Homeowner equity is being erased. As higher interest rates continue to put pressure on borrowers, the ability of the average person to afford a mortgage diminishes. Higher mortgage rates lead to downward pressure on residential home values as fewer borrowers can afford higher payments. Simultaneously, commercial real estate is dropping in value as vacancies continue increasing.

Put both of these issues together and already tenuous banks holding mortgage bonds as assets can become more unstable.

Put both of these issues together and already tenuous banks holding mortgage bonds as assets can become more unstable.

This dynamic creates the continual tremors in the background of an economy already suffering from high inflation and low consumer purchasing of durable goods.

A perfect storm starts to realize.

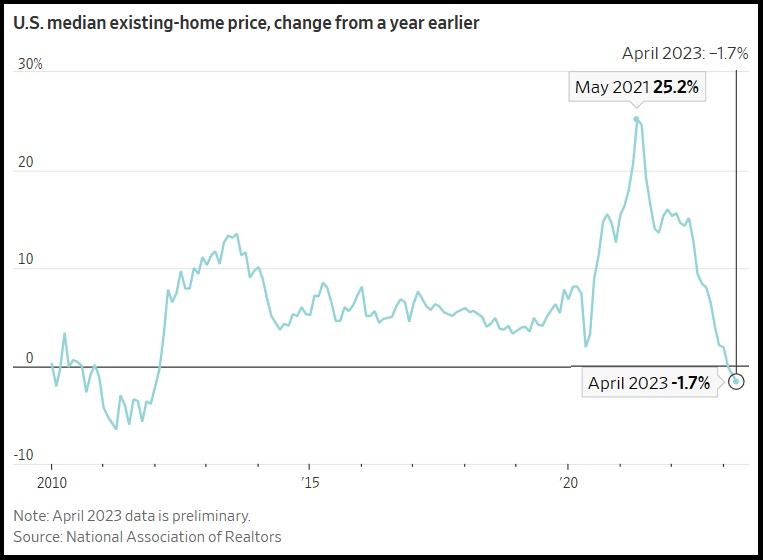

(Wall Street Journal) – Sales of previously owned homes fell in April from the prior month and prices declined from a year earlier by the most in more than 11 years.

U.S. existing home sales, which make up most of the housing market, fell 3.4% in April from the prior month to a seasonally adjusted annual rate of 4.28 million, the National Association of Realtors said Thursday. April sales fell 23.2% from a year earlier.

The national median existing-home price fell 1.7% in April from a year earlier to $388,800, the biggest year-over-year price decline since January 2012, NAR said. Median prices, which aren’t seasonally adjusted, were down 6% from a record $413,800 in June. Home prices have fallen the most in the western half of the U.S., while prices continue to rise from a year earlier in many eastern markets. (read more)

Before looking at today’s graph showing median existing home values, remember me saying this in 2021?:

“I said in June, at a macro level home prices had reached their peak (last two weeks of May, first two weeks of June was apex). Obviously, there are some geographic home value increases still happening as COVID related regional issues and work opportunities are shifting populations. There is also a lag and ripple effect that takes time to work through the economy. The macro-apex will not be visible until next year.”

When I said that in 2021, people said I was wrong. Well, with hindsight now visible within the data as it is reflected, look at the result:

May and June 2021 was the peak of year-over-year percent of change in median home value increases.

So, what was going on?

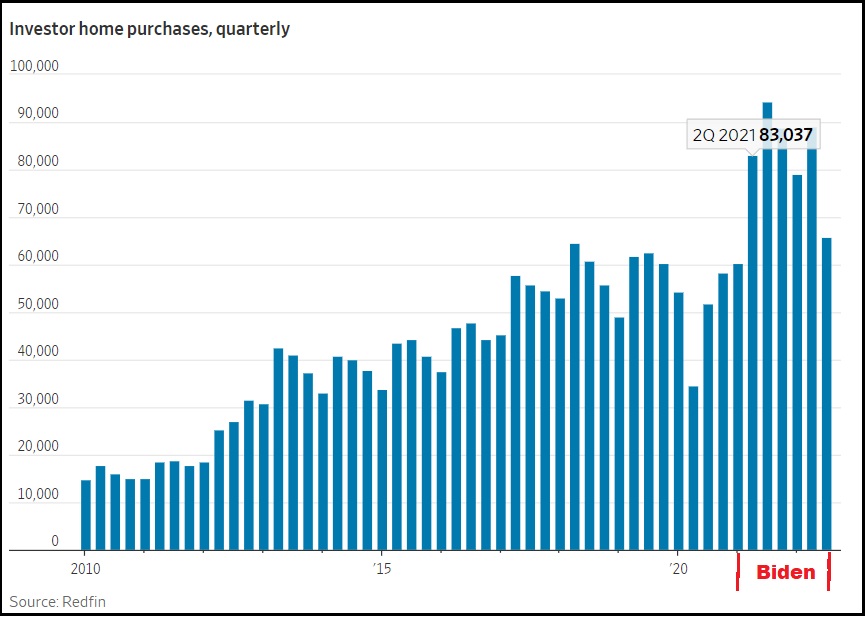

As CTH outlined in 2022: If you look closely at the timing (keep in mind the data reporting lag) what you will notice is that financial institutions began a big surge in purchasing hard assets, specifically real estate, as soon as Joe Biden took office (Jan ’21), and the economic policy became evident. Intangible financial instruments became an immediate risk as the professional financial control groups recognized energy policy would drive inflation (supply side) and devalued money would fuel it (demand side).

As an offset to predictable inflationary policy (the insiders’ game), institutional money (Blackrock, Vanguard, etc) was moved into hard assets with tangible value.

This shift in asset allocation, institutional sales, helped fuel a false surge in home prices and their valuations. CTH was writing about this in 2021, and sounding alarms as it took place. 25% of all real estate purchases were being made by institutional investors.

We The People got screwed.

The dynamic was predictable. The Biden administration economic policy, energy policy and monetary policy, was going to cause massive inflation. CTH was shouting about it in early 2021 and warning everyone to prepare for waves of price increases that would naturally surface first on high-turn consumable goods, and then embed into longer-term durable goods.

Despite claims to the contrary, this 2021 inflationary explosion had nothing to do with the pandemic or supply chain shortages. It was entirely self-created by western governmental policy – the collective ‘Build Back Better’ agenda. You can see now from the background moves within the financial sectors, they too knew the reality and their money shifts reflected that despite their ‘transitory’ pretending they were mitigating their own exposure.

We the People were yet again going to be victims of specifically intended monetary, regulatory, energy and economic policy.

We the People were yet again going to be victims of specifically intended monetary, regulatory, energy and economic policy.

The investment class rulers of the WEF assembly shifted assets to avoid the pain that we would feel. We “would own nothing and be happy,” and their shifts would position them to own everything and be in control.

Overall govt spending and regulatory controls drove inflation for these past two years. The ‘demand side’ was blamed, despite the lack of demand. I will be proven right when history is concluded with this. Interest rates were raised by central banks in an effort to support the policies that are driving ‘supply side’ inflation – not demand side.

Energy policy was/is crushing the consumer by driving up the cost of all goods and services. To support the overall goal of changing global energy resource and development (a false and controlled global operation), central banks raised interest rates. Various western economies, including our own, have been pushed deeper into a state of contraction by central banks crushing consumer demand, and eliminating investment via increased borrowing costs.

In short, the goal was/is to lower energy consumption by shrinking the economic activity. This, according to the BBB plan, was needed at the same time as energy development was reduced. These economic outcomes are not organic, they are all being controlled by collective western government agreement.

Within this control dynamic, there was always going to be a point where the reaction of the people to their economic reality means the financial control elements need to shift direction. They will always maximize profit and minimized risk, while knowing what the larger objective remains.

Just like every other durable good, housing demand contracts as prices and costs become unaffordable. The loss of equity within your home is damaging to your own value or ability to borrow against it.

From the perspective of an institutional asset, that same equity drop is an investment loss. However, the investment loss is not materialized until the sale of the lower valued asset is completed. Retaining declining real estate on investment books creates an artificially high appearance of the investment result; unless and until the real estate is sold at a diminished value.

As mortgage rates rise, just as a consumer would pull back from the housing market, so too will institutional investment groups now control the slow dumping of the asset to remove the equity they pumped into it. Much of the investment housing will be retained as rental housing, with the monthly rents being part of the returns on the investments. However, as this dynamic unfolds, further investment purchases of houses stop, because the asset overall is declining in value. This halt of investment activity also worsens a steeper drop in home values.

https://www.rocketmortgage.com/learn/property-taxes-by-state

And wasn’t it convenient that property taxes also went up along with the arbitrary inflation.

FYI, housing prices will also always reflect the illegal immigration policies of a White House occupant. It inflates them, because of demand, but it is 100% artificial since WE are paying for it too and that cannot last forever.

But they don’t care.

It’s a windfall for overpriced real estate markets in Blue states.

Windfall anywhere, red and blue states.

When you protest property tax increases, the local bureaucrats complain their costs are rising and claim they “only” raised your tax by the rate of inflation. When you point out, only government employees get COLA raises anymore, they stop listening (if they ever were).

Here in Fl soon your homeowners insurance will be more than your property taxes…

In NC, my property tax for 5 acres,3500 Sq ft house $1830/yr including trash. My homeowners with wind/hail is $3600/yr. Not just FLA.

Edit not working. Many here with no mortgage, drop their wind/hail. My regular homeowners is 800 year. It’s the wind policy that’s ridiculous . AND if it is a “named” storm the deductible is 10k.

Yes, mine went up too. Everything is going up under “Let’s go Brandon.”

That aspect may also price people out of home buying too.

In Kansas my property taxes on my home, value about $400-450,000 is $4100 a year and my home insurance is $2900 a year. It amazes me I spend almost $600 a month to own my home. Thankfully it has been long paid for.

I suggest that insurance companies are raising rates nationwide to help pay for the hurricane damages in Florida. Mine were $2600, up from $600 in 1984.

And smart money has gone to GOLD. Gold is a great way to preserve wealth.

Late in the game now, but probably still worth it considering where the Bribem regime is taking/tanking the economy. Should have bought in regular intervals over time; up or down economy. In the last decade or two, I think my average price paid was $1400 an oz. Today gold is around $2000. If you sell it, you lose 10%, so 2000 – 10% (200) is $1800 which is more than I bought it for on average. Of course inflation probably ate a lot of that up, but just sayin’.

If you can’t afford gold, try silver as well as a long term store of wealth. The key is to invest a little every month over long periods of time so it averages out. Waiting for a crisis to invest in metal doesn’t usually work out well.

I have to ask, if the world economy fails and people stop using gold to make things, what is it’s value?

All real estate stories are local. Like most issues today, it’s all about geography. Where you live is most important today. Stay out of the blue states and cities whenever possible.

Exactly. Out taxes on our casa are approximately $44 USD. Yes 44$ . Viva Yucatan!!

Those with the ability to make waves make money on the way up and the way down. The little guy has to act defensively to try to protect his wealth.

It’s a function of interest rates. Real people have budgets. May a budget of $X for a mortgage. If the interest rates go up, the price of the house goes down or real people can’t afford it.

Here in Bel Air, MD (a suburb about 30 minutes northeast of Balt), housing prices are either still rising a little or have peaked just about now. Average price is around $400K. People are swimming with money here. Still competing with all-cash offers and people are still waiving the inspections. People are no longer offering over list price, it seems. Can’t really tell for sure because there are so few houses on the market.

The price of new construction is ridiculous. Starts at $650K and goes to $850. People are paying it. Crazy.

Yet, despite a tanking housing market the thieves in state and county governments have added insult to injury to their reprehensible Lockdown that destroyed livelihoods by jacking UP property valuations – in our case and most county residents – 40 percent. (Not a typo) Residents now get to waste our valuable time developing a proper ‘comp’ valuation protest to undo their slight of hand thievery in the hopes the bank robber will show mercy and throw us a reduction crumb.

These people are thieves and criminals, this being their mode to refill the “lost revenue” hole they dug by destroying businesses and commerce over the past three years. Special place in Hell…

The County govt’s jacking up Property valuations way above normal prices are an Organized Govt’ Racketeering family feeding on the backs of the rest of us.

Hey Sundance, if the average person cannot see that not drilling for our own oil will cause prices to skyrocket, there is no chance for those who can see. You must know this…

Increased property tax = reduced home price / value

Correct.

So they win six ways from Sunday.

1. Prior to 2008 They drive up housing prices and make tons of money on mortgage commissions and fees to make bad NINJA loans to millions of people they know will have to default. These Home buyers are basically “renting” from them until they sell or default.

2 Market crashes. They collect billions on QE and suffer no pain for bad loans. Taxpayer foots the bill.

3. They scoop up discounted properties from defaults and foreclosures.

4. They increase property tax percentages because boo hoo not collecting enough tax for schools and services. No one complains too much since home tax assessment values went down … so overall… property taxes don’t really go up. Yet. (But we all know that increased percentage won’t be reduced when home prices go back up).

5 They drop the interest rates, collecting billions more in mortgage commissions and banking fees. Low rates fuels a housing boom and they now unload at high prices the foreclosure distress deals they generated and collect big profits.

Good gig. Trick people into buying a house from you they can’t afford, allow them to make your payments then when they default, you get it at a discounted price. Drop the interest rates, fuel a housing boom with low rates, pass go and collect $200 gazillion.

6. Have the construction industry fund the construction of the massive commercial multi family boom

7. Benefit by capitalizing on the low interest rates you issued to generate a housing boom to get those 2008 distressed properties off your hands. Sell at the top of the bubble, making the bubble bust even worse.

Drive up inflation, taxes and interest rates and people can’t buy into the housing market, so you rent them those commercial and multi family buildings that the construction people funded for you.

Keep interest rates high so People can’t afford to move up, further decreasing current housing supply. But inflation will cause many to be forced to sell and find a new rental.

And.. oh look who will be scooping up the crashing commercial real estate market! You can’t afford to buy, so you will rent. Probably give them billions in subsidies (tax dollars) keep rents “reduced”.

Rinse, wash, repeat.

That suck noise you hear is the monies coming out of our economy. You borrow $1000 and now there’s less monies in the system to pay it off. And you have 5.5% inflation making your other funds buy less.

In other countries they accept US dollar. Most citizens know the exchange rate of their currency to US dollar. This will not always be.

Now ask yourself, in the future, what will US citizens be asked in exchange for US dollar?

It’s a serious question and one you should start considering for your own future and that of your family.

From WSJ article posted ks by Sundance above:The national median existing-home price fell 1.7% in April from a year earlier to $388,800, the biggest year-over-year price decline since January 2012

Hmmmm It Seems like major financial crisis bubbles pop in election years:

2000 dot com crisis

2008 subprime mortgage crisis

2012 see above & Solyndra

2016

https://www.nytimes.com/2018/09/29/upshot/mini-recession-2016-little-known-big-impact.html

Rigging elections must be expensive. Creating crisis as a source of money transfers and laundering through “loss”?

Another factor is inventory if no one is selling in your area the prices stay high. We just sold a home and got the high rate of 2022.