SVB is Silicon Valley Bank, the almost exclusive banking network for Venture Capitalists (VC), tech sector start-ups and tech industry holding accounts. 48 hours ago, SVB was a “grade A” Moodys rating. As of tonight, they are insolvent.

“All told, customers withdrew a staggering $42 billion of deposits by the end of Thursday, according to a California regulatory filing. […] “The precipitous deposit withdrawal has caused the Bank to be incapable of paying its obligations as they come due,” the California financial regulator stated. “The bank is now insolvent.” (link)

Now, as ridiculous as this sounds outside Silicon Valley, the powers that be are concerned about a ‘contagion‘ effect, and openly discussing the need for a taxpayer funded bailout. Blood-boiling doesn’t even begin to describe the sensation.

Now, as ridiculous as this sounds outside Silicon Valley, the powers that be are concerned about a ‘contagion‘ effect, and openly discussing the need for a taxpayer funded bailout. Blood-boiling doesn’t even begin to describe the sensation.

Let the Silicon Valley companies who started with the funds from the bank sell some of their capitalization on the market and finance the bailout themselves. After all, this is one interconnected system of lenders, borrowers and investors. This is not a crisis for the guy making their catered lunches, mowing their lawns, or washing their clothes.

♦The system. A tech guy/gal has an idea or product. Venture Capitalists (VC) organize the funding for the idea/product and go to SVB for money to start the company. The bank funds the startup and takes an equity position in the company. The VC brokers the deal, takes payment and also takes an equity position. The company launches and if successful builds a multi-billion enterprise. If they IPO (most do) then shares of the company are sold and the value of the company rises with the increased stock purchasing.

The shares of the company are capital. The shares can be sold to create funds that can support SVB. If SVB needs funds, let the networked companies sell some of their capital and fund the bank that generated their venture. They do not need outside ‘bailouts’. That’s just the way I look at it.

Listening to some voices saying the guy who mows the lawn of the tech company executive has a responsibility to ‘bailout’ the bank that created the wealth for the tech company executive, is just, well, another absurd example of how corrupt this entire financial system has become. Sorry, but this beyond annoys me.

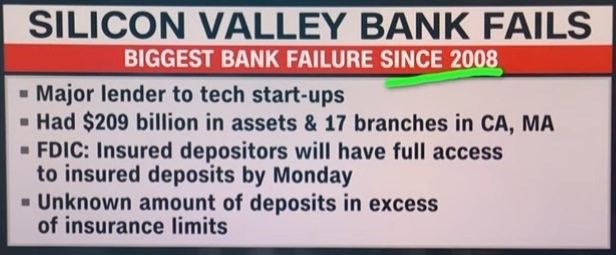

CALIFORNIA – Regulators shuttered SVB Friday and seized its deposits in the largest U.S. banking failure since the 2008 financial crisis and the second-largest ever. The company’s downward spiral began late Wednesday, when it surprised investors with news that it needed to raise $2.25 billion to shore up its balance sheet. What followed was the rapid collapse of a highly-respected bank that had grown alongside its technology clients.

Even now, as the dust begins to settle on the second bank wind-down announced this week, members of the VC community are lamenting the role that other investors played in SVB’s demise.

“This was a hysteria-induced bank run caused by VCs,” Ryan Falvey, a fintech investor at Restive Ventures, told CNBC. “This is going to go down as one of the ultimate cases of an industry cutting its nose off to spite its face.”

The episode is the latest fallout from the Federal Reserve’s actions to stem inflation with its most aggressive rate hiking campaign in four decades. The ramifications could be far-reaching, with concerns that startups may be unable to pay employees in coming days, venture investors may struggle to raise funds, and an already-battered sector could face a deeper malaise.

The roots of SVB’s collapse stem from dislocations spurred by higher rates. As startup clients withdrew deposits to keep their companies afloat in a chilly environment for IPOs and private fundraising, SVB found itself short on capital. It had been forced to sell all of its available-for-sale bonds at a $1.8 billion loss, the bank said late Wednesday.

The sudden need for fresh capital, coming on the heels of the collapse of crypto-focused Silvergate bank, sparked another wave of deposit withdrawals Thursday as VCs instructed their portfolio companies to move funds, according to people with knowledge of the matter. The concern: a bank run at SVB could pose an existential threat to startups who couldn’t tap their deposits. (read more)

.

This is such a brilliant idea, bring a throng of elites together to siphon off money from the classes via a banking system. It has worked over and over again and nobody is ever caught. Absolutely genius! And diabolically evil.

Maybe SVB will give 10% of the bailout money they receive to the big guy.

And what percentage of the ten percent goes to Ukraine?

Or to Palestine OHIO

They probably will kick some of it back

Biden, Obama, Clinton – all bailed out banks! Hmmm, coincidence? More like a pattern!

Reminds me of how Obama would on the outside pretend to be pro occupy wall street while working to crush it behind the scenes. Obama was always the one who spearheaded the mortgage meltdown before he was installed in the WH.

https://www.theguardian.com/commentisfree/2013/jan/23/untouchables-wall-street-prosecutions-obama

It started before Bammy with Clinton and Reno pushing mortgages banks accused of redlining.

It accelerated when they gave banks the green light to give loans to illegal aliens. That got bad enough such that banks were advertising on radio for the loans.

Future Gov Anrew Cuomo was the HUD Secretary working with AG Reno pushing those loans.

I will repeat my story – LOL

back in the day –

My sister worked at this restaurant

an illegal busboy purchased a home

with a government loan

he did not have a down payment

he did not have to verify income

he did not have to prove citizenship

For some of us these were called NINJA loans.

No Income

No job

No assets

I actually knew a couple, CONSERVATIVES by profession, that set up a mortgage company and did exclusively liar loans for illegals, KNOWING THAT THEY WOULD CRASH IF THE ILLEGALS WERE DEPORTED.

Appealing.

Yes, by using the Franks/Dodd Act. Franks is on video, along with the democrat majority, blocking regulation of Fannie and Freddie.

I read that the feds blackmailed the banks into going along with it

When Bernanke called Ken Lewis at BoA, and begged him to buy Merrill. Lewis said “yes” … And then got a look at the REAL BOOKS.

He went to Bernanke, and said, “NO way”, and B. told him that if BoA didn’t go through with it, they’d never do another Merger/Acquisition to try to get the books straightened out.

Let them eat cake.

Or, call SBF.

All well and good until Bank of America fails.

I’m not advocating for a bailout. We are beyond bailouts, the whole system is bankrupt. I’m just saying that arguing over whether bailouts should happen is like standing under the tree and arguing whether to save the bird’s nest – thirty seconds after the lumberjack yelled timber.

back in the day

Bank of America was the bank for illegals

along with Walmart wiring money to Mexico

This is why the elites will melt down. They weren’t smart enough to spread their money around so it will end up biting them in the butt but they are the major financial backers of the DNC. Bailout is the only way out for Joe & Co. After all, if they can’t buy ballots, they can’t win!!

In my opinion, it’s just plain stupid to have a balance at a bank over the FDIC insurance limit. I know there will be business situations where that’s impossible but I wouldn’t have my funds over the FDIC limit at a niche bank with just 17 branches in 2 states.

My grandmother used to say, “don’t put all your eggs in one basket”

For at two decades, SVB played the role of the start-up bank for the cool kids in tech and life sciences, if you were good enough for them (i.e, for the upper-crust VCs). Everyone in the business knew this. There are no innocents in this story. No one deserves a bailout, here.

Yes, and makes it very interesting how quickly a call for a bailout came.

jail time coming?

Just under 4.75 million dollars.

Well we no longer have a legal system or a non-corrupt justice system.

Won’t the proceeds of their stock sales be recoverable? I think that’s how it works in normal bankrupticies.

Debt based business rose in part because of the corporate shield, presuming no criminal activity. It’s not uncommon for principals to siphon the value out of a corporation, bankrupt it and walk away. Lawsuits might recover some of their loot but smart corporate people know how to work the legal system. One can examine a myriad of examples in the dot com crash and later the easy money crash in 2008.

I’m trying to see the big picture of what has caused this. To me, it seems that the base cause of this is the Biden administration energy policy which led to supply-side inflation.

Then the Fed, pretending that inflation was due to demand and not supply costs, raised interest rates to contract the economy.

The raised interest rates led to decrease in the value of US Treasury bonds. The value decrease may also be because of our belligerent foreign policies as foreign countries sell Treasuries like China which has sold around $200 billion of our debt.

Bank investments in Treasuries has reduced the value of investments that back deposits. When large depositors pull out their money in big chunks, the banks don’t have the money to pay all their investors.

Is this what has happened? In other words, is this all a result of Biden’s failed policies on every level.

I think you nailed it. That’s what QE was. For years the government transferred Billions every month to Wall St banks for them to purchase Treasury bonds to prop up the House of Cards that is our financial system. Then the Fed keeps raising interest rates in a recession making the Treasuries worth much less.

Bannon said as much. He said the interest rate rise made their treasury bonds worth less. This at the same time dedollarization is happening BIGLY because the US sanctioned Russian assets and the BRICS alternative is viable and China is pushing the petro yuan in deals with the Saudis and others.

How do I make money betting on the BRICS economies vs the Green New Deal economies?

Invest in hard currency for the coming age: fish hooks, needles, hard liquor, spices, exotic virgins and all the normal valuables of a non-industrial feudal society.

that is a great question

Yes, that’s a good description of what happened.

One analysis ties it to inflation this way:

Startup businesses have a high expense rate in the beginning of development. They go to a VC / angel investor for funding. The VC keeps their money in SVB, SVB makes the loan to the startup. The startup has risk of nonpayment, which is balanced by SVB’s risk tolerance (in the form of interest rate of the loan). The bank rates the loan’s risk of default, and if good, the loan is now an “income stream” to the bank, like a mortgage for property is a liability and an asset. Plus, the startups keep their cash balances in SVB for payroll, ops, etc.

Inflation hits, and the startups burn through a lot more cash than forecast. A lot. The risk of default on the loan is greater than expected. Much greater. And the assets that back some loans, like commercial real estate, are dropping (office demand is way down in a work from home culture). A mark-to-market value of commercial assets shows less value than on paper, similar to 2008 real estate traunches. SVB realizes this, and goes out for a $1.8B bond offering to raise cash, and no one bites. SVB puts out guidance on 3/8.

Now the VCs get spooked, because they too realize this feels like 2008, and they start asking for their cash back. And if a bank says “wait a second, I need to sell this commercial real estate to get your cash” and we all see that is overvalued, we wonder if there’s enough assets to even sell, is my bank underwater? So more people try to get their cash out. And more. And then we have a bank run in Billions USD per hour. And lo and behold, SVB is insolvent.

The collateral damage are all of the other businesses that kept their cash with SVB, which will now be frozen weeks to months. They are scrambling to open accounts at other banks, with IOUs in hand, to get any cash to make payroll (or real chaos emerges). I think this is why JPM swung up, as people realize there’s opportunity there.

Will they indite Trump for SVB’s failing?

Find out who’s taking the IOU’s and run them. If the killer vaccine didn’t motivate people to take to the streets, by God money should. If that fails, stick a fork in it, we’re done and it’s every man for himself. Wild West.

Exactly!

Yes it is. The rising interest rates and a bank that worked with Venture Capital Firms. They received billions in deposits from Equity infusion into Venture Capital Firms. They did not have a large loan base;so they invested in Bonds and Mortgage Backed Securities. They did that so they could earn more in interest than what they were paying out to depositors. Biden’s Oil Policy caused supply side inflation and the Feds raised interest rates. As an example they purchased $100 10 year bonds earning 1.79% . Fed raises interest rates thanks to Biden Policies $100 10 year bonds now earn 3.8%. Many of the bonds they owned saw there value drop by 1/2.

Old Bonds 100 x 1.79= 1.79 New Bonds 47 x 3.8= 1.79….

They would get full value holding for 10 years but the bank run caused them to sell those bonds to pay out depositors taking out there money. Bank Run. Losses were huge and the Bank Run got bigger. The “Incompetent” Democrats are like termites eating at all the structure of our country.

Yes. Very astute.

We have to pray that there are enough common sense members of Congress who won’t cave under the enormous pressure they will be under to fund this bailout. It’s time for McCarthy to continue his promises and Stop funding this crap! No more money to Ukraine. No more money to bailouts. No more money to pay off “friends” of this illegitimate regime!

“enough common sense members of congress”

why do I find that laughable?

I’m a Silicon Valley guy. I just don’t think this is the start of a lot of bank failures to come. The Valley is completely absorbed in the presence or absence of hype. This is a lot of negative hype that spread through the Sand Hill road folks and the CEO network and caused a run. I bet when the dust settles it will be reorganized under some notion of bankruptcy and will be viable in 6 months. I could be completely wrong too – but I think this is not a bellwether on mass bank failures. The Valley is just so different than the rest of the rest of the country’s business sectors.

I may be the fool, but a part of me thinks all the fear and angst in the media and online is part of a coordinated psy-op to pressure Congress to bail out SVB.

True. Also Venture capitalists and their banks have equity in companies that they can use as collateral to raise funds. They do not need a handout from taxpayers.

Still no excuse for a bailout but- most of these startups are not cash flow positive, they are still burning VC money and are not at this time financially viable.

So there’s little hope of equity sales to recover money. The tide went out and a lot of people are swimming naked.

Sucks to be them.

Then why is the word now for TAXPAYER BAILOUT. Where is all this money coming from? Is JOE and his Commies just printing, because they don’t care, if the money is ever paid back . US is a Country in decline soon to implode as long as

the Occupant stays in the White House with OBAMA and his crew running the show. Why is Obama getting Secret Service

protection when he is the Biggest Traitor and Hater of America. I can’t wait until things implode in this country.

The seams are within the breaking point.

Trillions and Trillions… let’s just print some more!

Even if we all stopped paying taxes, I read somewhere here it’s on the order of 5 trillion a year, they’d just add to the debt until U.S. currency no longer had trust nor value. When things go sideways, it’ll happen fast.

The interest rate shock that the Fed has caused affects all banks. The interest rate shock is causing bank bond investments to lose value precipitously. I don’t think the bond valuation problem is isolated to only SVB.

The huge losses in other regional banks this week points to a larger problem.

If banks did not hedge for interest rate rise they are in trouble.

The Fed will have to provide some relief in the form of QE or opening the discount window asap

Check out Chris Whalen on this topic

OR … smaller regional banks will be bought up at fire-sale prices and consolidated under the four existing majors JPMorgan Chase, Citi, Wells, and BofA.

True

That is their ultimate plan. If the global Fascists can get everyone dependent on the 4 banks they control,(and who will all be in sync with whatever they are told to do), then they can push the digital currency scheme they have to force everyone onto this. Then they can control people like China, ( and Trudeau did to anyone who supported the trucker protest.) If you say or do something they don’t like, they turn off your bank account access. You didn’t vote Democrat? You are a Christian? You state there are only 2 genders? You won’t turn in your firearms? You don’t pledge allegiance to the Anti-Christ and get “The Mark of the Beast”? You’re done. We are closer to the end times predicted by the Bible than many realize.

What we are witnessing is one thing after another that cause revolutions.

I’ll be honest; I don’t see many revolutionaries here or elsewhere, non-violent or not. It seems that people are more than willing to twist themselves into pretzels as the tyranny grows and pat themselves on the back for ‘I got this’ and ‘I survived’.

IDK, I guess it’s because my family battled and escaped the Reds and their killing machine during that Revolution that I have a different viewpoint. Tyranny should always be battled until all reasonable avenues are foreclosed. Then one must make the life for a life decision. My grandparents had seven kids at the time so they made the choice to escape and survive. I can respect that. I’m not going anywhere. God will claim me when He’s ready.

Let the scavengers pick over the carcass. No bailouts. That’s how we got into this mess.

“customers withdrew a staggering $42 billion of deposits by the end of Thursday,”

Curious how many had inside information to make withdrawals, leaving everyone else holding the bag.

I’m stuck at, no answer to what led up to that staggering $42 billion withdrew by the end of Thursday. I read this article 2 or 3 times. I was hoping to find out what led up to the staggering $42 billion in withdrawals, in a relatively short span of time it seems.

/Sarc

I read somewhere that Peter Thiel started it by urging his compadres to withdraw funds.

Now why would he do that?

When by all reports the bank was sound?

Is there an Elite VC email distribution list? Given that the SVB CEO, CFO etc took a powder & sold their stocks… Insiders who were paying attention saw this? Who then heard the bank was trying to raise capital? Sounds like an insider employed at the bank IMHO. Who were the first people to withdraw their deposits?

Maybe the answer is for us peasants to pay much closer attention to when the CEO, CFO of their bank are selling all their shares. Would guess that is public information since the info about the SVB Execs has been disclosed on the internet now?

My spidey sense tells me that the announced cause of SVB’s issues–unrealized losses in their portfolio of bonds–is not the only culprit. I strongly suspect some issues in the loan portfolio. My many years in banking and consulting, including working on distressed banks and those under MOUs from regulators, have shown me that it is rare for security portfolio unrealized losses alone to trigger a bank failure. If the loan portfolio has issues (unsurprising given recent trends in tech industry and the many layoffs of tech workers that could affect start-ups or cause the tech “lower tier” rich to draw down investments) then SVB would normally seek to access liquidity via selling the bonds in the portfolio. When both asset classes are troubled, then maneuvering room to ride out issues in either is lessened. Just my 2 cents, though I suspect we haven’t heard the real story behind SVB’s failure.

Great observation ! Thx for sharing

What if Liberybella’s information is correct – that Thiel, knowing the ins and outs of the Silicon Valley high net worth and VC social network, knew exactly who to talk to in order to run the SV network like a herd of sheep into a bank run?

Easy to do with a small closed social network and a bank with only 17 branches?

Yep there is a theory that this is all orchestrated by Thiel and other high net worth individuals to force Jay Powell and the Fed to stop with the tightening and go QE and easy money again

It will be so interesting to see what Jay Powell does on Monday

a small insight into how FTX/Alameda research works:

investors take margin positions (these are very risky loans) to either buy or sell a cryptocurrency.

the usual method is to use bank deposits as collateral.

what this really means is that the bank deposit is staked. In the instance of FTX/AR this means those who took these margin positions were locking their bank accounts as security for a position.

now how the media has described it is that the young prodigy had stolen this money..had shifted the ftx accounts into AR for his own hedge fund (margin trading coupled with “edge” trading combined with some real time machine learning trading bots..this is in fact how most sophisticated hedge funds operate..there is very little human intervention…except for placing initial orders with calls and puts (limits). But the reality is that MOST investors were quite aware that they were signing to have their funds allocated by the young prodigy into that far more risky AR margin trading platform. Not all of them, but most of the really big money…this helps explain why so very few actually have filed any lawsuits! It’s only those that were not aware or were duped into believing their funds ( bank deposit securities) were only being traded on the FTX platform.

my general assumption is that banks like SVB were exposed to massive amounts of margin trading to the FTX/AR fraud. As well as many other high risk crypto schemes. The one things people need to be aware of is that these virtual currency platforms are not regulated. You can easily put your real fiat fungible money into it, but there is no guarantees you can withdrawal. Most of the time you can. However, there are no guarantees that your receive the spot price for that crypto at the current market price. FTX operated as both a trading platform, a fund manager as well as market maker. In this regard, given they have no regulatory law that requires them to have any fiduciary responsibilities to trade AGAINST YOU, they did just that. This is where the Alameda Research aspect of FTX comes into play.

most of the sophisticated venture capitalist in the last 10 years or so, and more specifically the last 5 years have used crypto holdings as capitol for investments. It became the currency of choice.

It is my opinion that SVB failed because most of the accounts have extremely high margin exposure in such financial transactions. They are not just very complex, and subject to incredible volatility but the very basis of most of the wealth is derived from cryptocurrency speculation…

basically dutch tulips.

cabbage patch speculation with an encrypted distributed data base.

Some things will never change wrt to gambling. A sucker is born every 5 seconds…

God Bless America

Nah. You’ll see more later. This was an interest mismatch problem because of rate rises and CEO announced liquidity problems due to depositors needing cash and limiting the bank’s tier 1 capital. Depositors felt their money might be at risk, so pulled it , further reducing tier 1 capital. Voila, insolvency and FDIC takeover to protect insured deposits. It isn’t quite this simple and has some shadiness to it, but it isn’t about margin trading.

Speaking of Alameda, did you know?…

Through his family foundation, Rep. Daniel Goldman, D.-N.Y, a member of the House Oversight Committee, has ties to Arabella Advisors, a Washington, D.C., consulting firm that overlooks the largest dark money network in the country. Arabella Advisors manages the Sixteen Thirty Fund, which has bankrolled the Congressional Integrity Project, a group of liberal operatives working behind the scenes with Democrats in attempts to smother the Biden investigations by Goldman’s GOP colleagues on the Oversight Committee.

https://redstate.com/smoosieq/2023/03/10/dem-rep-dan-goldman-has-an-added-interest-in-sinking-oversight-investigations-into-biden-n714749

The rich people want the little guy to reimburse them for their losses…. Where’s Bernie???

Oh dear.. the techies won’t get paid. Welcome to the party pal! Working class Americans have been struggling since 2021.. Doesn’t feel so good, eh?

Employees going unpaid due to bank insolvency sucks, regardless of company or political persuasion. Those tech startup employees didn’t create the problem – the Fed and this administration did with absurd rate hikes.

Wrong! The majority of those techtards vote leftard. That whole sow and reap thingy. Those techtards also provided the backend facilitation to steal your vote. Let them eat dirt for all I care at this point!

They also provide the tools of weaponizing information to persecute and damage and destroy and sometimes kill us, and have.

Don’t discriminate IMO. They are the enemy. In war we kill plenty of ‘good’ people, both military and civilian. I leave it to God to decide and judge. My job is to arrange the appointment in an equal opportunity manner.

So where were the bailouts for the Mom and Pop operations that were completely destroyed by the lockdowns. You know, the backbones of the American economy? Oh wait, yeah, most of them were conservative so crushing them with forced shutdowns and then slow-rolling any help to them was A-OK with the Biden administration. A Silicon Valley bank? A bank with Zuckerbucks in it? Oh no, this is a Level 5 emergency. Bailouts. NOW! We can’t let that happen before the 24 election cycle. We need those Zuckerbucks flowing into our “critical mass” areas!

Think about it. Taxpayer money bailing out the bank of the Zuckerbucks Biden/DNC mafia. Sadly, the Wall Street Wepublicans will be all over it. Those 11 Senators who came out to defend the J6 Committee/FBI coverup last week will be the first 11 to sign on with their overlord, Chuck Schumer. Oh well, another day in China!

” Its a big club. But you ain’t in it. ” – Carlin

Not a financial geek here but I do remember articles way back…saying Wednesday was a day in finance…often used for balance sheets and decision making… a day banks had very limited hours if open at all.

And some banks when opened again on a Thursday ‘changed names’ due to solvency and take over issues.

There was chatter on this past Weds…..news on late Thursday and bigger news on Friday…giving a whole weekend (minus an hour lost, LOL) to try and right the collision course of this ship.

At the end of the day…this happened under bribem’s watch.

Failing economic policies, collapsing banks, signs of a failed state.

I would say that SVBs announcement regarding under capitalization is sign of policy working. The run on the bank was uninsured depositors reacting to the announcement. The reason for the devaluation in the SVB portfolio is what we should be focusing on here.

Roku announced that they have almost $500M in uninsured deposits in SVB.

Then stated they have another $1.4B in deposits & assets that can fund their business & obligations for at least 12 months. That’s as of today & doesn’t account for profits generated in the coming 12 months.

Roku doesn’t need a bailout & neither does anyone else at SVB.

Everything the Cabal touches turns to shiate

We should NOT make depositors whole over $250k insured limits. These VC’s are the “best and brightest” financial wizards who put their own assets at risk over $250k per FDIC.

But Yellin will do it.

Walk in any Bank and FDIC is noted everywhere!!

The solution is very easy, deposits in a bank over FDIC limits should be noted as unsecured deposits on balance sheets for accounting purposes.

And this FHLB lending crap to distressed banks without significant residential “home” loan exposure has got to stop.

FOLLOW THE MONEY 🙌🏼

Oh wait… you can’t because

IT IS ALL GONE!

Judgement Day is COMING!

California is aways bragging about being the World’s sixth biggest economy

California can bail out their own dam bank!

A criminal is a person with predatory instincts but lacks sufficient capital to form a corporation. (Attribution, H. Scott)

What’s the definition of a banker? See statement above.

I read yesterday that Matt Gaetz said he would do anything and everything to block any taxpayer bailout. I’m counting on him to come through on this. SVB are the people who despise the working class. They’re “Tech” and above us all and love to censor/ban and grift us. I don’t care who lost money in this deal, I know I don’t want to bail out the grifters.

In prior economic crises such as the dot.com bust and the GFC in 2008, and even in 2020, the Fed stepped in and either lowered interest rates, started purchasing assets, or both. What is the difference between then and now? According to the Fed’s quarterly banking report, of December 2022, the nation’s banks have about $620 billion in unrealized losses, due in part to what some of you have identified below: mortgages and US Treasurys that were purchased at 0% interest, are worth a great deal LESS now, at the current rate of interest. The amount of unrealized bank losses now is much greater than in 2008. But now, the Fed, instead of LOWERING INTEREST RATES and/or PURCHASING ASSETS, is INCREASING INTEREST RATES AND SELLING ASSETS. This could cause all the banks in this country to fail. Add to that the fact that 4 banks (Credit Suisse, Barclays, Deutsche Bank and Citigroup have all lost 97% of their value since 2007. (https://wallstreetonparade.com/). Why is the Fed provoking a huge economic crisis in the USA? Who benefits?

Chyna and the WEF. And Soros realizes his dreams: The destruction of the American Republic.

Reinstate Glass-Steagall

Of course they are gonna bail them out. They gotta protect their big-tech buddies.

Regretfully, you’re likely right. However, we can still enact economic warfare on both the financial industry and the government and use this particular time to our advantage.

Else, the tyranny will continue and we will be sweating to buy them bombs, bullets and bioweapons to continue their operations, including killing us.

Matt Gaetz was on Bannon’s Warroom last evening saying the House Republicans will not approve the funds to bail SVB out. I am calling, writing, emailing and posting to my representatives to let them know there will be HELL to pay if they bail SVB out.

The people of Palestine, OH were offered $1,000 to shut up and go away. J6 prisoners are rotting in the DC Gulag. There are still people censored by Big Tech.

I agree with Sundance, the Bastards are more than capable of bailing themselves out. I’ve had enough of this administration funding Ukraine, their administration and their pension plans, not to mention all the war equipment and funds over there.

In fact, I’ve had a bellyfull of this F*U(*&(*$g administration.

Anyone else wonder how much Tesla and SpaceX had in this failed bank?

I know, I know—set up a GoFundMe account!! 🤦🏻♀️

I remember Barney Frank telling us Fannie and Freddie were great investments, until they weren’t … now folks that can’t pay their electric bill should be on the hook to bail out a business that was designed to make risky loans … SICK!

How can this big bank collapse rumor be real if Real President Trump hasn’t even been blamed yet?

Gotta bail out those commiecrat donors, which they all are.

FYI: https://www.zerohedge.com/markets/record-bank-run-drained-quarter-or-42-billion-svbs-deposits-hours-leaving-it-negative-1bn

And this, for granular detail of the impact: https://www.zerohedge.com/markets/expect-mass-layoffs-real-world-impact-svbs-failure

The FDIC has 99 years to pay off any claim. There is no “Federal deposit Insurance!”

It’s all a lie.

Yep. It takes forever and a day to get any money at all.

This is the way they force-nationalize all banks, next on the agenda are credit unions

FSVB !

Let them ear cake

I hate auto write … eat

I had another word in mind but cake works 🙂

Huh?

Whatever happened to bail-ins? Thought that was an option when countries, including USA, passed a law (? 14-ish yrs ago) where bail-ins – not gubmint funded bail-outs) were the option.

I’m confused.

What Will Happen When Banks Go Bust? Bank Runs, Bail-Ins and Systemic Risk

Financial podcasts have been featuring ominous headlines lately along the lines of “Your Bank Can Legally Seize Your Money” and “Banks Can STEAL Your Money?! Here’s How!” The reference is to “bail-ins:” the provision under the 2010 Dodd-Frank Act allowing Systemically Important Financial Institutions (SIFIs, basically the biggest banks) to bail in or expropriate their creditors’ money in the event of insolvency. The problem is that depositors are classed as “creditors.” So how big is the risk to your deposit account? Part I of this two part article will review the bail-in issue. Part II will look at the derivatives risk that could trigger the next global financial crisis.

https://www.unz.com/article/what-will-happen-when-banks-go-bust-bank-runs-bail-ins-and-systemic-risk/

Banks like that will burn very nicely .

Sufficiently motivated we can force them into a bail-in situation and leave the rest to professionals regarding the infrastructure. There are plenty out there who aren’t fans of the financial industry or the Communists.

I’ve already done my part. Let’s just call it my little bucket of sand in the machinery 🙂

While I fully agree that the notion that depositors need to be bailed out to prevent the whole banking system from collapsing is BS (or as you suggest a cynical ploy), the fundamental issue is incompetence of SVB management. They took in hundreds of billions of deposits (literally- they went from something like $20B in deposit pre-COVID to $200Bish in two years). To make some money on those deposits they invested in longer maturity T-bills and what not that were paying very little interest. Now their depositors wanted their deposits back to make payroll and pay their other bills but because interest rates have risen so much when SVB went to sell their T-bills to come up with the money to give back to their depositors they took losses and didn’t have the capital to keep doing it. I’ve worked in financial services for over 30 years and this is just fundamental duration risk incompetence; they teach you NOT to do this in Banking Class 101. Maybe the people in Silicon Valley aren’t as smart as they think they are.

Elon said he might buy it ? I just read…

That’s actually not how venture capital works. VCs raise money in a fund from multiple investors. Startups pitch ideas to VCs. Sometimes VCs decide to invest. The startup sells shares of the newly-formed company to the VC (on more typically a syndicate comprising multiple VCs). The startup will often give the VC a board seat as part of the deal. The startup then deposits the money in a bank, frequently SVB for startups in Silicon Valley. The VC may hold their funds in multiple banks around the world. I know this because I have lived in this world for a time and founded a startup.

“. If they IPO (most do) then shares of the company are sold and the value of the company rises with the increased stock purchasing.”

Most don’t. That’s why they call it venture ( as in starting out without knowing the outcome).

Since most fail, this is the most speculative of capital utilization and banks should be no where near this type of investment. The FDIC should never insure entities which engage in venture capital investing.

“48 hours ago, SVB was a “grade A” Moodys rating. As of tonight, they are insolvent.”

That IS moody!

Maybe they could merge with FTX…

The credit rating agencies always seem to be the last ones to know. IMO, they are worthless.

Over leveraged much? Just like the entire financial industry…