The Bureau of Labor and Statistics (BLS) released the August review [DATA HERE] of producer prices for last month. August rose 0.7% with cumulative results now showing an 8.3% increase in prices; the largest year-over-year jump in prices for final demand products in the history of tracking. The prior record was July with 7.8%.

Inflation is skyrocketing for consumer goods at all levels of production: Origination (commodity/raw material), Intermediate (Mfr/Wholesale) and Final products (retail).

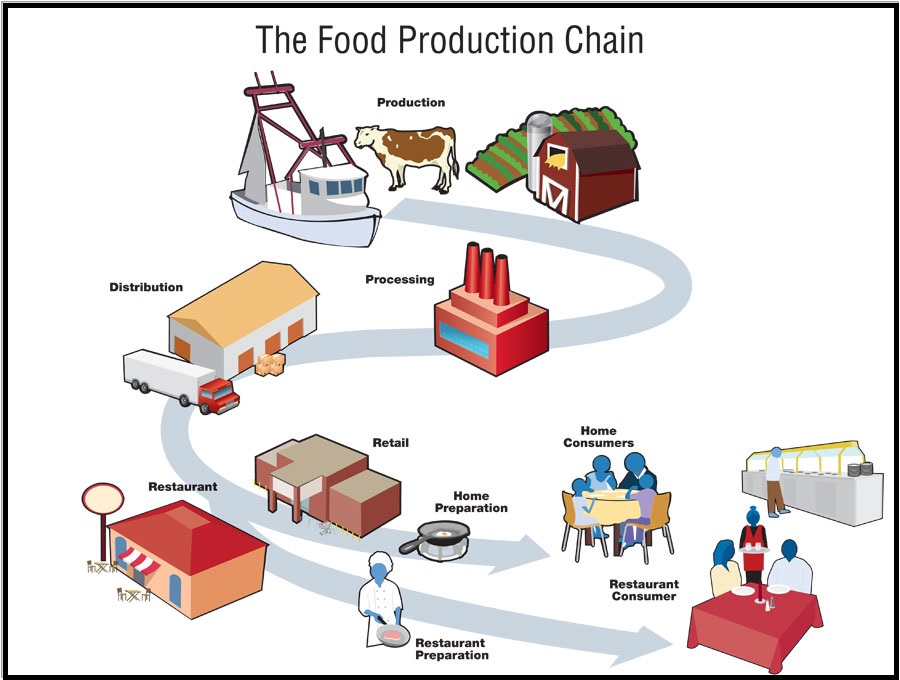

In part, the extreme upward cost pressure from escalating fuel and energy costs are accumulating throughout the supply chain and surfacing in the prices of the finished products. We are all witnessing this in the prices at stores; especially in the quick turning products, like groceries (fast turn consumable goods), which reflect price increases the fastest.

In part, the extreme upward cost pressure from escalating fuel and energy costs are accumulating throughout the supply chain and surfacing in the prices of the finished products. We are all witnessing this in the prices at stores; especially in the quick turning products, like groceries (fast turn consumable goods), which reflect price increases the fastest.

Final demand prices moved up 0.7 percent in August, 1.0 percent in July and 1.0 percent in June. The year-over-year inflation rate on final demand products now stands at 8.3%.

MEDIA – […] “The data comes amid heightened inflation fears fed by supply chain issues, a shortage of various consumer and producer goods and heightened demand related to the Covid-19 pandemic. Federal Reserve officials expect inflationary pressures to ease through the year, but they have remained stubbornly persistent, with Friday’s numbers indicating that the trend likely will continue.

Excluding food, energy and trade services, final demand prices increased 0.3% for the month, below the 0.5% Dow Jones estimate. Still, that left core PPI up 6.3% from a year ago, also the largest record increase for data going back to August 2014.

Final demand services rose 0.7% for the month, thanks to a 1.5% gain in trade services, or the margins received by wholesalers and retailers. Transportation and warehousing costs surged 2.8%.

About one-third of the overall gain came from health, beauty and optical goods, which jumped 7.8%. Prices related to outpatient hospital care held back the gains, falling 1.5%. Prices for final demand goods rose 1% for the month, pushed primarily by a 2.9% gain in foods which in turn came from an 8.5% surge in meat prices. Slaughtered poultry prices surged 11%. (read more)

The skyrocketing prices at the grocery store are predictable based almost entirely on Joe Biden’s pro-Wall Street and Multinational Corporation policies. Main Street is getting hammered, and the working class is suffering as a direct result.

The skyrocketing prices at the grocery store are predictable based almost entirely on Joe Biden’s pro-Wall Street and Multinational Corporation policies. Main Street is getting hammered, and the working class is suffering as a direct result.

Their specific accountability for these outcomes is why the Biden administration is trying to distract and blame COVID-19 for supply chain issues. However, it is not COVID driving the prices, it’s Joe Biden policies that benefit multinationals. {Go Deep}

Food products are fast-turn consumable goods, and the inflation in the food sector is jaw-dropping already. However, fresh and processed foods turn at different inventory levels.

Obviously fresh foods spoil fastest (think produce, fish, meats and dairy) so they are replenished more quickly, and the thin supply chain (field to fork) passes along increased costs fast. Processed foods have a longer shelf life (boxed, canned, frozen, etc), and as a consequence, have a much larger inventory level in manufacturing, warehousing and retail storerooms/shelves. Within processed foods, there is a lag between cost increase at origination and that cost hitting the stores.

The problem identified within the current ‘producer price index’, is that price increases in the raw material and intermediate material are building into the supply chain. Keep in mind, the entire supply chain is dependent on energy costs and the fuel prices that impact transportation.

The retail consumer supply chain for manufactured and processed food products includes bulk storage to compensate for seasonality. There are over 800 commercial and public warehouses in the continental 48 states that store frozen products (2020 data). The previously processed food price increases are currently reflected on store shelves (already hurting). However, the coming processed processed food price increases will be much, much higher. We will see even higher prices on processed foods in the supermarket.

The same price increases happen for restaurants, albeit faster as they follow the similar supply chain to fresh foods.

As we predicted last month, the BigAg multinationals (K-Street Lobbyists) made deals with their congressional sales-force for increases in government welfare payments (EBT and Foodstamps, WIC etc.). BigAg lobbies congress for higher reimbursement rates so they can raise the prices of food and export domestic product to other nations. Food assistance payments increase, and BigAg benefits. In essence, BigAg takes the fed food subsidies and fattens their profit margin. Then, they payback the politicians. It’s a circle of money.

Less than 72 hours after we noted the BigAg deal was likely already done, the White House announced they were increasing Food Stamp and SNAP benefits by 25 percent. It’s a rigged game, and we are suffering the consequences. Or, put another way, “it’s a big club, and we ain’t in it.”

If the Bidenistas were deliberately trying to destroy our country, tell me one thing they would do that would be different from what they are already doing on a daily basis.

Not a thing, because they are, and it brings them pleasure. Sick.

Anarchism is now mainstream leftism. We know Antifa and BLM are mundanely violent and destructive, but take note of the tolerance, even encouragement, that the mainstream Democrats have for these formerly fringe elements of their Party.

The end of the Republicans through violence and intimidation is the short-term target, along with the corruption of the legal and electoral systems. This is the anarchistic project of Pelosi and Schiff and so many other mainstream Democrats. First smash the system, then re-build it without Republicans. This objective is quite popular with mainstream Democrats. Just ask your Democrat friends.

“Democrat friends” = oxymoron

America only works, America only survives because we can have Democrat friends.

No Democrat friends is a zero sum game. Many Republicans will switch before they fight (including, obviously, many of our Congressmen).

The lies and censorship of our disgusting news media has produced many people who live in a fog. Try to gently steer them towards the light.

Antifa and BLM and violence. Is it the government run media, or what.? Why have we not had any riots, BLM marches, or ‘city burnings’? Seems , to me, that once the coup was accomplished last January. all peace broke out amongst these scruffians.

Coincidence I’m sure

it brings them $$$$$$

I have thought that exact thing many times. Of course, the short answer is that they DO intend to destroy our country.

I think they believe that once it goes to the New World Order they will be on top of the heap. The only bright spot is they would probably be put out with the trash once their work is completed. These totalitarian type regimes never keep those who brought them – they always purge those who helped because they could reorganize against those who would rule.

Why else do you think the ChiComs pay them so well? Just as the elites in Australia have been subverted against their own people, the incompetent and corrupt American elites get rich off their grift and CCP bribes!

It wouldn’t surprise me at all to find that there are ChiCom advisors giving the O’Biden Regime exact steps for destroying US institutions like our military and healthcare industry!

This is one of those trick questions, trust me they will come up with something else next week, etc.

And yet the blinkered progressives STILL can’t see it!

Or won’t…?

Excellent!

DD

Destruction IS their plan. Its the tried and true democrat (communist) playbook. Create destruction, invite crises and foment confusion and fear. Then claim that someone else created the problem and present yourself as the only way to bring safety again.

Watched the Soviets do this in Central and South America through Cuban guerilla proxies in the 70s and 80s over and over. Same play book different faces.

Incidentally, the ONLY solution for this phenomenon is the utter and complete destruction of these people. They cannot just be defeated politically. They cannot be humiliated into surrender. They cannot be converted and won over or reasoned with. Just as the radical terrorist understands only overwhelming force, these people must be completely destroyed.

Eventually the quiet nerd knocks the bullies teeth out.

A: Give Kamala some actual responsibilities.

Getting us into another no – win war comes to mind. But I guess there’s still time for that.

Federal Reserve officials expect inflationary pressures to ease through the year, but they have remained stubbornly persistent, with Friday’s numbers indicating that the trend likely will continue.

“government officials expect” – right up there with “we’re from the government and are here to help.”

Yes, inflation is getting bad. I’ve had to downsize everything.

Yesterday I ate a Kid’s Meal for lunch at McDonald’s…

His mom was furious 🙂

Thank you Wordman for the laugh! Much appreciated.

Paraphrasing Will Rogers:

No, seriously, in my 60’s I’m now much stronger than

the strapping young buck I was in my 20’s and 30’s.

Why back then I could only carry $10 dollars in groceries,

but now I can carry $50-$60 dollars worth of groceries.

Re “Yesterday I ate a Kid’s Meal for lunch at McDonald’s…

His mom was furious.”

McDonald’s? I can’t even afford fast food anymore; so, I’ve started eating snails… 😉

Nice!

I can’t afford the gas that makes my S car go…

otherwise I’d meet you 🙂

Thanks, Wordman! Yeah, the price of gas is not exactly rising at a snail’s pace. We may even have to go back to communicating via snail mail….

Everything you wrote is true. I have a client that is a commercial food producer. I’ve witnessed first hand how he has to constantly source out new providers for his raw materials. It’s fascinating/frightening. They are good for now, but it’s getting harder. I told him he should try to order any raw materials with a years shelf life in a one year amount. Even offered to help him purchase the amount if he needed the funds.

Joebama just announced “All you damned unvaccinated are driving up prices!”

It’s a big club, and they know how to wield it.

But food prices are free for the tens of thousands of Afghans lodging on our domestic military bases.

Not free…we, the American taxpayers are paying. There is no such thing as getting things free from the government.

E.B.T.= Eatin’ Better Tonight

Finally Biden beats Trump at something.

I don’t think Trump ever got an inflation score of 8.3

I think the highest score he ever got in that category was about a 2.5

The economic policy creates massive inflation which reduces a worker’s economic independence, then the social policy dictates the same worker submit to pharmaceutical experiments or lose his or her job.

This is another reason they stopped the unemployment benefits.

To tighten the noose on the workers necks.

Another intended effect might be the sudden competition for jobs causing those willing to quit to avoid the stab to reconsider their options.

Talking about inflation will be subjected to approved narratives from the left and violators will be censored. Just like the vaxx. Once the left sees it can impose speech control over one subject area, it will apply it everywhere.

As I mentioned earlier, jobs are a lagging indicator. Even with jobs vacant due to government handouts, they will eventually go negative as people simply stop consuming because they don’t have the money.

Yes. They will label people who complain about inflation as “domestic terrorists.”

BREAKING: 1st District Court of Appeals just granted the State of Florida’s request to reinstate the stay — meaning, the rule requiring ALL Florida school districts to protect parents’ rights to make choices about masking kids is BACK in effect!

Gov. Ron DeSantis Dispels 2024 Rumors: It’s ‘Purely Manufactured’

https://conservativebrief.com/rumors-50783/?utm_source=CB&utm_medium=ABC

Bidenomics = spiraling inflation + labor stagnation + domestic social destabilization + foreign policy disintegration + gross leftardation

More windmills and solar panels = more inflation

If Joe Biden gets to know if I got injected or not, why can’t I know if he can pass a mental competence test or not?

The emperor has no brain ……

Nor soul.

The drooling idiot disgracing the White House, is the puppet. The puppet masters, will continue to make everything more uncomfortable for all Patriots. What they want is a response, if non is forthcoming, nothing is going to change. Food costs, fuel costs, vaccine mandates and any other thing that makes life miserable will be put in place. After all the fence is being put back up and the guard will be there to protect, the deep state.

“Excluding food, energy, and trade services…”

Oh, great, once you remove the things that normal people need to survive on a daily basis, the numbers are not nearly as bad!! Thanks for clearing that up for us, CNBC!

Their “basket of goods”, which is used to calculate inflation always contains the most ridiculous items. So let’s throw in, for example, printer ink, tire levers, Gorilla glue, shoe polish…you get the point. Statistics are always manipulated. For a true inflation measure the site Shadowstats is one to look at. But not if you don’t want to throw up.

I really don’t care how high inflation gets as long as things don’t cost any more.

Nice one!

$24.00 a pound for ribeye steak at the local butcher. Headed to the grocery store and found it for $23.99 a pound. People have got to be getting angry, I know I am.

Well that is wonderful news. Now Circle Back can declare at her next presser that “Steak WAS expensive, but now you are saving money!”

Lol – I see what you did there 🙂

I stopped at a local farm market and his rib eyes were only $18 a pound. Nice lookling sirloins at $12. Home grown burgers $6.50 blended with ground bacon, my favorite. We got some burgers. I am developing a relationship with a couple of local beef farmers by being a regular customer. Prices are still high but I am nearer the front of the line for availability.

On the flip side, we made a stop at the local grocer that had bone-in chicken breast on sale for $0.88 a pound. We got about 40 pounds for the freezer.

Obama handed out huge raises to federal bureaucrats, at the bottom end of the 2009 recession. His stimulus was spent saving bureaucrat jobs at the state and local levels, even creating superfluous new government jobs.

The net effect was one fallacy and one sinister perversion.

The fallacy was the new-born belief of government workers that they are immune to the vicissitudes of the American economy. Bureaucrats genuinely thought Biden could destroy the oil industry without it having a huge impact on their lives. The trite fact that oil prices effect all other prices eludes your average Democrat, particularly those in government jobs.

The perversion that now haunts us has been the conversion of all federal bureaucrats into Democrat Party operatives. The faint hope that Sessions or Bill Barr could stir the Justice Department into action against the interests of the Democrat Party was tragi-comical.

Expect a drumbeat for huge raises for government workers as this inflation crisis continues. This, of course, would exacerbate the inflation cycle. Only government cutbacks will end the cycle, but will any Democrat support this? No.

I can’t wait to see what the Social Security cost of living increase is for next year. Based on inflation figures, it should be 4-5%. Not that it matters. We’ve already had our Medicare premiums increased midyear, and that alone has eradicated any increase (as it does every year). Just waiting to see if there is another increase in Medicare on top of the one they hit us with a couple of months back. I expect to see a “Hey!! Presto Change-o” manipulation of the actual inflation number that is used to calculate SS increases. So it boils down to negative interest rates for us retired responsible savers who have no interest in joining the Wall Street casino stock market, further depletion of savings, and a Medicare consumed COLA adjustment. I’m truly not complaining. It is what it is, and we’ll cope with strategic planning. My concern is totally focused on those being threatened with job loss. Every time I think of it, I burn with a WHITE HOT fury for everyone so threatened. Everything The Imbecile (and his owners) touches destroys families across this nation. I just pray that all these governors and AGs are not just lip flapping on their promise to fight this unconstitutional mandate (not law). I suggest that they not stand on ceremony. Get their @sses out of their seats and GET IT DONE! This incompetent vicious dictator by his actions has united all patriots in ways I don’t believe he has foreseen.

Notice that they’re putting the fences around the capital building and supreme court. Apparently, national guard are being deployed again too. I wonder what they know that we don’t?

When a government wishes to deprive its citizens of freedom, and reduce them to slavery, it generally makes use of a standing army.

– Luther Martin, Maryland delegate to the Constitutional Convention

Sleepy Joe. What a disaster.

Politically, Biden is toxic. Perhaps I’m wrong, but I think the uniparty’s plan is to institute the ugly part of their scheme on Biden’s watch, then when he steps down (or whatever they have planned), roll out the “reset” as “much-needed relief” on Kamala’s/Pelosi’s watch.

Joe Run From The Podium Biden is completely responsible for all this inflation. Of course its by design- break the middle class voting block- you know, those evil Deplorables.

The plan is to destroy the middle class and small businesses, the hallmarks of healthy capitalism.

Inflation is trending at such a alarming rate (it hasn’t peaked) that demand destruction has begun. Earnings peaked Q2.

This clown car of senile idiots and America-hating Marxists is steering us directly to a GreaterDepression and THEY KNOW IT! The course is set, the correcting Federal agencies have been politicized & weaponized against us, so here we go, over the cliff. PLEASE prepare your spirit & soul for the times ahead, then prepare your pantries & stores to keep you and loved ones alive. Learn or refresh skills, acquire tools you can use, think about Victory Gardens once again, neighbor & family bonding and the needs of your faith.

Good advice for any time.

3rd quarter earnings reports drop Oct. 1st, will show further increase in inflation they cant hide.

Then there is the debt ceiling that was already reached. They must raise it or find money elsewhere or default. Not sure how a continuing resolution applies here if any care to explain.

Who said this ?

President MgGoo or Mitch McTurtle ?

Talk about winning, winning and more winning…geez, can Obama and his team still do more damage to the United States?

You bet they can and will not stop doing so until and unless another overwhelming force appears to counter such destruction.

Do you sense any opposing team coming onto the field where these evil bastards are playing? I don’t…

Btw the white house isn’t ruling out a domestic flight passport.

Yet very soon to come, and utterly inevitable, are the end of summer peak temps with sky high humidity in the south and on the eastern seaboard, and the bone dry wind whipping Santa Ana’s in the southwest where energy monopoly utility companies turn off the power for our ‘safety’. Various electricity brownouts and blackouts will likely take place across the southwest and the south and up the east coast because our Government controlled power grid is so old and dilapidated — like our POTUS. Power could be off for days at a time. You never know. So add that to the list of things that’s going to make everything else so much better. Sorry, I so hate to be glum, ever, but it is coming so be prepared for that too, just sayin’…..

YES!!!!

And even that figure is lowball BS:

Substitutions and Hedonics: Inflation Data Absurdities

Jan. 24, 2007

https://seekingalpha.com/article/24933-substitutions-and-hedonics-inflation-data-absurdities

I have long railed against many of the absurdities associated with modern Inflation reporting. Let’s take a closer look at some of the specifics.

I was always told back in the day that inflation was to much money chasing to few goods. I like driving around areas that have farms and ranches and I have noticed what were once beautiful farms and ranches are now with no cattle, no crops being harvested, empty barns and land left fallow.

I found out by doing a little searching on old Whatfinger posts that on april 21/21 the Feds started offering 1 1/2 the value of crops if farmers destroy them, if they refuse they will be denied any further subsidy’s. They did this using climate change as an excuse.

Thanks Democrats and RINOs!

Just had this note from a friend in the furniture industry. “With the lumber, foam, and finishing product along with freight cost the furniture industry has seen from 18% to 30% increases since Biden went in the WH. It is driving smaller dealers completely out of business and the larger ones are beginning to back off order new merchandise. For the reps in particular that depend on income from their sales it’s going to put a lot of them in deep debt.” He said some of the container shipping costs for furniture are now several times the cost of the contents of the container.

Any idea when the BLS plans to change the formula for calculating inflation? Surely, the clan can’t allow another month of record failure to take place! Lol?

Folks, if you live in an agricultural state and/or near a farmer, become friends with him! He, his knowledge and his farm products(meat, poultry, eggs, honey, grains, vegetabkes, fruit) will be a lifeline for you and your family. Runs both ways, too: many farmers would welcome the cash……

Amen. An example of Catherine Austin Fitts advising all who can go local. Tighten up those bonds with your local communities… people one might come in contact with normally, but oft times become friends as well as neighbors. When I lived in a small community in Wales, we had a butcher (2 actually), ditto the baker, and honest to goodness, a candlestick maker. Even people we might not know by name, we certainly knew their faces (a phrase I came to love). The sense of community was simply incredible. One can foster that sort of “small community feel” even in American larger towns and cities by trying to shop locally as often as possible, price a huge consideration I realize. I’ve done it here in our Texas city, and have gained some lovely personal connections with those who work at the businesses I frequent. In these disturbing times, a happy face or two goes a long way to making things feel somewhat normal.

Been doing exactly that. Bought some ground beef today from a local farmer.

President Trump was Correct Again…

Remember that Biden clown that said if you remove “Beef, Pork and Chicken, inflation is low” ?

That reminds of former DC Mayor Marion Berry saying “If you remove the murders, crime is down”.

These people, jeez.

I do remember being surprised that the mayor of DC was a crack head.

I was not surprised; however, that Democrat voters reelected him AFTER they found out he was a crack head.

[video src="https://commons.wikimedia.org/wiki/File:Marion_Barry_smoking_crack_video.webm" /]

Thomas Sowell on Twitter: “Inflation is a quiet but effective way for the government

to transfer resources from the people to itself, without raising taxes.”

You called it Sundance. A while back you explained it is the total of adding each monthly inflation together that gets us to the 1st part of stagflation. And of course the destruction of the middle class out put that is the second part.

Is it true that farmers are being paid to destroy their crops?

Not around here. Milk prices have been so low that farmers poured it out in desperation/protest. There are also cases in which farmers were required to destroy growing crops because they had planted in excess of their allotment.

More common and more invisible are the farmers that just decide to not grow things because it is more work that it is worth. Row crop farming (corn, soy beans, etc) is a very risky business. Converting to forage or grass fed livestock is lower stress. Some may just let the ground go fallow. If a farmer is old and every new crop is barely break even, they can not sell the place as the Capital Gains tax may be onerous. Better to just let it ride, let the heirs have it with stepped up basis and then sell it. That us the reason that the government is thinking of ending stepped up basis.

There is the joke about three old farmers sitting around at the store discussing what they would do if they won the lottery. The first said that he would pay off all of his loans and go on a long vacation. The second said he would replace his old tractors with new ones. The third said he would just continue farming like he was until it was all gone.

Thanks for you answer. I watched a video here yesterday and thought it was a spoof. Thanks again.

Not highest ever. The 1970’s were worse.

From sister in law, various meats up 30-40% per pound.

The Biden Administration: “Inflation isn’t bad if you ignore everything that costs more”

Here we go again….

I’m old now and I have seen this script play out SO MANY times in my lifetime that I’ve lost track. I have so much to say about this but I can’t. Younger people (voters) never learn until they have to suffer through a couple of big ones. They think they no more than their parents, and are oblivious about history. Wash, Rinse, Dry, Repeat.

Suffice to say, we live in an agenda driven country, as we always have. And those agendas are driven by converting a younger minority of voices by paying them to carry a loud megaphone. All bought and paid for by the oligarchs that promise a “better world”.

What these people haven’t figured out, and they never do until it’s too late, is that the only ones that profit are the oligarchs.

Why are China and Bill Gates buying all the USA farmland and ranches? They have an agenda. Don’t these young people understand that? Of course not.

Nothing ever changes. Sigh……

“My people are destroyed for lack of knowledge.” -creator God

This week stock market wiped out the past 10-week stock market gain in just one week.

Food is getting crazy high at restaurants. Even cheap food like fast food is no longer cheap. And the quality of food at even sit down restaurants is way down.

And it will never get any better, sadly….

His Fraudulency II continues to out suck himself on a monthly basis. He really is the worst President ever. And at least the previous worst of the bunch actually won their elections.

As far as I am concerned there are 2 reasons why food prices are going way up:

I got a great deal on a new product called Soylent Green. Can’t wait to try it out.