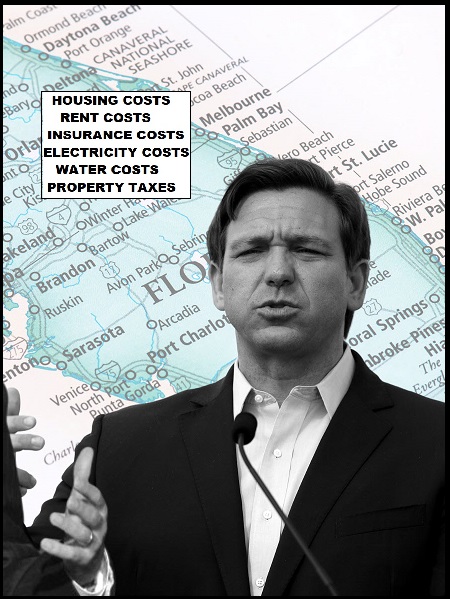

The insurance crisis in Florida is hitting the middle-class family, working community and retirees on a fixed income directly. Hundreds of thosands of residents have lost insurance coverage, and even more have seen policy premiums double. It is not uncommon to find homeowners who are paying more for insurance than their actual mortgage payment. Unfortunately, the situation is getting worse.

Farmers Insurance has notified the state they are pulling out of Florida, will not be writing any additional policies in the Sunshine state and when existing policies expire, they will not be renewed. Home and auto policy rates have already doubled in many areas for many people.

Farmers Insurance has notified the state they are pulling out of Florida, will not be writing any additional policies in the Sunshine state and when existing policies expire, they will not be renewed. Home and auto policy rates have already doubled in many areas for many people.

The insurance situation is becoming more unstable by the day, and the future outlook seems even worse amid reports that even more companies are planning to exit.

FLORIDA – Another property insurer is dropping coverage in Florida.

Farmers Insurance will stop writing new business and not renew its existing “Farmers-branded” automobile, home and umbrella policies in the Sunshine State, the company said Tuesday.

Last month, Farmers said it was only pausing new business in Florida. The company is also limiting new home policies in California, where it is based, according to news reports.

“This business decision was necessary to effectively manage risk exposure,” the company said in a statement.

The move will impact 30% of the company’s business in Florida, or roughly 100,000 policies. Policyholders affected by the decision are required to be given 120 days’ notice that their coverage will not be renewed.

Farmers on Monday sent notice of its plans to the Florida Office of Insurance Regulation, which is reviewing it. Insurers must give the office 90 days’ notice if they want to discontinue writing business in Florida. (read more)

The insurance company withdrawals works in concert with investment groups who prey on the outcome. Single family homes and even large condo developments are squeezed into a situation where housing is no longer affordable. The investment vultures then swoop in and end up controlling the properties.

Florida’s working and middle-class is being destroyed and a divide between the haves and have-nots is being created. The wealth gap is expanding as families are forced to leave the state and a larger percentage of self-insured rich people move in.

Long before Ron DeSantis became a potential presidential candidate, and long before Hurricane Ian devastated southwest Florida in 2022, I was highly critical of state policies that were not constructed around the backbone of the economy, the working class. Temporary H1B Visa workers replacing permanent residents as a workforce to fill the gap is not a long-term solution.

When you stop paying attention to the economic systems that support a sustainable service and production workforce in Florida, this snowballing outcome is predictable. None of it is good. Unfortunately, as I forewarned prior to the COVID era, Governor Ron DeSantis is creating a class-war tinderbox. The sentiment on the ground is increasingly growing angry. His absence is only making it worse.

“My Tribe“

As you noted, it’s happening in CA as well. Because of the fire risk. Interesting how these huge “mega” fires are a recent phenomenon. An agent recently told me the policies are being dropped, then the State of CA comes in and insures them by fleecing them.

In my opinion, just another tactic to make us all permanent renters.

Met a middle aged couple last weekend that told a terrible story about how their house burned down and the insurance company would not pay for any damages.

Why?

Because part of their roof, a part that was between two new additions, was too old, so it voided their contract.

Don’t know if details like that were in the fine print of a 70 page policy and missed upon reading, but I’m guessing we all have ‘gotcha’ items in our policies.

Remarkable how “they” are working so hard at making sure the middle-class lose as much as possible the older we get, including the medical industry stealing any wealth someone has by finding “something wrong” during a routine health screening.

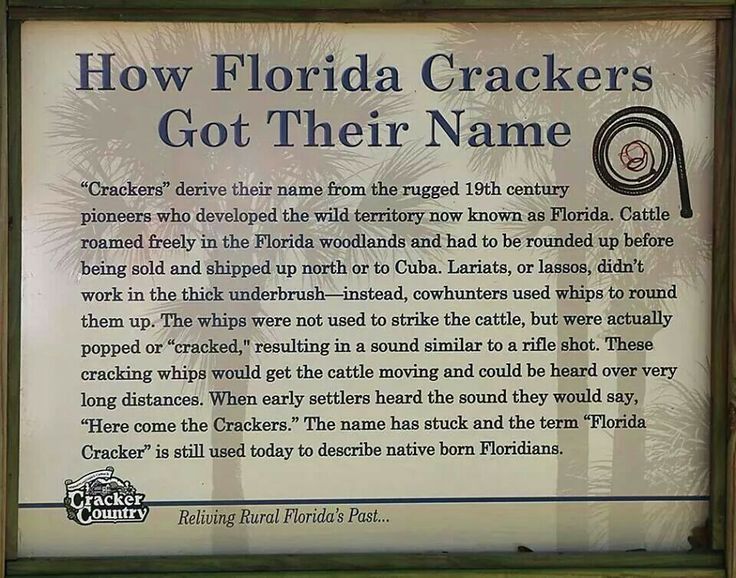

Love the history regarding Crackers.

Georgians drove their cattle into Florida to feed, rounded them back up and returned to Georgia.

Most of our cattle got driven to Punta Rassa for export..prior to and after the war.

Back in the early ’70s Michael Johnson wrote and sang a song titled ‘Cain’s Blood.’

In it are the words, “Half of us want a revolution, they’re gonna burn this country down, half of us wonder who’ll be here to fill up the hole in the ground.”

Burning the country down seems to be a theme with the leftist radicals for a long time. . .

Regulatory Taking. A strategic weapon in the war on America’s middle class.

Fire. Storm. Flood. Hurricane. Wind. One hammer on the construction and permitting side. The other hammer swings from the insurance side.

Add a touch of inflation, then the elite collect all the chips.

Fascinating analysis, sDee!

As I read this and the COMMENTS it stirkes me it’s all symptomatic of what we have and continue to be willing to put up with. As an aside, the Friends of Ron DeSantis PAC has taken in just under $4.0M from Florida insurance industry as of 29 May 2023. Additionally, his PAC has received $9.5M from Florida Power & Light aka FP&L which is a subsidiary of NextEra (NYSE: NEE). I lived in FL. years ago and moved years ago and still have family there mostly in Pinellas County, but I’ll let those who still do detail what happened to their (these) respective rates. DeSantis is of course not the only elected official who takes donations from public utilities or any other.

accumulation by dispossession

what happens to home loans without insurance?

does that break the terms and conditions of a loan?

Yes, it does. The lender will then “force-place” a policy on behalf of the borrower, and it usually costs more than ins that the HO would get in the open market.

It’s a lose-lose.

People find another different insurance company.

Farmers kept increasing my home and auto insurance and I canceled with them and found a better insurance company with same exact coverage and saved $560 this year on premiums.

which company gave you a better rate than Farmer’s?

What will the ‘elite’ do with all those ‘chips’? There are Buyers?

Rent them back to the serfs.

Isn’t that the truth!

Disturbing how what should be a basic discussion about business models and fiscal viability instantly descends into political rancor. That said, if a private insurance company projects that they cannot profitably sell their product at an acceptable price to cover an area due to the natural inherent, and unchangeable risks associated with that area, from a strictly fiduciary stance they will with draw. It is not unlike the many retailers pulling out of the urban crime centers as government sanctioned theft make profitability impossible. Now just a bit of politics. The various, unconstitutional government insurance programs distort the markets as they have the ability to steal money at the point of the IRS gun to subsidize the high risk area off the wallet of those who do not live there. Like most Americans I have no love for the necessary evil of the insurance company but State Farm does not have the ability to send a swat team to seize their premiums like Feral Government does, is, and will do more of with the 4 Divisions of new tax harvesters both parties just gave them..

I’m not an insurance underwriter or EVER worked in an insurance business. But part of their analysis is always to appropriately price an premiums at a level commensurate with the risk of a catastrophic payout event. If indeed the “premiums’ being charged are higher than one’s 30 year mortgage, it seems to me that the insurance company deems the property is likely to be subject to a catastrophic event more often than the 30 year term of your mortgage or that the replacement value of the insured property far exceeds the original value of the mortgage.

When the state insurance commisioners start leveling charges of price gouging etc about insurance premiums, the only choice left to insurers (who can’t recoup its payouts/costss in its premiums) is to leave the state. The state either needs to allow the premiums to rise and fall as required OR demand houses be built to a higher standard minimizing the potential damage. Or beef up regulations on land developments adjacent to wetlands, beaches, lakes and low-lying areas. But in Florida THAT is where people want to build. A combination of sky-high insurance premiums and/or building restrictions will help solve the problem. So will improved roofing standards and building codes…but it will increase the costs of construction for consumers.

I HAVE worked in the insurance industry and you are exactly right. The money has to come from somewhere to pay for the costs of hurricanes, wildfires, mudslides, floods, tornadoes, etc. The higher the risk that your home will be damaged in one of these natural disasters, the higher your insurance premiums will be – if you can get insurance at all. I have friends who lived in Hilton Head Island and after their home was damaged by two hurricanes in a row their insurance company dropped them and said they would no longer insure homes on the Island. Why should people in the mountains of Tennessee pay more in premiums because people in Florida live in a high risk hurricane zone? But they do. I live on a mountain in North Carolina. We’re lucky to be able to get homeowners insurance because we’re in a high risk zone due to the fact that our fire department is all volunteer and is located about ten miles away; there are no fire hydrants within a 30 mile radius; and in the event of a fire the fire department has to bring the water with them.

The job of an insurance company is to assess risk and either decline coverage or price it commensurate with the risk. This news about Farmers pulling out of Florida makes me also wonder if the Florida Insurance Commission caps the rate of premium increases.

This. Exactly what I do but in a very technical niche field of insurance.

Great question regarding premium increases.

A lot here are rallying against insurance. Most don’t understand- without the car insurance- no loan (unless you can prove you can pay off your car- only thing legally required 3rd party liability coverage).

People on the right have a tendency to fly off the handle without taking the time to actually looking at the why. As long as it something/someone they do not like they will rant.

🤡💩

Sounds a lot like the people on the left, doesn’t it?

” OR demand houses be built to a higher standard minimizing the potential damage. Or beef up regulations on land developments adjacent to wetlands, beaches, lakes and low-lying areas. But in Florida THAT is where people want to build”

Exactly, very well articulated. NOBODY should be able to build homes in certain areas, millionaires or not.

Tourists often admire the views of European coastlines while on vacation. Many are unaware how restrictive the zoning can be, nobody is allowed to build homes at a certain distance from the shore, even if one owns the land. It is a constant battle because the big building companies and conglomerates are constantly pushing for less regulations, scandals involving bribes to local politicians abound etc…

It’s not just in FL, it’s also in the northeast. My parents bought a small house on the CT shoreline in 1950. At that time it was “the wrong side of the tracks”…not a desirable place to live. There were a few houses up the street but elsewhere it was salt marsh and marinas. Now, that same small house was gutted to the studs and completely renovated by the new owner, who lives in it only 2 weeks out of the year. There are McMansions and the marinas have greatly expanded. It is now a very popular location in town…hurricanes and coastal flooding be damned. FEMA rules have to be followed and homeowners insurance requires storm shutters. Towns increase property taxes not just for having waterfront, but also for a “seasonal water view”. The wealthy elites can afford all that.

When our society was agrarian based, folks wanted land suitable for farming. That is no longer the case.

Excellent point…I’m no expert, but from what I’ve seen of much Florida housing, it’s very cheaply built…

Have you ever seen a tract McMansion built? Lol

“…at the point of the IRS gun to subsidize the high risk area off the wallet of those who do not live there…”

What you are writing is quite important, for instance, homes and entire neighborhoods that are periodically burn or flooded (as in California), rebuilt, and the cycle starts again because badly defined and enforced zoning codes. And is it not a question of pricing out the Middle and Working class, NOBODY should be allowed to build homes there.

Exactly. A lot of misunderstandings here.

It’s the government interfering that causes this.

It’s a combo.

Word on the street is that reinsurance companies are upping their fees 50%. The large reinsurers cover all types of insurance; home, auto, life. Part of the problem is the bond market. Reinsurance invests premiums in bonds and then makes a sliver of a profit between the return on bonds and what they pay out. Another part of the problem is the “unexpected” increase in deaths to things like the clot shot and such. It’s causing the reinsurers to go in the red, which means they raise rates to stay in business. A rise in the reinsurance rates means a rise in insurance rates for home, auto, and life. It is what it is.

Well, if their bond portfolios are losing value everyday like the bank portfolios are, that does not bode well for their ability to cover future losses either.

Exactly, thus, it’s not rates being increased, rather, they are not providing as much capacity.

That’s not how re-insurance works. Re-insurers typically cover the top level of the coverage. Direct insurer is responsible, depending on re-insurance contracts, for the first so many levels of coverage.

Re-insurers help minimize the total exposure of the direct insurer. Re-insurers buy in with what they are comfortable with for the type of coverage.

Word on the street also said Trump colluded with Russia- be wary of the word on the street.

If you took the death jab…you should have to pay more for life insurance.

gentrification…it happened in hawaii…it happened in florida. this is the main reason for problems in florida…and hawaii…

the typical middle class homeowner gets squeezed…having neither the money or the opportunity to meet the high valuation centered money realities.

couple this with joe malarkey caused inflation….double whammy.

I am in florida right now…helping my brother do some renovation to his house…bought it 4 years ago…beach property…not some castle…a modest beach home. 3 b/r, 2 bath, single with a pool…garage…selling it for twice what he paid.

cannot afford property tax…is downsizing to a different neighborhood that is unincorporated and not subject to high valuation and insurance and tax problems. he has that option…kids are all grown adults. but his case is not common I would expect.

eventually, people in florida are looking at the realities that hawaii local faced long ago: two, three jobs and EVERYONE is working…or move to the mainland somewhere affordable and realistic.

it’s a combination of gentrification at scale…and really bad economic policies set by the state…all about the tax revenue.

I hope folks in Florida are prepared what comes next…it isn’t pretty…this isn’t even the worst of the inflation and joblessness that is going to happen. and with war looming…God help us all.

God Bless America

Terrific post!

Hawaii is a perfect example..a working class and successful sixty year old couple from here in Greater Vancouver B.C. a couple we know well.

“ rolled the dice” six years ago and bought a detached, termite invested, damaged dump for $320,000 ( U.S.) or so, on a “lesser island “and then tore it apart, added a basement suite and rented rooms seasonally.

A local working couple rent the tiny ( 500 sqft) or so suite for $1600.00 and the rooms on on Air BnB for “ decent coin”

My guess is the place is worth in the mid sixes or so.

It seems unreal to me..here on Vancouver Island B.C.folks are paying $400.00 plus a night to live in an ancient but clean room with a bathroom on or with the ocean nearby.

Cheers!

Don’t agree with your gentrification analysis concerning Hawaii. Hawaii had an economy largely based on sugar and pines agriculture. The plantation system provided a level of economic security, though not by typical definition “middle class”. WWII brought defense dollars which enhanced the business sector though not so much the plantations. Post-WWII saw the returning AJA vets demanding a bigger piece of the pie. With the business sector largely closed to them, they turned to government resulting in a massive increase in gov’t employment, especially with statehood. The jet age brought mass tourism as an economic alternative that would eventually replace agriculture as rising costs made Hawaii sugar and pines uncompetitive. Plantation labor largely migrated into low-level service jobs.

Land use planning decisions coupled with inefficient gov’t zoning and permitting processes result in new development trending towards the high-end. Meanwhile existing housing stock is hard to maintain resulting in upward price pressure. Air BnB and military housing allowances get blamed, but even absent those I think liberal gov’t policy decisions are the main reason SF houses now are median of about $1 mil. Sure, you got your billionaires on neighbor islands (and Oprah’s got some nice digs on Maui), but that doesn’t drive home prices in Waipahu or Kaimuki let alone Kaunakakai or Lāna‘i City.

have you seen how many NEW PEOPLE WITH BOAT LOADS OF MONEY have made hawaii their new homes in the last 20 years…it was nothing short of an invasion…in that time, there have been new terms: monster homes.

gentrification is the number one reasons for high home prices and inflated taxes in hawaii…all islands.

of course there are other historical factors…and of course there is a noted very corrupt government in hawaii….those contribute…but it has been the INVASION of vast numbers of very wealthy people moving to hawaii over the last 20 years…and with a limited supply…and very restrictive laws against overbuilding to protect the “aina”, prices soared….leaving everyone in the middle class up to their eyballs in higher property tax…more renovation and building restrictions…coupled with the joe malarkey “bineomics” that has left no state untouched…and for the worse.

it’s wealthy people snapping up properties that has driven home prices soaring….no other single factor has had more impact on the cost of homes in hawaii.

( I remember a time in the late 80’s when the first big invasion happened…it was very wealthy japanese who flew in, and literally drove around with literally suitcases of cash….knocking on doors and offering big huge insane amounts of money for residential and business building and property…it was a thing…overnight the market soared….mostly it was exclusive beach property and waikiki hotels…but it was other islands too and extensive sales on unimproved properties.. There were people who had inherited a small wood “rambler” constructed during ww2 selling homes for hundreds of thousands of dollars..the year before, the same home would have been valued at less than 80K….but that weird japanese bubble that happened was miniscule in its effects compared to what has happened in the last 20 years. It’s staggering how much homes prices and the taxes applies to all of them have soared.

All planned. And yet, you have folks who refuse to see what’s right in front of their face. Some go as a far as praising the policies that harm them. The idiocy is beyond reproach.

Very unlikely any of these issues started with DeSantis. Most, if not all, have roots going way back and are impacted by bad state-level GOP policy and corruption (not to mention county and local level issues).

Problem is, DeSantis lied to his voters about being their governor and he’s clearly not interested in getting his hands dirty dealing with difficult FL issues. He’ll do stuff that gets him clickbait headlines on PJ and RedState and nothing more. He knows 2024 will be a big family payday and he knows his political career is over.

The people of FL get poked and his family gets mega-rich (to lose).

The big risk in Calif. where I live is knowing at any moment, we could have a devastating earthquake.

I have a separate policy with CEA ( Calif. Earthquake Authority). The cost is similar to my homeowner’s policy and has a 10% deductible with many exclusions and limitations. Since my home is my biggest asset and as long as I can afford the premiums….

I too live here and my State Rep gave a town hall on last week that touched on this. I had also seen an article somewhere that talked about a small group of lawyers causing something like 70% of insurance lawsuits in the ENTIRE COUNTRY, and they’re here in FL!!!! Thank the Lord that the State Rep reported that they passed Tort Reform in the FL legislature but when these lawyers got wind of that, they filed gobs more lawsuits which puts huge pressure on these insurance companies to stay in business!

Same issuea here in Louisiana. I went from 3100.00 to 6100.00 in the 18 months after Ida and I didnt have a claim.

We can afford it, but many can not.

Inflation drives replacement construction costs upward. Premiums must rise. Homeowners cannot afford premiums. Insurers cannot cover losses.

Perhaps we can discuss the insurance industry during Nixon and Carter when the country was in chaos and inflation was rampant. My recollection was, even as a young adult, auto and homeowners insurance wasn’t unduly burdensome, at all, even working for grunt wages while in college. BTW, I paid cash for college too. One more interesting discussion.

How many Treepers believe this is all fabricated with an agenda to destroy the Republic? Can I get a show of hands?

“A a foolish man [who] built his house on the sand: and the rain descended, the floods came, and the winds blew and beat on that house; and it fell.” Matthew 7:24-29. It’s unfair to expect insurers not raise rates astronomically or pack up and leave areas where hurricanes destroy massive swathes of property on a regular basis.

Hurricanes have never destroyed massive swathes of property in Florida. The vast majority of the damage is caused by flooding from storm surge just like Katrina (cat 1) in New Orleans. The homeowner must have flood insurance typically not carried by most home owners.

Floridians usually have a homeowner’s policy, a flood policy and a wind policy. Yes, homes do get destroyed by hurricanes (wind) but most of the property damage is from flooding. Either way, the damage has to be fixed and that costs lots of money.

I live in north central FL. I do not live where I can get flooded, have a storm surge, or an earthquake. Tornados are always a possibility but very unlikely. WildFire is not possible either, as I own a large acreage that is not wooded. My biggest risk would be wind, or electrical fire, or flooding via broken plumbing. In 46 years of home ownership, I have literally never put in a single claim.

Last year my insurer excluded 25% of any wind damage. And doubled the premium. I can’t wait to see what they do when/if my policy renews next month.

Yes I lived in that area for many years. Completely different from living on the coast yet we get the consequences.

Poor freaking farmers

The backbone of America

Govt

“Go ahead and starve rodents”

#ronflation

Over the past year, Florida has seen a 12% growth in number of SNAP participants…second in the country….12% is .no where near our population growth, which is what the RINOs will use to defend our new welfare state.

https://fns-prod.azureedge.us/sites/default/files/resource-files/30SNAPcurrHH-6.pdf

I used to be a rugged individualist. Once the government damaged me and my business during Covid under color of law, that’s out the window. Retired, SNAP, Medicaid, SS, more money for ammo for the coming war. Economic warfare. I had my fill of those scumbag humans and their greed, avarice and mendacity.

I heartily encourage patriots to use every tool in the toolbox to stick it to the Communist. Whatever it takes. Oh, yeah, no homeowner’s insurance for years now. Screw them and the corrupt legal system that enriches itself daily off this. Get angry. We don’t have to take this anymore. Howard Beale told me that in a dream 🙂

Guardian is pulling out of SC. I have to find a new carrier.

Floridian here – we got caught last year, when 1) our insurer, Southern Fidelity, raised our rate to $6K….then, 2) right after we paid it, they declared insolvency. Thankfully the State took control of their assets and we got our money back. Now, on Citizens, the insurer of last resort – with a rate of a little over $2K per year. Of course, they also let you kow that is a major storm occurs and their assets are used up, they can assess a 45% adjustment to that (it is only 2% for private insurers). Still, that all beats the 6K.

Problem in Florida is that people want to live on the coast – and in some areas, like those hit by Ian, manufactured housing within miles of the coast is decimated.

I feel ya! I’m in Florida as well. Last year, our car insurance more than doubled. We had been with GEICO for over twenty years without an accident. They asked why we were leaving after so long. Seriously?! They responded that they were trying to get the rates down. Sigh.

This year, our homeowner’s insurance (mobile) also doubled. It went from $900 to $2700 in two years time. It was told to us that because lumber had gone up around 25%, the state of Florida had lifted some restrictions. We shopped around regarding insurance decisions and left companies that we had been with for years. I’ve lived in Florida for over 50 years and this is just killing our hope of retiring any time soon.

We are in coastal south GA. I am hearing from neighbors that their insurance is being cancelled, Lloyd’s of London in this case. We called our insurance agent. They are bewildered as to why insurance rates are skyrocketing here, but being lowered for South Carolina, which is just across the Savannah River. BTW, we are bracing for a huge increase in our insurance in October that will match the tax bill I just received. Wowzer!

Sorry, So. Carolinian here…my insurance did NOT go down…it went up. So did my car insurance.

And I CAN’T afford it.

There’s a house insurance crisis for everyone. Same thing is occurring in AZ. 40-50%+ increases! It’s root cause is basically a result of Biden’s energy policy. The fuel costs are driving up the cost of raw materials, finished goods and likewise the insured replacement cost of a house. It’s the same cause and effect that’s resulted in the rising cost of food and, in fact, inflation in general. Now, when you compound this with Democrat spending habits that necessitates the availability of more taxpayer money to spend with the likelihood of increased taxes then we have a genuine compounded crisis. Sooner, rather than later under the uni-party we’re all going to face the financial triangle of income vs necessities vs bills.

My insurance, when I could get it, was close to $2000/yr for a 800 sq ft simple home in rural Commiefornia in 2015. After 55 years we left to Arizona. We now pay a little over $500/yr for a 2000 sq ft custom home. Auto registion and insurance is a fraction of what we paid in Commifornia. Utopia is very expensive. (Snark)

Insurance companies see the losses coming and are getting out before this hurricane season cranks up. This will lead to

government takeover of insurance market. They created the crisis and they will “solve” it.

Our “insured” materials subject to inspection and approval stamp by our federal government. Does your home meet current federal guidelines for CO2 emissions? No, here’s a fine. If you can’t pay it, confiscation. Is your vehicle “Clean & Green”? No, subject to fine and confiscation. Are the food materials in your house from approved “ESG” companies? No, here is your fine.

Don’t think this isn’t on purpose. It’s the long game we have to prepare for, not the knee jerk-reactions of most people.

The government already runs the insurance market- they create the regulatory framework and laws that insurers must follow and some are to the detriment of the insured, not the insurer.

Bottom line- government already runs it.

It’s why UWs and actuaries are required to be licensed.

unlicensed motorists not mentioned regarding auto insurance. I wonder what the connection to illegal immigration might be.

I would expect the ranks of unlicensed and uninsured to ratchet up as hostilities grow and citizens increasingly have less and less to lose. That is exclusive of the imported government mercenaries who run their ops on citizens. They don’t need such pesky things; they’re backstopped or expendable.

Shame meatball is in South Hampton NY, or maybe he could offer those citizens some insight on how to cope with the bad news.

The Absentee Governor

Lived in Coconut Creek FL for 10 years lived thru two bad hurricanes damaging home. Home repair and insurance got ridiculous. So moved back to rural New England, my home and auto bills now reasonable and as example my 4 cars cost under 1.5k total, Paid that for one car in FL.

I am in the mobile home insurance business and I am down to a handful of companies. We cannot forget all “free” roofs and resulting lawsuits when it was found that the claimed “damage” was done multiple years earlier and constituted a fraction of the actual damage had the claim been initiated when the damage “occurred.” And who makes money from this debacle? The lawyers. Add in the companies huge reinsurance money increases (charged by the companies insurance companies and “someone” needs to pay those bills. One elderly client made claim for a roof three years after the storm. Her actual damage was one tiny section of her roof under $1,000 (under her deductible) and the roofer claimed $45,000. The client wound up paying $10,000 for her new roof to the roofer.

I have clients in New Port and south who are still waiting for roofs and need to make a complete accounting of how they spent their claims checks.

My non-renewals are very large in number and I receive 30-40 calls a day from potential clients with a very limited number of companies to place their properties. Thus happened three times in the last 20 years but nowhere as severe.

Write letters and make phone calls to your Tallahassee representatives! It has been working in Washington to a small degree-it just could possibly work in “free” FL, too.

I am a flooring sub contractor who lived in Florida from 1977 to 1990. Insurance fraud is rampant in Florida. People have this entitlement idea that because they paid for homeowner insurance it is OK to have the insurance company buy them new flooring every decade. I have even had a brazen few people tell me directly what they have done. I showed up to give an estimate on a whole house of damaged carpet but the brother who was supposed to flood the house hadn’t done his part yet!

It must be a piece of cake to go through a hurricane without suffering any damage and than “arrange” damage to get yourself a new car, kitchen cabinets or flooring. Also, with previously honest insurance customers being gouged because of fraud, how long till some of them decide to moralize insurance fraud because … Everyone is doing it and I’m paying for it!”

I have never sued anyone or collected on any homeowner or automobile policy. I would never help anyone defraud an insurance company and I would report anyone that I knew who did.

My post above I wrote with indented paragraphs and as soon as I posted it, all the indentations disappeared? I edited it again, posted it and the same result?

Put two lines between paragraphs (press enter twice not just once).

What you outline is known as insurance fraud.

“We cannot forget all “free” roofs and resulting lawsuits when it was found that the claimed “damage” was done multiple years earlier and constituted a fraction of the actual damage had the claim been initiated when the damage “occurred.””

^^^^This is fraud. Which is why I believe you have certain words in quotes.

“The elderly client made claim for a roof three years after the storm. Her actual damage was one tiny section of her roof under $1,000 (under her deductible) and the roofer claimed $45,000. The client wound up paying $10,000 for her new roof to the roofer.”

This too is fraud. Whether initiated by the elderly lady or the contractor. It’s fraud.

And regardless of one’s feelings about insurance- those conducing fraud need to go to jail. They impact everyone else.

Those waiting for new roofs and already received claim checks…well, why are they still waiting on a new roof: is it scheduled and not done yet? Or did they spend the money on something else? Again if the latter- not fraud if roof was actually damaged (if not, fraud) but they don’t get to file a second claim for the same thing and cry foul. They should, if they recieved money for fixing their roof but still need new roofs and want the insurance company to front more money, should have to provide an accounting. If it’s legit that they need more cash, a good company will step up.

What you’re saying is that the insurance adjusters are committing fraud or helping the homeowner/roofer commit fraud.

My uncle was a GC. Not an insurance adjuster but he could tell you without question whether the damage was recent or in the more distant past. Why can’t the adjuster?

Florida will end it’s personal income tax satutus and take over the home ownership insurance bizzz to help pay for it…in my opinion

Isn’t this the state where the Big Shot, absentee governor is running for higher office, while still taking a paycheck for a job he isn’t doing?

Here is what Jimmy Patronis, Florida CFO, said when a reporter asked what’s a person to do if they receive a Notice of Non Renewal…

“I say to those policyholders pick up the phone and call another carrier,” Patronis said.

Thanks, that’s a lot of help. What a pathetic answer.

IL landlords forced to rent illegal immigrants or face criminal charges. With the risk pool deepening – all renters will pay jacked premiums. Just like Obamacare.

Remaining FL insurers will absorb the uninsured at $$$. Government will slither their way in as the savior versus the boogeyman insurance companies. Just like Obamacare.

The Government Reprising it’s Role as Fireman Arsonist or is it Arsonist Firemen? Brought to you By Cloward, Piven, Powell, Yellen & Soetoro.

With that fat slob Illinois governor making it illegal to not sell or rent to illegal invaders,I hope it is taken to the Supreme Court. I will say several, 6-3, will think that’s perfectly fine. If I owned rental property in Illinois, it would burn.

Property insurance is unaffordable as is most of the goods and services we are buying. We cannot export jobs to foreign manufacturers and then imports their products and come out on top. Neither can we import nearly unlimited labor and think that as the working class we will have any pricing power in wage growth. We are operating this country as an oligarchy with the few dictating the rules of the road. Trump had it right and that is why they go into a panic when he shows emergence as the leading candidate. We need tariffs to weed out the unfair and subsidized goods and to rebuild our manufacturing base. And we need an end to illegal immigration and the subsidization of the illegals.

China grows because they protect their workers jobs and they do not import labor.

Getting President Trump elected needs to be our focus right now.

The vast majority of storm damage in Florida has always been flooding from storm surge not wind damage from hurricanes. Typical home owners insurance covers wind damage but not flooding. This was the case for Katrina(cat 1 with very little wind damage in New Orleans) and the big storm in Houston and until the last storm in Ft. Myers, FL which did have a lot of wind damage but also way more storm surge damage (i.e. flooding).

Incredibly in state of Md car insurance rates have just increased 30%! We are in a Recession soon possibly to be Depression. We have GOT TO GRT JB OUT !! He’s destroying our great nation but by WEF BIT

It’s all planned to gut America…NWO is the new agenda.

The “risk exposure” Farmers’ is talking about is the absurd litigation risk posed by Florida’s Tort lawyers, the richest in the country. It’s not hurricanes. Tort lawyers make up around half of the tv advertising in Florida and I’m sure, have millions of dollars to buy influence in Tallahassee. The recent “tort reform” legislation was smoke and mirrors. Insurance companies aren’t charities. Instead of robbing citizens, modern bandits rob insurance companies. I’ve been in the insurance industry for over forty years and it’s obvious why companies make the very sensible decision to leave the “Sunshine Sinkhole.”

In addition to high living expenses, Florida has flooding, hurricanes, evacuations, power outages for two weeks, alligators, large flying insects, high temps and humidity for 6 months. But, alas, no State personal income tax. Sounds like Valhalla for retirees.

Insurers have the inside track, and have been withdrawing coverage because they know that geo0-engineered weather will be coming more and more frequently, targeting states and areas of states. Viudeo evidence of Ian being strengthened and steered was on the net before the storm had finishing traversing the state.