If you followed my research on banking and the reality of the Russian sanction regime, this report takes on an entirely new dimension. The article is from ZeroHedge, and the topline is not the real story.

ZEROHEDGE – The collapse of three US regional banks – First Republic Bank, Silicon Valley Bank, and Signature Bank – marked some of the largest failures in the banking system since 2008. Central banks contained the “mini-crisis” earlier this year with forced interventions and the mega-merger of Credit Suisse and UBS. Despite the interventions, global banks still axed the most jobs since the global financial crisis.

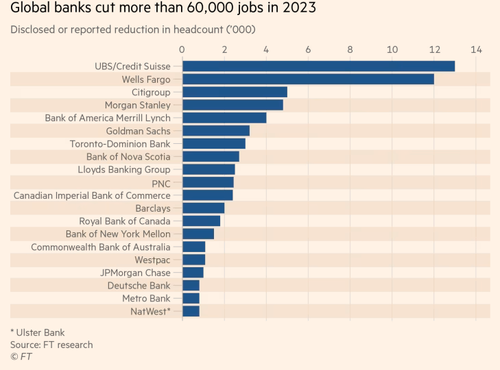

A new report from the Financial Times shows twenty of the world’s largest banks slashed 61,905 jobs in 2023, a move to protect profit margins in a period of high interest rates amid a slump in dealmaking and equity and debt sales. This compared with the 140,000 lost during the GFC of 2007-08. (more)

Look carefully at the graphic labeled “global banks.” What do they all have in common?

These are not global banks, they are all “western banks.” Do you remember a key component of my trip to eastern EU {Password Protected}. That part of my research trip was specifically to understand the contradiction between what the west says about the Russian financial sanctions, and the reality of the irrelevance of those sanctions in Russia.

I didn’t talk, I watched; I listened.

Here’s how it really looks from the outside looking at the USA. The same way the Patriot Act was not designed to stop terrorism but rather to create a domestic surveillance system. So too were the “Russian Sanctions” not designed to sanction Russia, but rather to create the financial control system that will lead to a dollar-based western digital currency.

BRICS+ was creating a non-dollar-based currency alternative for trade. Then comes the western financial sanctions, under the auspices of punishment for the Ukraine conflict. However, think “stopgap.” The sanctions didn’t block Russia, they walled-in the WEST.

The sanctions were not designed to keep Russia out of western banking, they were designed to keep us in. Start thinking from that perspective, and all of the downstream activity, including the aggressive USA govt/banking response to crypto markets, makes total sense.

♦GROUND REPORT – You might ask how I know the Russian sanctions are ineffective – here’s an example. After doing advanced research, I went to three separate banks as a random and innocuous customer. I put my reason in the kiosk at each bank, got my ticket number and sat down to listen to the conversations. When my ticket number came up on the digital board, I just ignored it and sat for hours listening to conversations. No one ever noticed or questioned me – not once.

At every one of the banks, the majority of the customers, at the “new account” desk, were foreign nationals asking about setting up business accounts to trade with Russia. In every bank the conversations were friendly and helpful, with the bank staff telling the customers exactly how to set up their account to accomplish the transactions. No one was saying no; instead, they were explaining how to do it in very helpful detail.

Within Russia, there are now 3rd party brokers with international accounts, an entirely new industry, which creates a layer of transactional capability for the outside company to sell goods into Russia. A Samsung TV travels from South Korea to the destination in the RU with the financial transaction between manufacturer and retailer now passing through the new ‘broker’ intermediary. Essentially, that process is what was happening in the banks for small to medium sized companies.

The USA led “western” sanctions against Russian interests were not designed to keep Russia isolated financially, they were designed to keep USA and Western banking customers walled in. The end goal? To create a dollar based CBDC for western finance.

In order to accomplish that goal, WESTERN govt/banking needs full control. Any alternative (BRICS+ currency/trade) is a threat.

The Western sanctions created a financial wall around the USA, not to keep Russia out, but to keep us in. The Western sanction regime, the financial mechanisms they created and authorized, creates the control gate that leads to a “dollar based” digital currency.

In essence, the Ukraine war response justified a system that creates a digital dollar.

The loss in “western banking” jobs, the downsizing within the banking system, is a feature – not a flaw.

Our daughter, (who is 36) got laid off from her job of 8 years with a bank in late November. She worked in the corporate level, and her entire TEAM got laid off, including her boss. She has come away from a decent severance…so she is okay for now, and looking for her next “gig”. She is fairly well connected and is utilizing many resources her former employer has offered to their laid off staff. This bank had a merger a couple years ago. (BB&T merged with Suntrust Bank, and became “Truist Bank”.) BB&T Bank was a very conservative and tightly run successful and popular bank…and WHY they merged with Suntrust…(which was a TERRIBLE bank), I have no idea. Anyway, I have been noticing that all the “Truist Bank” branches around here, only have 2-3 cars in their parking lots. (Employees???) I wonder if their management wound up being so incredibly STUPID the the entire merger is collapsing.

And, also in our area (Raleigh-Durham) we are seeing literally hundreds of new housing developments, AND apartment buildings. The prices of the homes are astronomical, and the rents from these apartment/townhomes are $$$$$$. We wonder who the hell can afford them? I worry about people these days.

My husband and I are retired, and paid off our house a few years ago…which we are very fortunate to have been able to do. We also own 10+ acres of land near the Virginia border. We had planned on building our “retirement home” up there, but NOW…have decided to stay put because well…as we are getting older, we are finding that it might be in our best interest to be where we have friends, some family, and things that we are familiar with. If we moved up to our land, we would know no one, and have to locate new resources of health care, shopping, etc. Plus…who wants to navigate getting a home built, with the insane prices these days?

Take good care, everyone.

Wave of immigration is providing the demand for new housing. Payments are in excess of affordability–how do refugees afford a monthly house payment at market rates, when the average American doesn’t even earn enough herself to meet the mean?–so the only plausible takeaway is that federal funding is passing through the refugees into housing industry.

This would explain the persistence of housing prices being at or near premium DESPITE a very, very large relative jump in interest rates–double. Ask any mathematician, any real estate agent, any analyst, any assessor…what the new housing prices would be after a doubling of the borrowing rate of interest. They would all say that prices would come down materially, with the lone cynic saying, “all other things held equal” as a caveat. Well, that caveat explains the phenomenon at hand: massive investment in assets as inflation hedges and massive influx of refugees placing demand on entry level and above housing, which shifts demand up all the way up the curve.

i work in an aspect of housing. first off, the feds counterfeit almost 4 trillion per year. that means there is no buisness or aspect of economy that isnt getting counterfeit money directly or indirectly. secondly, my experience is that most of houseing boom is driven by people fleeing the cities to get away from the insanity. prices are still high because there is still demand and not enough supply.

There is plenty of supply! It is being withheld from the market to drive up the cost!

Technically, it’s called “fiat” money, not counterfeit. The difference? You won’t be arrested and imprisoned for spending fiat money. But if you spend counterfeit….well….the feds really don’t like anyone horning in on their scheme.

Just ask George Floyd what happens to you when you pass counterfeit bills. Oh snap! Never mind.

Anyone who moves to FL should have an impact fee on the home they purchase and have to do 100 community hours.

When you are not paying the bill the price doesn’t matter.

The Truist Bank here in Broward County FL appears weird also. The building is huge compared to the 3 people working there. I loved BB&T and was horrified how long it took to get Truist organized for its customers.

We have friends who moved from Kentucky down to the south Alabama area and build a dream home. She, the wife, always says that if he dies first she will sell and move back home. They find being “new’ to the area a bit of a challenge.

My advice, is to stay put and don’t sell your land. Blackrock and their cronies who want to control all housing will be offering the sun, moon, and much more before this squeeze on private property ever ends. They want it all and they want our children and grand-children held hostage to rent.

Wise decision. Seeing the same in San Diego. No sane person would move to California from anywhere unless they are wealthy or working in the tech or medical field.

Crap Weasels

hardley any workers at the local wells fargo in small town pa

Meanwhile: Russia to begin supplying pork to China

https://www.rt.com/business/589800-russia-pork-exports-china/

So, here we go with the downfall of the US Currency system and subsequently the downfall of the US Dollar as the value setting currency for the entire world. Adam Smith would not have been able to describe such a debacle. Get ready for the end of the greatest economy in the history of the world. This will change every mind in America, but too late to make any difference. They will crater our economy just to stay in power. No wonder the rich are all building bomb safe bunkers beside their mansions. The economy will be going underground in more ways than one.

I’m watching houses being built and very large apartment buildings going up everywhere here in central Ohio. I’m also seeing a massive influx of illegals with very nice cars and lots of groceries at the store. We citizens are having a hard time keeping up yet the new arrivals seem to living well. It’s my gut feeling that the housing is owned by the same people planning to blackmail anyone who won’t sign up for their digital ID and currency with no food or housing.

Close, very close.

Who are these new Russian brokers?”. So, I hold what are now “worthless Russian securities “, in a U.S. brokerage account. From listening to his experience at a foreign bank, Imshould be able to set up a foreign account and transfer these shares to it, so I receive the dividends I’ve been missing..due to sanctions….. Shouldn’t that work?

What banks will take US accounts that still do business with Russia? I need such an account for my now worthless Russian securities, so I can still collect dividends

If you were these people trying to start a digital economy and you had invested a lot of money, time and political capital into it and your start up system began to fail what would you do? Crash the economy completely? Start a major war? Commit suicide? All three?

One thing you would not want to happen is have a populist like Trump elected President who could expose all of your misdeeds to the world.

Seems like it might be a good time to put funds into an international account in a BRICS country?

I don’t often comment. I hope that SUNDANCE sees this. DAVID WEBB came out with a documentary and pdf book titled “The Great Taking.” that explains that all the mechanisms are in place to crash the system and take all assets.

The documentary and pdf book are both available at:

https://thegreattaking.com/

Quote from page 41 of the book:

Essentially all securities “owned” by the public in custodial accounts, pension plans and investment funds are now encumbered as collateral underpinning the derivatives complex, which is so large—an order of magnitude greater than the entire global economy—that there is not enough of anything in the world to back it. The illusion of col- lateral backing is facilitated by a daisy chain of hypothecation and re-hypothecation in which the same underlying client collateral is re- used many times over by a series of secured creditors. And so it is these creditors, who understand this system, who have demanded even more access to client assets as collateral.

It is now assured that in the implosion of “The Everything Bubble”, collateral will be swept up on a vast scale. The plumbing to do this is in place. Legal certainty has been established that the collateral can be taken immediately and without judicial review, by entities described in court documents as “the protected class.” Even sophisticated profes- sional investors, who were assured that their securities are “segregated”, will not be protected.

Telly, I just posted upthread to Sundance requesting he do an analysis of this. I am reading the book now. I don’t understand all the financial mumbo-jumbo but I do understand the bottom line. As we have been told by the traitors in power “you will own nothing and you will be happy.”

If they get universal CBDC they can do away with bank branches entirely. Everything is digital not physical so no tellers, no vaults, no armored cars, no security guards, no branch managers. Everything is in the AI-powered computer system so no loan officers, no auditors, no HR staff and no back office except for a few sysadmins. The computer will do only what it is programmed to do, no human decision making to second-guess or feel pangs of conscience.

CTH – “In order to accomplish that goal, WESTERN govt/banking needs full control. Any alternative (BRICS+ currency/trade) is a threat.

The Western sanctions created a financial wall around the USA, not to keep Russia out, but to keep us in. The Western sanction regime, the financial mechanisms they created and authorized, creates the control gate that leads to a “dollar based” digital currency.

In essence, the Ukraine war response justified a system that creates a digital dollar.

The loss in “western banking” jobs, the downsizing within the banking system, is a feature – not a flaw.”

They must have a war to have “dollar based digital currency”. In short, they must remove “Any alternative (BRICS+ currency/trade) because it’s a threat”.

Plus, the Bible seems to say they will get it. And we will see 666.

They could joint together under the threat of war, but right now it seems unlikely.

I have not found any articles or news about how Americans with a fair amount of money invested in CDs are beaming at the interest they are being paid on CDs and MM funds.

That is a game changer and unless someone points it out for what it is, a bribe, then many of us will think the economy is great.

I predict come tax time, that most of us earning high interest will be TAXED beyond the pale. Also, once the election is over, look for CD rates to take a downward turn.

CDs paid almost 0% interest for a decade and Biden and Yellen et. al. figured out how to trick us into thinking that higher yields would shrink the money supply and falsely lead to a decrease in inflation. What say those who know more than I do?

Sundance – have you seen the article on Dr. Mercola’s webiste “The Great Taking”? I am reading the book about it now. I think the CTH would benefit from your analysis of this.