World view, and a major re-ordering of priorities, which all starts with “Get right with God” and submit to HIS guidance.

Focus on what you NEED, and let go of what you WANT, accept HIS guidance and tell Satan “get behind me!” when he whispers in your ear.

I’m a “deadbeat”. We have a Costco executive membership with a Costco credit card. We use it to pay everything all month long (and I mean EVERYTHING), and then pay it off in full. We get cash back every year of around $1200 after subtracting the membership fees. It’s a nice little money maker.

Same for me.

We let our Costco membership go because they were mask fascists.

Costco can bite me.

paid off my house because no longer can claim interest. I am worse off since the tax reform.

Yep. Trump’s tax reform.

https://www.express.co.uk/finance/personalfinance/1760901/global-house-price-crash-UK-property-market-meltdown-housing

Yep! He was promised big money, which he got, even his two friends that he borrowed the two children from got rich, they all got rich, that’s all there is to that story.

This must be the reason the stock market is up. The institutional investors are moving the profits back in to liquid and paper assets. So my question is are they going to move their assets back into real estate once price move down and foreclosures begin climbing or somewhere else? I did not comprehend what Sundance was talking about back in January 21, otherwise I would have gotten more aggressive in the real estate market.

This rule will have disparate impact on whites and Asians who have high credit scores and lower debt to income ratios. Since we’re always told anything that causes disparate impact is bad then this should be struck down in federal court.

If this is allowed to stand then it will artificially create new home buyers who will eventually default on their home loans similar to what happened with George’s W. Bush’s subprime loan scheme to boost home ownership among minorities. It caught up with us in 2008 and crashed the economy.

As usual, Sundance is spot on. He succinctly describes the real reason for this policy implementation . But, to me, equally aggravating is the given reason published by the opinion makers that this policy ensures racial equity, an abominable and unconstitutional construct that elevates equity of outcomes over constitutional equality of opportunity.

Wasn’t it trump who capped the mortgage interest deduction to 10K?

No, because there is no $10K cap on mortgage interest deduction. Interest paid on the first $750K of mortgage debt is deductible. If you bought before Dec. 16, 2017, the interest on first $1 million of mortgage debt. No limit

The $10K cap is on deduction of state and local taxes (impacting those in high tax states).

This will fail because smart consumers will find ways around it. For example; instead of putting 15-20% down they will put 10%, buy down the rate, and save another 5-10% to immediately pay down the principle once the loan is closed.

Mortgage companies will also offer products that skirt around any of these fees. The people proposing this have no clue. It’s just like a city imposing a sales tax. people just go to another city and the city with the sales tax ends up with less even though they raised the tax.

Buyers will also negotiate tougher with sellers knowing the market is dropping, further dropping the market prices.

A point I see being missed:

People who can’t manage a basic financial life–checking and credit cards–to get a solid credit score aren’t going to be able to manage/maintain/improve a house.

Why would Big Finance want to turn loose on existing housing stock incompetents with no work ethic, no forward thinking, no discipline, and no ability to maintain anything? A credit score is a measure of how well you manage money, and that is a proxy for how well you manage all sorts of things. It is the tip of the life-competency iceberg.

I can’t think of a more devious way to engineer a wrecking crew for housing stock that Big Finance wants to see gone…so they can make tons of money redeveloping it. With more gubmint bling (“programz”). The only way they can do that is by driving these houses into the dust–as they’ve done in beautiful old cities all over the US–then bulldozing them for clapboard Revit-designed cookie-cutter inflatable neighborhoods, complete with the prerequisite cookie-cutter franchise business district.

Also, by getting these incompetents into mortgages that they have no hope of ever being able to amortize, on houses that will crumble under their occupancy, Big Finance is assured of X years (and I’m sure some savvy quants have numbers on this) of interest payment (the first 0-7 years of a 30-year mortgage being nearly all interest payment).

Then the mortgage holder will default, the banksters get a bailout, and more mortgages get ginned up, resetting to the front of the interest/principal curve.

This is not an economy. This is a total BS shell game in a mob-owned casino.

They well know that there is a significant portion of the population–and growing, under their own policies–that are basically failed humans in need of constant, expensive custodial care.

But Big Finance keeps honking on in its PR garbage about the culture and lifeways of competent, intelligent, hard working people.

The next thing you know, the Dumb Ass Administration will mandate that homeowners without a mortgage will be required to pay a monthly fee, likely higher than the numbers discussed in the article. These loons are EVIL to their very core. Please tell me what sense any of this makes. Then again, it comes from the no sense Dumb Ass Administration.