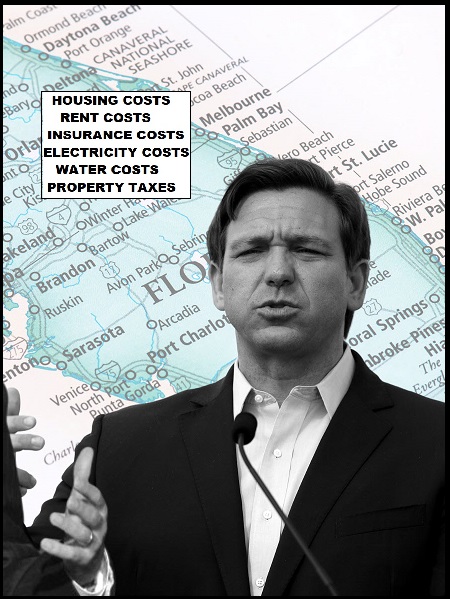

The insurance crisis in Florida is hitting the middle-class family, working community and retirees on a fixed income directly. Hundreds of thosands of residents have lost insurance coverage, and even more have seen policy premiums double. It is not uncommon to find homeowners who are paying more for insurance than their actual mortgage payment. Unfortunately, the situation is getting worse.

Farmers Insurance has notified the state they are pulling out of Florida, will not be writing any additional policies in the Sunshine state and when existing policies expire, they will not be renewed. Home and auto policy rates have already doubled in many areas for many people.

Farmers Insurance has notified the state they are pulling out of Florida, will not be writing any additional policies in the Sunshine state and when existing policies expire, they will not be renewed. Home and auto policy rates have already doubled in many areas for many people.

The insurance situation is becoming more unstable by the day, and the future outlook seems even worse amid reports that even more companies are planning to exit.

FLORIDA – Another property insurer is dropping coverage in Florida.

Farmers Insurance will stop writing new business and not renew its existing “Farmers-branded” automobile, home and umbrella policies in the Sunshine State, the company said Tuesday.

Last month, Farmers said it was only pausing new business in Florida. The company is also limiting new home policies in California, where it is based, according to news reports.

“This business decision was necessary to effectively manage risk exposure,” the company said in a statement.

The move will impact 30% of the company’s business in Florida, or roughly 100,000 policies. Policyholders affected by the decision are required to be given 120 days’ notice that their coverage will not be renewed.

Farmers on Monday sent notice of its plans to the Florida Office of Insurance Regulation, which is reviewing it. Insurers must give the office 90 days’ notice if they want to discontinue writing business in Florida. (read more)

The insurance company withdrawals works in concert with investment groups who prey on the outcome. Single family homes and even large condo developments are squeezed into a situation where housing is no longer affordable. The investment vultures then swoop in and end up controlling the properties.

Florida’s working and middle-class is being destroyed and a divide between the haves and have-nots is being created. The wealth gap is expanding as families are forced to leave the state and a larger percentage of self-insured rich people move in.

Long before Ron DeSantis became a potential presidential candidate, and long before Hurricane Ian devastated southwest Florida in 2022, I was highly critical of state policies that were not constructed around the backbone of the economy, the working class. Temporary H1B Visa workers replacing permanent residents as a workforce to fill the gap is not a long-term solution.

When you stop paying attention to the economic systems that support a sustainable service and production workforce in Florida, this snowballing outcome is predictable. None of it is good. Unfortunately, as I forewarned prior to the COVID era, Governor Ron DeSantis is creating a class-war tinderbox. The sentiment on the ground is increasingly growing angry. His absence is only making it worse.

“My Tribe“

My tribe too!

Yup my policy was dropped last year despite never having a claim in almost 20 years. To get a new policy I had to get a new roof and replace my driveway.. 25k later I was able to get a new policy at twice the price of the old one.

Mine has quadrupled. I did stick em for a roof though.

And that is hurting all of us.

Yeah, and we all have to replace our roofs every 15 years now. Thanks to lying, self-centered idiots and roofing companies that conspired and made claims after Irma. Your roof may be warranted for 25 years but the insurance companies won’t cover them after 15. Glad you got to stick it to them though.

If Farmers could make money selling insurance in Florida, they would stay there. But, because more and more houses are built in storm and flood zones their risk is up. And, with home prices doubling in the last 7 years, Insurance rates need to double to continue doing business. If the State Insurance Commission won’t let insurance rates rise, companies are forced to leave or hemorrhage money.

BINGOI!

My policy in FL went from $1200 to over $4000 … we are currently self insured. Damage from IAN left me out over $6,000 on what was not covered and paid me <$300 for what was covered. Not to mention that electricity has trippled over the past 5 years. I find myself retired and a have not in the free state of FL. Too old to move and too poor to live … and they call it paradise. SMH

No you’re not. Sell all you have. Get a cheap tag along and live at an Rv park in the Carolina’s or Arkansas. You’ll be fine. And pray. Thank God for all he gives and takes away.

Believe me, I thank God every day … and I am truly blessed!

That’s good!!!

stay out of North Carolina, dont care who you are. until we can get a moratorium on letting you migrants vote.

Policies in Alabama have been that high rate for quite some time. Even at the high rate the deductible is such that you are basically self insuring unless a tornado hits your house. Fire and theft only ….runs over $1200.

A lot of folks here are finding Farmers difficult to renew. They took my policy over three years ago and now I’ve left them due to restricted coverage, terms of renewal and high fees. Everytime I see that Farm’s ad (We are Farmers…duh duh duh de duhduhduh) I think how many will loose with these bums. Screw ’em.

Farmers and all of them go up and up every dang year without fail….and then as if….they need a big rate increase approved by the state ….well they get one. I remember years ago ….well over a decade….the state approved a big increase because the companies lost so much in the stock market believe it or not. I don’t recall us getting a break when they were making money hand over fist in the stock market. This countries policies and politicians are truly ruled over by big corporate US. Although at one time we did have the power of the vote they still controlled who we voted for. Now we no longer have either.

Our Louisiana criminal, masquerading as Insurance Commissioner, Donelon – is responsible for the “named storm” deductible theft program … my less than polite letter to him – using 2 of Insurance Companies favorite words – arbitrary and capricious (denied is #1) … applied … the hurricane storm that caused hundreds of millions of dollars in damage – all the way to the Canadian line – was ONLY imposed on South Louisiana homeowners … zero reply … except – now EVERYTHING is “a named storm” throughout the entire Country … so insurance companies can gouge their Insureds with HUUUUGE deductibles on property damage !!!

I’m sure his kickbacks from grateful insurance companies have been Joe-MASSIVE !!!

we know a thing or two because we’ve seen a thing or two – and we’re outta here Florida, see ya, wouldn’t want to be ya

I switched from American Family to Farmers for one year. Premium was considerably lower. Renewal premium with no claims, no changes, was much higher. Went back to AmFam. Not a fan of Farmers.

I’m still a little unclear on what’s happening and why.

Farmers insurance is not offering insurance policies in the State of Florida any longer because they aren’t profitable and / or they’re losing money on the insured.

Reverse supply and demand.

Causes stress ( financial and market ) on policyholders and other insurance companies.

The underlying cause is insurance profits and the fact that insurance companies are big donors to DeSantis.

Nothing new, right? There’s always been weather, disasters, civil unrest, crime, you name it. Think back to the last high inflation/social unrest/crime ridden era, the 60’s and 70’s.

Any complaints about insurance back then? My memory was, like college, it was affordable. What’s changed since that clusterfck period that didn’t appear to affect insurance?

How long have humans survived without insurance? How many centuries?

IMO it’s another tool of the Communist to divide and conquer the population, most specifically the vast middle that has something to protect. That’s the target. Corporate and government fascism running unfettered.

We have choices. I’ve made mine. Economic warfare. Don’t play the Communist’s game and take direct kinetic action if threatened. One person’s life means little. A million or two taking action, then things will get clarified. Look what the change in beer drinking from Bud Light did. What did the Canadian bank run do? Small examples. Think large. How can we destroy the insurance industry and the Communist cock sucking humans in it? They make their choices to support the Communist. That has a price.

Life is war, then you die. Choose. Or, complain. I’m not complaining. I chose.

Dunes….what has happened since the 60’s and 70’s is that mansions have replaced beach cottages. It is the build up of business and expensive homes. Back in the 50’s and 60’s here in AL. they didn’t even build directly on the beach but across from it. Back then you also had the money to pay cash for it there were no mortgages on beach cottages. Insurance and mortgages have allowed for the buildup of hurricane prone areas. There is also the stock market that has come into play. Insurance use to be where we all with our premiums helped insure each other now it all involves the stock market and the upside never rewards the insured but the investors.

This. The beach house we owned when I was a child was about 1/5th the size of the house that occupies that lot today. On the beach. Whomever insures these things is just asking for a claim.

Secondly, in days long gone by, if your house sustained some damage, the neighborhood dads came over with their hammers and helped you fix it. Today, that’s illegal because you aren’t a licensed contractor and insurance won’t cover such illegal repairs. 🙄

It’s the financialization of everyday life that’s also driving these costs.

I wonder if, just like TPTB only want 3-4 too-big-to-fail banks for better control, they want only 3-4 insurance companies insuring commercial and residential properties.

How quickly “own nothing and be happy” could befall millions of homeowners if TPTB lean on just one insurance company to pull or restrict policies.

Just a thought…..

Agreed except where you use the word communist I would say globalist. Maybe we mean the same thing?

They do want to destroy the middle class and their plan for coastal areas is to have them be for the elites. They have been working on this for awhile, but now their strategies are more in the open.

Are any insurance co-ops.forming. pooled risk might be 5he way to go.

My take: FL has an elected insurance commissioner. Politicians have wealthy friends who donate to their campaigns. Wealthy people live on or near the beach, and they don’t like to pay big insurance premiums for their homes. Nobody does. Political pressure on the elected commissioner means rates do not reflect the cost reality (which is driven by many things, not simply hurricanes — try litigation, e.g.). If insurers cannot cover their costs, and note they need approval from the commissioner’s office to charge those rates, then they go out of business or they stop engaging in writing insurance where it is unprofitable from the start.

There are solutions but they are difficult, politically speaking. The trial lawyers, big donors, the construction lobby, etc. all have a lot of sway in the legislature. Whose ox gets gored first?

Oh my gosh! We are truly the serfs of America.

If this is what they mean by retooling, it will also be a failed effort. Both are hoping for an arrest of a lawfully elected President.

The DeSantis vs. Newsom Duel

By Christian Milord

11 Jul 2023

https://www.theepochtimes.com/the-desantis-vs-newsom-duel_5386130.html

Sadly ET is slanted toward DeceptiCON RON! I have been watching it for awhile. I set them straight.

On ET: Anklebiter Fickle Elder is one of their own. He couldn’t make it against Gruesome Newsom, didn’t even try, and yet he also thinks he can be President.

Then there’s this at ET, made to make President Trump look bad:

Trump Set to Miss Iowa Presidential Forum Hosted by Tucker Carlson

By Ryan Morgan

11 Jul 2023

https://www.theepochtimes.com/trump-set-to-miss-iowa-presidential-forum-hosted-by-tucker-carlson_5390456.html

If I were President Trump I might sign their loyalty pledges and then tear them up Nan-Xi Pelosi style at the end of the event, during the ending credits, without saying a single word.

President Trump had already committed to Charlie Kirk’s outfit to speak. Resist the Mainstream also has a hit piece on President Trump on this “Iowa Presidential Forum.”

The Traitors in our midst,

Are real good with timing.

I wake up every morning, just thinking about who I’m trying to screw over today, and what time?

What a waste of human life.

I would hope that even if he didn’t have other commitments that President Trump would have turned down the Tucker “town hall.”

I wonder why Tucker feels the need to help these people campaign. It is clear people want President Trump and I would have thought Tucker would support President Trump’s policies.

You might say Tucker wants people to be informed, but I think things are pretty clear and these five don’t need help.

I also wonder why Tucker scheduled his event the same time as the Turning Point event.

I don’t plan to give the Tucker thing energy by watching it and I’m so happy President Trump isn’t giving it energy. I hope he sticks to ” no debates.”

A year or so ago, I read the head honcho of Epoch Times passed away (unexpectedly) and I wondered if they would continue to provide good reporting

I tried to find info on internet all that I could find was info pre-2022 talking about it being an evil source of pro-Trump misinformation.

Here is a review BEFORE he passed:

https://www.coloradoindependent.com/2019/11/15/colorado-local-news-media-robots-epoch-times/

Our insurance costs approximately $ 5000 pesos. Yearly. What a difference in Mexico!! Viva Mexico.

Have fun when you eventually get jack potted in a .50 cal, 7.62×39, or round=X crossfire… or get your head severed with a chain saw by some dope cartel mutants. This is MY country and me and mine will stay here and fight. FXXX mexico and those filthy pigs who’ve enslaved their people along with the Catholic church for centuries. You have 2 “buyers” so far who can maybe join you.

Wow! You are very uninformed. Dude. Abd I’m very glad. We do need your ilk in family God Loving paradise. I will pray for you.

The California exodus to Florida is having secondary effects. So sorry for those of you who have lived there peacefully for decades.

Cali also destroyed colo. Cali is now destroying idaho. How about all you cali’s STAY in your bankrupted state of gavins garbage. We don’t want you!!

It seems when ppl leave California they bring their progressive, I hate how they co-opted that word, ideas with them. It is tantamount to cancer when it metastasizes into healthy tissue.

You know, I really resent comments like this. Many who moved out of California did so specifically to move to more “red” conservative areas. I’m speaking for myself when I say I DID NOT bring any “progressive” ideals with me and hope that my self sufficiency and tax revenue that I generate are a bonus for the community where I moved to, not a drain or a burden. I pay my taxes and vote conservative.

Honestly, you have to understand that there are a LOT of conservatives like me in these blue states that are either stuck financially and can’t afford to move or have family ties that make it impossible.

Please don’t disparage all red blooded Americans who have moved from horrible progressive states like California.

And Oh By The Way……………some of these states like Colorado, Idaho, and Florida had plenty of their own home-grown idiot progressives. Don’t think you are insulated from nit-wit ideas.

Got a letter from a dear friend yesterday.

She and her family of four moved from California to Idaho over a year ago and have been treated very poorly since getting there.

They are very strong Christian conservatives — who, they thought, would fit in perfectly with the people of Idaho.

They left Californication with a sense of joy knowing they were shaking the dust of evil off their feet on the way out, but no one in Idaho wants them.

They were lied to about earnest money that would be refunded once they moved into their new home, and after losing a LOT due to the major life change, she decided to go back into the work world.

She is not even being called to fill basic jobs; jobs where a lot of employees are needed, and believes it is due to many factors, the largest being she had been a Californian.

She and her husband own their own business, which also suffered, but that was a chance they were willing to take to get out of hell while they could.

Now she is washing her families clothes by hand and they’ve been eating their stores of food, the food meant for when the world crashes down around them.

The world has fallen down around them, because the people of Idaho refuse to believe a conservative can come out of California.

As a Christian the best part is to read their take on what is going on with them through this dark valley. When she wrote that they were eating their food stores she included that it’s a good thing they did that now, since they are finding out some of the food they were told is “delicious” is so bad they wouldn’t even give it to an animal — and doubt any animal would eat it. Finding joy in hard times. Those are the people we all need around us every day.

That’s just tragic. I too have felt discrimination when I say that I moved from California.

Bottom line – you can’t paint people with a broad brush before you’ve even given them a chance.

I pray for your friend…….

Thank you and well said.

I, too, resent all Californians being painted with the broad brush of being a liberal idiot. I echo your point that there are many in the state who are conservative – and this should be known! Some of us are fighting to save this state, rather than flee. Our captured voting system doesn’t allow the number of conservatives in this state to be heard. Many don’t vote for this liberal stuff, yet we get blamed. Other states are beginning to know what this feels like. Some of you already know exactly what I mean as you see your election results look completely impossible.

When I started seeing judges striking down things that the people in the state voted for overwhelmingly, then I saw the writing on the wall. The will of the people was toast.

I neglected to mention good folks like you who are willing to stay and fight. I just didn’t have it in me anymore especially with what was happening to young families with school age children. You only have so much time with kids to get it right………….

Please don’t overgeneralize people from California. I lived in California my entire life until two years ago, when I moved to Texas at age 70 to ESCAPE the crazy liberal Democrats. It’s definitely better here in Texas, BUT most of the Republicans in office are RINOs, who recently impeached our great Patriot AG Ken Paxton.

Correct … like anything else – those who move to escape RAT insanity are assets to their new cities and States … the damage comes from the millennial morons … a Soros Agenda tactic … he leaves the wealthy & poor in blue cities & states and moves the young millennials to RED cities and states – into huge apartments, condos & “gayborhoods” w/good jobs … turning everything blue, RINO & crime infested – Austin, Houston, Dallas, San Antonio etc.

The blame is really on the progressive socialist school systems that have indoctrinated three generations of democratic socialists who have overwhelmed the state legislatures.

I blame the parents who leave their kids in these schools.

Progressives tend to stay in CA. The middle class in CA is being wiped out, so if they leave it’s certainly because they’re conservative and despise what liberalism has done to this state.

Colorado was destroyed politically by California.

You can add Nevada, Arizona, New Mexico, ……………

Nevada and Arizona had questionable elections.

Research the history of voting machines and problems with elections nationwide. I don’t think voters are really voting for this awful policy. CA was a middle class red state in the days of Reagan. Now it’s horribly corrupt

Those elections were not questionable. They were rigged.

True – worse than rigged. Went to a city council meeting to demand the Dominion contract not be renewed. (Failed) The argument that we just can’t count paper ballots is stupid. They were counting Nov ballots into Feb here until the Democrat “won”. So efficient haha

You should see what they have done to Calispell MT

That’s fine but I would argue it’s not California people fleeing Commiefornia that are the problem. Our elections have been hijacked just like the rest of the country. You’re telling me Newsom “won” by 61.9% of the vote and also “defeated” the recall (Citizen anger during Covid was HIGH) by the same 61.9%? Come on!

Also, I went to Arizona August 2020 looking for sanity and the masks and oppression were just as bad there. All politicians in CO (except maybe Boebert) are progressives. I see this as just another divide and conquer tactic. Make citizens hate each other.

Precisely. Sometime, I see comments here like “Leveraction” and “NTB” and I wonder if they are trolls out to divide people…….or if they’re just plain ignorant.

Don’t rule out massive insurance fraud when builders built and rebuilt houses without code enforcement or government looking the other way. Also building homes and businesses out to the waters edge, guaranteed to be destroyed when a hurricane hits that shore. The majority of people who own houses inland where the hurricanes will do less damage are paying for this.

Exactly!

See my previous post.

The idiots keep rebuilding in known hurricane zones. As their losses mount up year after year, the risk is spread to the rest of us.

How about the idiots in the tornado “zones”, the flood zones, the drought zones, the anything zones. Seems like we all live in some kinda zone. Here in Alabama we have a very small coastline and when a hurricane hits it is the northern counties that are under threat of tornado. What would you suggest, vacate half the state?

Tornados are 1% the size of hurricanes and occur randomly over 60% of the United States.

Hurricanes occur in well-known stretches of the Atlantic and Carribean coasts in Florida, North Carolina, Louisiana, Texas, and Mississipi, and pretty much limited to the coasts (see Hugo for exception to rule). When they occur, they destroy hundreds of thousands of properties (maybe damage millions). Tornados destroy hundreds of homes, if that, typically.

There is no comparison in terms of risk to insurance companies.

Hurricane Agnes destroyed a lot of homes and businesses in the eastern part of PA. Hurricane Sandy did a number on northern NJ and NYC.

Gulfaddict…the answer is to be a good Boy Scout.

“Be Prepared”.

Seems like a reasonable concept.

Or 2/3 of the country? I doubt there are many states that do not have tornados, flooding, ice storms, or some other devastating event that is destructive.

Maybe it’s the old game of “bait and switch”

https://www.policygenius.com/homeowners-insurance/news/coastal-insurance-collapse/

It all ends up with Citizen’s Insurance – the Citizens of Florida –

https://www.policygenius.com/homeowners-insurance/reviews/citizens-property-insurance/

This is nothing new. Property insurers cut back or ended the writing of new coverage en masse shortly after Huricane Andrew. The new residential constructionn codes (primarily those that deal with windspeed ratings for roof truss tiedowns – aka Simpson StrongTies) helped mitigate this, but not entirely.

If you want to affix blame on someone for this problem, I suggest you start with the county and town property tax collectors. If they would cease issuing permits for construction in the most weather- and sea-exposed areas, there’d be fewer claims filed after each major storm.

You are correct! I lived in Hillsborough County when Allstate cancelled at least 25% of their Florida policies after Andrew. Mine was one. Cost me double to get a replacement policy with less coverage.

State Farm and Allstate have both left California. The decision was based on the Reinsurence market and costs, the skyrocketing cost to re-build in the state and the policies of the legislature to keep premiums low which insurance companies saw as a risk in a catastrophic event.

FEMA is partly to blame. They insure in areas that are not suitable to build. Think tornado alley, Galveston, Texas, back hillls of California. If people want to live in risky areas, they should self insure, but the government should not pay to rebuild in these areas.

We went through Thomas Fire and then a landslide in California that killed 23 people. Several insurance companies cancelled policies around us after the event. We sold and moved to a safer location.

Every citizen is also subsidizing flood insurance and water front property insurance. They are offered by big gov, subsidized by you and I. In Florida people want to own water front property even in flood prone areas. The counties give permits to building in those areas, people buy thinking things are great, then when a storm comes and floods the area the residents want you and I to bail them out for their ignorance, instead of asking why was building allowed in the area in the first place. This is prevalent in Florida, population growth encroaching on swamps and builders get permits to build there.

With an RV you can at least live in a Wal-mart parking lot, or so I heard, in whatever town you choose, whenever you choose, with no property taxes.

We the taxpayers have been funding them (Wal-mart) for years, so they owe us. They have been stealing our Main Streets and our towns for decades, putting us out of business.

Walmarts in some locations (not all) allow overnight RV stops, but I doubt if they would permit multiple nights/days. There are federal lands where free boondocking is permitted (no services or hookups), but they often have time limits as well. Many private RV parks have long-term (‘seasonal’) residents, but of course you pay for those.

It all depends on the state you “reside” in. You forget residents/homeowners/bz and business property owners under the new rules of egagement have no rights in many states. The homeless and drug addicts and mentally unstable have taken over their lawns, sidewalks, parks and crawl spaces, many even their entire homes.

If you can’t kick them off the sidewalk in front of your home or bz how are you gonna’ get them out of the Wal-mart parking lot?

Many places require that you only stay 6 nights in a row. This is to prevent rust buckets that never move and develop entire ecosystems underneath. As opposed to permanent ‘manufactured community’ homes. A lot of people stay in one place where they are comfortable, get to know their way around, know the neighbors etc. and then spend one night a week at a rest stop. That is manageable.

WalMarts in Las Vegas do not allow overnight parking nor do most shopping centers here in town.

None of the Wal Marts in Tucker or Decatur do, either. City of Tucker won’t allow it.

Don’t get me started on how codes enforcement operates in this town. Selectively and vindictively.

Cracker Barrels are the place to park now. They’re awesome ! A lot of Walmarts are clamping down on RV’s in their lots now.

State Fram HQ located in Ill.

Would be interesting to review where State Farm insurance policies/rates are headed in other states.

One thing can be asserted confidently: inflation data is highly suspect.

Was notified by SF a couple of months ago my insurance in AR was going up about 10%.

Property?

Asset bubbles have their own magic!

Brain *art…Farmers insurance.

Northern CA.

Farmers insurance for 32 years.

Was $4,000 last year.

$10,000 this year. No notice of increase. Happy not to be cancelled… at least not yet. The State’s insurance program is required if private insurance can’t be obtained ( and it can not in some areas).

One of the biggest problems is that Blackrock and the likes are allowed to buy large quantities of houses with cheap/cheaper or leveraged money (some of it, one way or the other, made possible by Yellen). By this glut they increase the residential real states prices and the insurance (for a more expensive real state) would be higher. The thing is that the job pay has not increased at the same speed. So the working class is losing. The legislature better pass laws preventing funds from buying residential real states. Only individuals, with their own private money at risk, should be allowed to compete in the residential housing market. Is that big money is also financing DeSantis?One wonders.

Yes, it is the same big money. And no, they will not pass laws to prevent the problem.

The reasons are what you are seeing is the globalist plans being carried out. This is being done on purpose.

I have always believed that the West Coast fires are to drive the middle and lower economic class people out, so the millionaire/billionaire classes can take over. A land steal of the worst kind, just like they did with farmers using the Death Taxes that President Trump finally got rid of.

They couldn’t care less about having you as a neighbor and can afford to buy large properties and turn California into the MECCA for the -illionaire classes.

In my Florida area there are several large-scale home developments underway. Amazing how many homes are being built. Most are what I would call “small” homes.

I have no idea where all these people are coming from, what work they do, or how they obtain homeowners insurance.

IMO residential real estate in many communities is viewed by many as an asset class first, and as a home second.

Immigrants to our city ( Greater Vancouver B.C.) get on the “ property ladder” as quickly as possible.

Several family members get “ on title” qualify for a mortgage or get it through their “ church “ and never stop acquiring “ dirt”

We have hundreds of homes in communities surrounding Vancouver that have homes larger than many modest motels, or hotels.

They are homes to several extended family members and their “ high end” vehicles.

Real Estate agents, Accountants, Banks, Real Estate lawyers, and governments via higher taxes, and here in British Columbia and sales tax on property purchases.

Add folks that Air BnB their places are all making huge money on this paper boondoggle.

When will it end..up here not anytime soon. We have 500,000 immigrants anticipated to be accepted next year, into a country of approximately 35 million.

We are doing okay and have participated in the “ property racket” but like many we know are “ sitting tight” as Insurance and Taxes are getting onerous.

Hold tight!

At closing Insurance sucks them in with one rate but after that big rate increases. Even on existing homes you can switch to a more affordable company then the next year they hit you…..It almost seems like a bait. ATT does this with phone plans and cable plans. Good rates for 6 months or a year then all the credits fall off.

Look at who builds them

All illegals in CO building Dr Horton crap homes at $600k

Are they putting ideas into the heads of the sleeper cells and saboteurs……..

They have had those ideas for a long time.

It works both ways. The big cities would make Dante’s Inferno look idyllic after a week of no power. No water. No food. No mechanical conveyance. Cannibalism in a week…….

Instant Hell on Earth.

While Michael Z Williamson says his book “Freehold” was not intended to be a “how to” manual to destroy civilization it pretty much is. I recommend it highly.

Farmers was crossed off my list of viable insurers when the company, as it is with the majority of others, enticed a low sign on annual premium at very good rate. Once a customer is secured the company substantially increases the rates each and every year.

People pay thousands of dollars/year for coverage only to discover when the time comes to make a claim these companies either significantly increase the rate or drop the customer. I would strongly suggest people lobby for state/federal government oversight on all insurance companies.

I would not count on “government oversight” of an industry that is already one of the biggest donors to politicians unless you are planning on the insurance industry charging you more money so that they can increase “donations” to politicians to get them to vote in favor of the industry.

Look at what has happened to the medical insurance industry and how heavily regulated it is.

State officials are in the pocket just like health BCBS.

This is on purpose. Throw Florida to dems in 2024. Won’t even have to cheat much if succss

Insurance is a scam to begin with.

The American people have been scammed out of trillions of dollars that would have otherwise covered many things for many differnt situations.

Interesting post!

I agree unless one is “ scamming it”

A friend of the family a retired Colonel in the American military mentioned that to me many decades ago.

He new his stuff, and was a man of high intellect.

Apparently he had become a dentist while in the military.

He stated Insurance companies controlled the U.S.A. and Canada where he finally settled it was the Banks.

Now that was back in the seventies, and he is long deceased, and maybe his views would be different today.

Cheers!

Thank you Sundance for educating me to reality.

As I began reading I instantly saw this was a way for Blackrock et al to turn Florida into a giant favela on the road to depopulation of Earth. Continued reading confirmed my thoughts

Holocaust in the making so the psychopaths can turn the world in to vast estates with enough serfs to provide cushy lives for our “betters”.

Exactly. What we are seeing is the globalist plan and the uniparty (the dems and repukes ) are carrying out the plan.

Electing President Trump is what to focus on now.

Things I advise young people to do:

Live in an rv or cheap mobile home for a few years and save every penny you can scrape up.

Buy a piece of property in an area that looks like it will gentrify soon and build your home yourself. Don’t know how? Go work for a home building company for a few years and learn every trade you can.

Buy a wreck of a home, gut it and rebuild it. This is the best way, as you get the benefit of cheap property since no one wants to deal with tearing down rotted housing. Save what you can of the structure, and rebuild. Generally you can double your money when you finish.

Most importantly pay cash. Don’t take out a mortgage. Self insuring becomes a possibility then. Just be sure to take liability insurance, you need that imo.

Zero Interest Rate Policies for 15 years, printing money causing general inflation, combined with real risks, all adds up to Insurance Companies balance sheets getting hacked to pieces as bonds collapse in value and real money has to come from somewhere to pay claims.

Greenspan, Bernanke, Yellen and for a while, Powell, were the Carnival Barkers while the American self-appointed elite robbed the cupboards bare.

No refund, no return, no rebate, no reward. Time to rethink the entire ‘mortgage’ concept.

I lived in Florida as a teenager and still have friends there. So, I strongly considered during Covid moving back into the area where my family had lived and where friends still live.

I looked at houses available and actually called a couple of realtors about listings. One problem was a shortage of anything affordable in reasonably good condition, but the biggest problem was when I checked what the insurance costs would be on the listed housing. That was 2 years ago and insurance has only gotten more expensive.

Insurance costs have gone up and up in recent years all over the southeast US, but Florida’s costs are among the highest.

As an aside with no science behind it, I have been seeing more Florida plates here in the Phoenix area of late. Maricopa County and close by towns of neighboring counties are growing in population as never before. No natural disasters to speak of, other than the storms known as July and August.

Sssshhhhhhh!

Don’t tell more people about our paradise!

Not exactly a “natural disaster”, but in the Phoenix area starting some time in May, temperatures climb to unbelievable heights, making going outside after 9 am a miserable experience. These temperatures can last right through October.

Any one contemplating moving to the Phoenix area, would be well advised to rent a place during these months to see if the area is right for them.

When idiots continue to re-build over and over in a hurricane zone, insurance companies will finally say enough.

The entire state of FL is a hurricane zone…Now what?

Surprised nobody is talking about the other huge issue of non-sense litigation. There are situations where insurance companies get sued over a windshield (that likely would have been replaced) and the plaintiff was awarded $210 but the attorneys racked up 65k in legal fees which the insurance companies have to pay. I’m not saying insurance companies are angels but these blood sucking lawyers in the state of Florida have caused what would be a normal claim to become a massive lawsuit, and they know how to rack up legal fees. These costs all get passed to the policy holder.

Interesting how the Covid operation and the actions of the medical and associated insurance industries are all but forgotten now, isn’t it? All part of the fascist government/corporate plan.

Smart of them, the Communists, to essentially take over the judicial system. We see the results daily, both criminally and civilly. It’s been key, along with infiltrating the educational system, to destroying the Republic.

We still have choices though. Tough choices, sure. What kind of sand can we throw in the machinery?

Forgotten by whom?

This thread is about property insurance.

I love the anecdote shared at the end regarding Florida Crackers.

I am in insurance Risk Control. Very specialized insurance not related to PD, flood, or general casualty. We are a member company funded and controlled- we are generically considered an Underwriting firm, not a typical insurance model.

I share because I want to back SD up regarding the comment about investors.

All insurance utilizes “funds” of money to ensure they can cover their losses. Companies like Farmers have multiple “funds” for their various products. Insurance companies manage their funds as a separate function of operations- not associated with Risk Control or Underwriting. I don’t know how Actuaries tie in since that is not my cup of tea. Funds are managed purely by finance folks- Controllers, accountants, money managers, etc. Most large firms have internal money managers who move monies to ensure they get the best return on their investments, typically large portions of the “fund.” Small companies hire firms like Blackrock, Vanguard, or similar companies to manage their assets.

Farmers may or may not utilize the big firms to manage pools, or they may keep it internal; I don’t work there and don’t know their processes.

They fill their funds via two means: premiums and member company investments. This is especially true for Mutuals and Captives:

Mutual: A mutual insurance company is an insurer providing collective self-insurance to its insured members.

It has no shareholders and is owned and controlled by the insured. By pooling their risks together in a mutual insurance company, Members (the insured) can take control of the extent of their insurance cover and obtain it at cost. USAA is an example of a mutual, as is Liberty Mutual (liberty biberty). They may be less susceptible to outside influence (unless they utilize external money managers such as Blackrock). Less but not immune because the insured is the member and typically the sole source of money less the investment returns. For total clarity- either company does not employ me, so I can’t speak to the nuance behind the scenes. I am providing generalities.

Captive: an insurance company wholly owned and controlled by its insureds; its primary purpose is to insure the risks of its owners, and its insureds benefit from the captive insurer’s underwriting profits.

It sounds like a mutual, but there are differences. Rather than a long explanation here, this article does an excellent job of differentiating: https://www.captive.com/captives-101/what-is-captive-insurance.

I apologize for the very high-level generic explanations. It helps contextualize why Farmers is pulling out and why SD said investors will come in to buy the properties- they are the money managers.

Those member companies who invest want returns. They are using the disasters associated with living in Florida to validate premium increases (which is fine if it aligns with actual losses and claims paid to each insured- it’s how they maintain appropriate funds to cover claims).

Farmers is a traditional member company driven firm. But, without being an insider at Farmers, I am guessing that they are receiving external pressure to drive premiums to a level where their investment companies have no fear of losses and the returns on their investments stay favorable. The insured must make up the difference.

These pressures can’t be avoided because if you think premiums are high now, they will be even worse if major member companies decide not to participate going forward—a double-edged sword for the insurer and great for the investors.

Again, I apologize for such a very high-level, somewhat inadequate explanation. This can be a highly complex system of money and my goals was to provide a general understanding.

Hey Dwayne…good explanation. Only one clarification. Farmers Insurance and USAA are both reciprocal insurance exchanges. It’s like a mutual insurer but the policyholders are literally insuring each other in a reciprocal. There are also different management structures (attorney-in-fact runs a reciprocal vs. mutuals who can vote for their board and even some can vote for their senior officers) and income tax treatment.

And I’ll elaborate on actuaries. They are key to understanding the losses of an insurer and how the insurance company should set its rates. They complete sophisticated analysis on the insurer’s book of business and develop models to analyze policyholder loss and risk data. They also use catastrophe models from outside vendors that are widely used by P&C insurance companies (like AIR and RMS as just two examples.) Actuaries are very important math nerds in the business. Most of the actuaries on the P&C side come from the Casualty Actuarial Society and have to complete a series of professional exams in order to earn their Associate or Fellow designations. There is also the American Academy of Actuaries and the Society of Actuaries. Super smart professionals and their journey to become an actuary is pretty grueling.

Thanks!

So the question is, how much of those actuarial models use the bogus climate change hoax theories to set rates. Ie, sea levels rising, increase in big storms, more wildfires vs the reality of sinking land, decrease in number of storms, arson etc etc.

Well, that’s a very good question. There are different kinds of models used. Most of the actuarial models are data driven by actual loss information, loss trends, and industry data that has nothing to do with climate. The catastrophe models are a little bit of a black box, but what I’ve been able to discern (my opinion) is that there is more climate hoax in the news than these private models. There is a tremendous amount of science and actual data behind them. You also have competition between the various purveyors of private catastrophe models and estimating wrong can be harmful to your CAT model bottom line. Most large insurers and reinsurers will run multiple models, have some proprietary analysis of their own to price things accurately, and tilt the rating process where they feel comfortable (i.e. 95% confidence level) in their scientific wild ass guess (SWAG Method.)

Now, having said all of that, don’t for a minute think that the insurance trade press isn’t filled with climate hoax stuff in order to keep the narrative flowing. I mean, it is in the industry’s financial interest to have some joyous terror to wring our hands over. Every year, the reinsurers say the sky is falling…they have been for the 3 decades I’ve been aware…and insurance companies do try to push as much rate increase past the various State insurance departments as they can. Make hay while the sun is shining, as it is said. Most insurance departments require extensive analysis of rates and the data behind it, and sometimes, even when a rate increase is justified, the department will say “no.”

Without putting the scientists, actuaries, and computer nerds that program the CAT models on an Inquisition Era stretch rack, there is no way of fully knowing what goes into it as it is proprietary to each company. The only saving grace is that state insurance departments do get nosy about those models because the CAT model output is often part of the rating increase request. And, some state insurance departments rely on those models, as well.

Insurance companies are pulling out of Florida because of fraud. Don’t get caught up in conspiracy theories on this one. https://market-ticker.org/akcs-www?post=249227

What the difference between insurance companies and a Ponzi scheme ?

A lot.

The real bullbleep here is that “insurance” is mandated by law- but the law does not mandate insurance companies to provide coverage. Therefore insurance should not me mandated.

Furthermore I consider “insurance” to be a tax and not a value added product.

Most states’ laws only require you to have what ever insurance is available on the open market- if there is none available, you are not legally required to have it. Some states require the insurer to be based in that state. Most major insurers have offices and licenses to provide coverage in most but not all states. Some avoid certain states- like Farmers is doing in Florida.

The decisions to provide coverage in state is not always driven by funds, monies, or excessive claims (which is what Farmers is alluding to in this case). Sometimes it is due to certain state specific regulatory requirements, which most often, drive premiums or in some cases force coverages for which the insurer is not prepared to cover.

A tax? Interesting. Insurances saves peoples lives and asses.

You would think differently if you ever caused a car accident that resulted in either a death or serious injury to yourself or others. Without the insurance, kiss your assets goodbye. No more house. No more car. No more bank account. You will be forced by the courts to cover the costs all by yourself. Yes, the injured or aggrieved would have to sue but you will lose if you are at fault. Additionally, the insurer provides the legal cover for the claims defense. Yes, you should get your own lawyer (because you need someone to represent your interests not the insurers) but the insurer’s lawyer will do the heavy lifting.

You would also think differently if you lost your house in a storm.

Now, yes, some of the companies suck regarding how they handle claims. Some suck bigly. But then, that is on you, the consumer, to do your research. It is also on you the consumer, and purchaser of a policy, to ensure you buy adequate coverage. Most people don’t do that….they choose the cheapest insurance regardless of their budget. Then they cry when it is not enough to cover their losses.

When you go to buy insurance it is important to understand the value of your assets, ask the right questions, and then purchase the appropriate coverage. If the polices provided by the insurers is insufficient- then you need umbrella coverages. Most of us, myself included, are very under insured. It’s a balancing act.

Not value added…until you need it.

Some States may require That if insurance companies offer car, life, or just fire and theft, then they must offer wind and hail.

It is my understanding that what sparked this exodus of insurance companies was excessive liability claims. Florida law permitted plaintiff’s attorneys to recover bloated billing rates when they won property claims against insurers. This was supposedly fixed in a special legislative session last year.

Then, more recently, since the sooper geniuses at the Fed have cranked interest rates up so fast, insurance companies and other institutional investors have gotten crushed with losses on their bond portfolios. This is not only a Florida problem, but it is the cherry on top for sure. And, of course, Ian losses were an owie.

Dunno what the fix is, but it’s hard to lay this at the Governor’s feet.

This, thank you, it adds to my comments above.

I think what everyone is laying at DeSaster’s feet is his lack of any tangible action to find a fix.

I assume this is due to both economy and supply chain as costs of repair are skyrocketing? Combine this with Florida being prone to frequent hurricanes, I have to wonder what building strategies people employ to avoid their buildings being destroyed with each storm? I would think bunker-like structure for a home would seem appropriate. Heavy and deep slab with iron frames and heavy reinforced cinderblocks for outer wall construction? It could be made to look normal with outer fascia and internal walls would still be built with wood and drywall.

Why do I doubt that this is done in Florida very often? If I were to live there, that’s more or less what I would have done.

IDK, elements of construction were part of my business for decades and I’ve been purchasing the raw materials for it since the 1970’s. My basket of ‘stuff’ that a typical consumer would use to perform construction tasks, with a bump during Covid, has slid back to near Trump era levels.

That leaves labor. People are greedy. As greedy as the market will permit. My solution? Don’t support greed. Do it yourself. At some level that takes the willingness to go to war with government; the oppressor. Some of us have been at war with the humans in government for decades. It simply hasn’t gone kinetic yet. Since most citizens get along to go along, playing the game to grow their own pile, government overreach has grown by leaps and bounds. If Covid and actions since haven’t rammed that reality home, heck I don’t know what will.

Our elemental freedoms have been trodden upon by other humans. It’s accelerating. But hey, cut the grocery budget to pay the tax man and fluff the profits of the humans in the insurance industry. That’s America. Apparently.

Funny how you don’t mention one of the biggest problems, the roof.

In FL, the walls don’t usually collapse. It’s usually the roof goes and the inside gets drenched, or the storm surge picks the house apart.

Storm surge will obliterate a concrete or block wall. I’ve seen it happen. It’s why many houses along the coasts are built on stilts.

Power industry is raising the rates because they don’t use cheap fuel to power the generators, the power industry is also run by environmentalists, it’s their way of forcing us to use green useless energy.

The vultures swooping in is nothing new. They did so in post WW1, bought up properties for pennies on the dollar, cast the world into an economic collapse that ultimately sewed the seeds for WW2, especially in Europe. Then they financed both sides. But we are not allowed to acknowledge these facts, by the ones who perpetrated this. As the bodies stacked up, so did their profits. Nothing new under the Sun.

Adding to that misery is the standard response from flood insurer-that water damage is from wind or homeowners denying claim stating that the water damages from the torn up roof is really from flood waters which happened at the same time but not at that place. Carriers should not be allowed to cherry pick covered products , like auto not home, IMO.

You know, that there is a “water line” when most flooding occurs, right? The Flood insurer will typically go 1 foot past the flood line for their consideration. Anything, coming from the top down, through the doors, through the windows etc goes to the wind related coverage. It is really not all that hard.

Also, people outside of Fl are sympathetic to carriers believing Florida has a lot of damage. Here are some data about claims paid:

https://www.iii.org/fact-statistic/facts-statistics-flood-insurance

More of Ron’s legacy just unfolding before our eyes. Guess the campaign script regarding his successes as Governor of FL is going to undergo a rewrite. But this is what to expect from a political facade who attempts to put the screws to Disney and ends up getting humped by Mickey Mouse.

I do not live in Florida, but energy and insurance prices are rising everywhere. I call it the delayed calamity of inflation. Inflation amounts to nothing more than a big tax increase so the Government can guarantee itself a bigger share of the GDP of the working classes. Here in Colorado, we are seeing large increases in every tax, right down to even sales taxes, because of inflation that has already occurred. This is why our economy is in the dumpster. The insidious thing is that incomes never keep up with inflation and that is where we are. The flooding of our country with indigent illegal immigrants is also putting downward pressure on incomes. A double whammy that cannot ever be completely recovered. Most folks just learn to live with the conditions and get on with their lives because their neighbors aren’t doing any better either.

The Government can blow all the smoke they want to about the great economy, but it will only get worse, like it has been doing for over 30 years. Only the Government benefits from inflation. They continue to bake in a 1-2% inflation rate every year by printing money they never had and spending it through Wall Street investors.

My question is, why do the people always vote for more free stuff, when nothing is ever free for working people? Government intervention in the marketplace is always a ticket to another horror show.

Exactly.

Fed money printing/NIRP….gov’t debt. It’s been working overtime since the 1960s.

I would only add that this inflation also greatly energized the move of industry and jobs to China and other places in Asia in the 90s and 2000s.

We all know that “they” used covid to do a lot of damage to us, our country and the world.

For the last few weeks my husband has been saying “they” also used covid to raise the prices on everything.

Instead of starting a war — which had been the standard for raising prices across the board for decades — “they” started a planned-demic to raise prices as high as they can go.

I believe they took political advantage and made it a plandemic. They caused a tremendous amount of inflation by shutting the economy (the supply chains) and forced everyone to shop at a handful of big corporations. Those corporations immediately saw the windfall if they started boosting prices for the goods over which they had monopolies on the supply. The upshot is, yes the plandemic caused lots of inflation because the Government spent over 10 trillion dollars they didn’t have in order to prevent the total collapse of the economy due to the shutdowns.

But the shutdowns were politically inspired and, with them, the Demcommies destroyed President Trump’s chances at re-election. The people always vote their pocketbooks, and Trump could not overcome that political fact. That plus the fact that most voters are blissfully ignorant when it comes to how the Bureaucratic State operates.

Trump didn’t lose because of lack of voters. He “lost” thru cheating.

Don’t play their stupid games.

Neither my parents nor my grandparents had fire insurance or homeowners insurance or car insurance. When I first was driving there was no requirement for car insurance. We now are forced to have car insurance. The property we now have was first built on in 1911. We bought it as a clear cut in 1992. Three houses burned down on this property before we bought it so we built our house of cement block filled with rebar and poured concrete with a metal roof. so we do not insure. earthquake insurance is way too expensive anyway.

Look at the data on the surest paths to personal bankruptcy! Hurt/Kill someone in an accident and you are permanently screwed if you aren’t covered up to your earlobes.

we do have liability insurance. $250/year

My post was intended as a “don’t get your hind quarters in the ringer.” I went through all the logic on this stuff when I finally hired a financial advisor four years ago. I too thought I had a strong command of the subject. Turns out, like many things, if it’s not one’s field or research interest you can and will miss things (i.e., the rank ordering of risks; which risks need to be considered).

I think that , if your assets are in a revocable trust, you may be safe from asset seizure bc of a law suit.

Yes, you’re absolutely right. The corrupt judicial system has constructed it that way to enrich themselves. Smile when that private jet flies over. They thank you for the fuel 🙂

Too bad our governor is too interested in his failing presidential run to pay attention to this critical issue here in Florida.

Contractor and Insurance collusion that reached peak insanity. The state regulators turned a blind eye too it because it increased the GDP of the state.

We own two houses in FL..lots of my friends and workers got in on the roof scam in NC FL..we didn’t..My one premium did not go up..I’m waiting on te other. Both my cleaners are working under the table and collecting $$$ for kids, food stamps, free cable, free medical, utilities..it makes me sick..they are living in 300000 houses and both spouses are self employed.

What regulations are driving the monstrous increases? I ask to understand the larger picture.

I live in Michigan and our auto and homeowners rates are ridiculous too (IMHO).

Well, this won’t have any repercussions s for a certain Governor, will it? Sarcasm fully intended.

Health care and life insurance are completely separate businesses with their own set of issues that have little to do with the property-casualty insurance business. Yes, people can lose their lives and get injured in a hurricane, but Farmers Insurance is reducing its Florida property-casualty business. You’re welcome to be mad at all insurance companies but I’d recommend understanding the different issues these industries face.

It’s a year old but might shed some light for my fellow Treepers about the Florida property-casualty insurance business.

https://floir.com/docs-sf/default-source/property-and-casualty/stability-unit-reports/july-2022-isu-report.pdf?sfvrsn=34f77ed6_2

Page 10 explains in a simple bar graph that property-casualty insurance isn’t a scam but a money-losing business in Florida.

Some easy math to demonstrate it: Coverage A for your homeowners policy is $500,000 and Coverage C is 50% of Coverage A (or $250,000.) No other property in this example. Let’s say the insurance company charges $15 per $1,000 of coverage, or $7,500 of premium in this simple example. The total limit that the insurance company is potentially on the hook for? $750,000. Without taking into account inflation (i.e. increase in rebuilding costs, code enforcement upgrades, or surge demand for construction materials after a hurricane) the insurance company will have to collect $7,500 each year for 100 years in order to collect enough premium to rebuild the house and replace its contents exactly once every 100 years. But what about the salaries of employees, reinsurance costs, hiring lawyers to defend against litigation, federal and state income taxes, and policyholders’ committing insurance fraud, among other things? Yeah, that’s extra.

Let’s say you’ve paid your insurance company for 20 years and not had a single loss…and they drop you. Well, if you had set aside that $7,500 and self insured for 20 years, you would have $150,000 (plus investment income.) Again, this assumes you’ve dodged every hurricane/wind storm in the last 20 years. You would be better off self insuring, obviously, and you’d have a nice little nest egg for a (literal) rainy day. But, you’re now in the insurance business and you have a significant risk of loss during hurricane season every year.

My advice? Ask for premium pricing with higher deductibles. Maybe 5% or 10% or even 20% (on the Coverage A above that would be $25,000, $50,000, and $100,000.) I am certain your insurance premiums would not increase as much. Sometimes insurers will offer a higher dollar instead of percent deductible. Take it and start setting aside for your future losses. Florida is not like any other state in terms of catastrophe losses. It’s the worst. Also, move inland. Sure, ocean views are the best but people should pay for their own risk of loss without others subsidizing them.

What to do about the poor and middle class in Florida? Insurance cannot solve that and I don’t have any great ideas, either.

“Also, move inland. Sure, ocean views are the best but people should pay for their own risk of loss without others subsidizing them.”

Couldn’t agree more.

In theory, insurance pools resources based on event probabilities and expected costs. Again, in theory, this serves to lower annual insurance cost across the pool. So, self-insurance could prove to be more expensive. Correct thought process? Again…”in theory”.

I would guess that part of their profitability ‘problem’ may be related to the strong influences of their woke financial overlords forcing them into DEI, GND and ‘social equality’ investments that are beginning to be widely rejected by the sane amongst us.

DeSantis getting great results for his owners!

I am with you, desertson, but please don’t overgeneralize vegans.

I have always been a Patriot. Since he came down the escalator 8 years ago, I’ve been a staunch Trump supporter have been to 14 Trump rallies, and he signed my MAGA hat.

I’ve also been a vegetarian (not vegan) for 46 years. Hence my handle VegGOP. And I’m not the only vegetarian in our Patriotic midst.

FYI, the dietary difference is that vegetarians (like me) DO eat diary products and honey that come from animals but do not require killing them. Vegans avoid all animal products.

Agreed. I migrate between vegetarian and paleo depending how my body feels.

I’m not and never have been “vegan”.

I thought vegans were from the star system of Vega.