SVB is Silicon Valley Bank, the almost exclusive banking network for Venture Capitalists (VC), tech sector start-ups and tech industry holding accounts. 48 hours ago, SVB was a “grade A” Moodys rating. As of tonight, they are insolvent.

“All told, customers withdrew a staggering $42 billion of deposits by the end of Thursday, according to a California regulatory filing. […] “The precipitous deposit withdrawal has caused the Bank to be incapable of paying its obligations as they come due,” the California financial regulator stated. “The bank is now insolvent.” (link)

Now, as ridiculous as this sounds outside Silicon Valley, the powers that be are concerned about a ‘contagion‘ effect, and openly discussing the need for a taxpayer funded bailout. Blood-boiling doesn’t even begin to describe the sensation.

Now, as ridiculous as this sounds outside Silicon Valley, the powers that be are concerned about a ‘contagion‘ effect, and openly discussing the need for a taxpayer funded bailout. Blood-boiling doesn’t even begin to describe the sensation.

Let the Silicon Valley companies who started with the funds from the bank sell some of their capitalization on the market and finance the bailout themselves. After all, this is one interconnected system of lenders, borrowers and investors. This is not a crisis for the guy making their catered lunches, mowing their lawns, or washing their clothes.

♦The system. A tech guy/gal has an idea or product. Venture Capitalists (VC) organize the funding for the idea/product and go to SVB for money to start the company. The bank funds the startup and takes an equity position in the company. The VC brokers the deal, takes payment and also takes an equity position. The company launches and if successful builds a multi-billion enterprise. If they IPO (most do) then shares of the company are sold and the value of the company rises with the increased stock purchasing.

The shares of the company are capital. The shares can be sold to create funds that can support SVB. If SVB needs funds, let the networked companies sell some of their capital and fund the bank that generated their venture. They do not need outside ‘bailouts’. That’s just the way I look at it.

Listening to some voices saying the guy who mows the lawn of the tech company executive has a responsibility to ‘bailout’ the bank that created the wealth for the tech company executive, is just, well, another absurd example of how corrupt this entire financial system has become. Sorry, but this beyond annoys me.

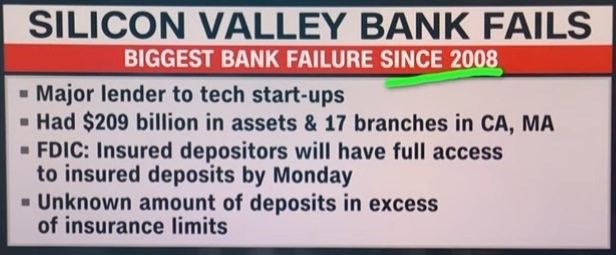

CALIFORNIA – Regulators shuttered SVB Friday and seized its deposits in the largest U.S. banking failure since the 2008 financial crisis and the second-largest ever. The company’s downward spiral began late Wednesday, when it surprised investors with news that it needed to raise $2.25 billion to shore up its balance sheet. What followed was the rapid collapse of a highly-respected bank that had grown alongside its technology clients.

Even now, as the dust begins to settle on the second bank wind-down announced this week, members of the VC community are lamenting the role that other investors played in SVB’s demise.

“This was a hysteria-induced bank run caused by VCs,” Ryan Falvey, a fintech investor at Restive Ventures, told CNBC. “This is going to go down as one of the ultimate cases of an industry cutting its nose off to spite its face.”

The episode is the latest fallout from the Federal Reserve’s actions to stem inflation with its most aggressive rate hiking campaign in four decades. The ramifications could be far-reaching, with concerns that startups may be unable to pay employees in coming days, venture investors may struggle to raise funds, and an already-battered sector could face a deeper malaise.

The roots of SVB’s collapse stem from dislocations spurred by higher rates. As startup clients withdrew deposits to keep their companies afloat in a chilly environment for IPOs and private fundraising, SVB found itself short on capital. It had been forced to sell all of its available-for-sale bonds at a $1.8 billion loss, the bank said late Wednesday.

The sudden need for fresh capital, coming on the heels of the collapse of crypto-focused Silvergate bank, sparked another wave of deposit withdrawals Thursday as VCs instructed their portfolio companies to move funds, according to people with knowledge of the matter. The concern: a bank run at SVB could pose an existential threat to startups who couldn’t tap their deposits. (read more)

.

silicon that is your problem not The taxpayers problems,

Why oh why can’t we discuss the obvious. . .that THE FEDERAL RESERVE Central Bank is the exact cause of all these problems. With artificially low to zero rates fueling these companies/banks “success” and and the rise of Inflation; and then by arbitrarily raising the rates specifically to hurt the economy (destroy wealth) to combat the problem(s) they created.

Jay Powell for PRISON.

Not just Powell but several before him as well, including Mr. Andrea Mitchell (aka, Alan Greenspan) who sought to juice the housing and market back in 2002-05 to help the re-election of G.W. Bush in ’04., thus creating the housing bubble that burst in 2008.

I dont think Greenspan was nearly as much to blame as Robert Rubin, Clinton’s brilliant, nefarious, and conniving Treasury Secretary.

In 1999, he destroyed the wall of protection that had kept Americans safe from Investment Banking predation, the 1933 Glass-Steagall Act.

It only took 7 years for these greedy bastards to completely degrade the whole financial system, bringing on the 2007 crisis, with their Mengele-type bizarre financial experiments, destroying THE ENTIRE WORLD.

And no one went to prison, or learned a lesson from it. We are ruled now by his descendants, fiddling while Rome burns.

This was caused by a vast combination of stupidity by the same people who created the stupidity. Watching Barrons this morning and they suggest buying into the “big banks” vs the regionals due to sell off in past several weeks. The majors are also exposed and mostly due to leverage plays and exposure to illegal naked shorts. Hiw far the contagion reaches is yet to be realized. IMHO

Play with monopoly money, end up with monopoly money. F’ em.

There needs to be accountability…these people violate their fiduciary policies/responsibilities and expect bailouts after their greedy activities fail. Let this bank be an example to the others that engage in the same practices. There will be no tax payer bailouts.

Lack of accountability, along with greed, avarice and mendacity, appears to be a pandemic.

Accountability? We “print” monopoly money…They don’t care. The real people who need to be held accountable are the empty suites that sit in the seats in our Congress and supposedly conduct our business. …. F’em

C’on man if the taxpayers don’t bail this bank out where are all those campaign donations from silicon valley for the demonic rats going to come from? Joe bribeum needeth some cash.

Somehow the fact that SVB had an A rating from Moodys less than 24 hours before being declared insolvent jumps out as telling … telling us something about Moodys.

The Silicon Valley Bank pipeline of free money to

venture capital-backed Tech and Healthcare companies

is over. Many worthless Woke Tech companies in

Silicon Valley will become Homeless Camps.

There are at least 10 other financial institutions in similar situations to SVB and could suffer a similar fate. However, none of them are “to big to fail”!

And no more Taxpayer Subsidies to Elon Mus for the B S Climate Change, Green Energy and EV Hoax… NONE. Stop it.

Put a mask on the doors of SVB, that should stop the “contagion” right? They’re called vultures for a reason..

I’m not knowledgeable about banking, but you distinguished enough between SVB and my regional bank to see that I don’t need to worry about it effecting my bank. I think we are headed towards inevitable financial collapse anyways, but I suspect it will be through hyperinflation and then a sudden “reset” of the currency. Not nationwide bank runs, at least not at first.

Local and regional.banks have rules prohibiting derivatives on their books. Safer.

Venture Capitalist>> Vulture Capitalist! There fixed it for you 🙂The people who really need to be held accountable are the empty suites that sit in the seats in our Congress and supposedly conduct our business. …. F’em

The zombie biotech industry (merely a fancy tool to raise money from suckers) imploded late in 2021, meaning the sharks who run VC recognized none of their magic gene drugs worked, or ever could and no BS story could keep them going in the stock market, pulled the plug. Besides, the $200K+/year employees weren’t showing up for work by diktat of the State.

You can now drive down Torrey Pines road in La Jolla CA and see a very big nest of beautiful, empty buildings for sale or lease – the home of biotech. Just poof, gone. It is so bad that even their trade newsletters have disappeared.

These little pharmas and VC banked at SVB – a merchant bank for the free money class – it took a little over a year for this to hit. The small ripples become waves become tsunamis. The internet has us all believe everything happens in a flash, but it takes time for the weak seeds of free money to wither in the face of an inflationary East Palestine blow up. There is $6 trillion still out there from the govt printing machine, but day by day, it withers and there is less. Print more and you blow up higher. Print less and you collapse.

With a social / cultural backdrop of indoctrinated fools emerging en masse from our equality gardens – name your college or university, high school, middle school, etc – the endgame will be a ferocious destruction of private property. Envy is biblical and we are not far from a chaos unimaginable except in the Bible.

There is no future President, no legislator, no one in dark robes who can stop what has been nurtured for decades. KIpling’s “Gods of the Copybook Headings” will come. They are packing their bags.

Don’t focus on the “look over there” statements. This shows the power of people when they all decide to take $ out on a large scale ,all at once. It caused over leveraged bank to close. The look over there part is about the $20 billion they had I longer dated treasury’s that yielded under 2%. When they had rush of large withdrawals they were FORCED to sell those treasury’s at a 2 billion $ loss. I own 100,000 in treasuries yielding2% that had 1 and 2 year expirations . One has 1 month left to go and the other has 13 months to go. I will wait and get my 100,000 back plus interest. IF I had to sell the longer dated on now I would lose 4%. Not my greatest investment but I am not forced to sell . Have other short term $ at 4%plus. Pray and help others

Which tells you how utterly incompetent the Fed Folks are, not to have foreseen this kind of dislocation resulting from their raising rates so fast.

Idiots.

I heard Matt Gaetz say that he was going to say no to any type of a bailout. Steve Bannon’s show.

The top executives sold their Silicon Valley Bank

stocks weeks before the crash and did not deposit

the money into their Bank accounts. They hid the

money in their homes.

Wow!

Regardless, if a start up gets a loan or sells equity and a condition is that the funds are deposited at SVB, then access to working capital becomes an issue and $250k isn’t going to go far on payday.

SVB went Woke, then went Broke! How ’bout Brandon’s DEI & ESG?

Suspicious me wonders if the bank run on SVB was deliberate in order to (A) receive government bailouts or (B) to engineer government ‘supervision’, in order to gain more control over the bank’s clients. ‘I see you’ve got a nice firm there. Be a shame if we had to call in your loan early, or put a freeze on your cash flow’.

Moody’s was extraordinarily complicit in the 2007 banking collapse, putting AAA ratings on mortgage backed securities that were literally sacks of shit. I’m surprised Moody’s was allowed to stay in business, and Lo!, here they are again.

The rating agencies were the enablers of the securitization vehicles that crashed and burned in 2007-2009 market crash. Both Moody and S&P put investment grade rating on bonds that were collateralized by below investment grade mortgages.

Below investment mortgages defaulted at a 30 percent rate even in good timed. Bundling these junk mortgages together and selling the Debt with rating of BBB to A and higher was nothing short of delusional. However Moody and S&P collected $200,000 and more for each of these vehicles they rated. The problem with SVB looks like a case of not matching asset maturities. Buying long dated assets ( US Treasuries)with funds that have short term maturities (bank deposits) will result in losses if the longer dated assets decline. This appears to be what happened with SVB. Very bad asset management on the part of the Banks management. Also, the lack of Moody to be alert to this situation as it developed speaks for itself (gross failure).

Total ripoff to taxpayers but Fed doesn’t care! This is a perfect storm and Pappy Joe’s budget is the phony remedy in doubling cap gains taxes and making a virtual flat tax for high earners. So who wants to work when they take more money! We’re all getting the shaft!