As if carrying Homeowners insurance in California and Florida wasn’t already subject to ridiculous increases in premiums, things are about to get a lot worse.

Effective with the July 1st notification, Reinsurance rates, these are companies who insure the insurance companies, are telling their clients there will be up to a 50% increase in cost for underwriting catastrophic coverage. Perhaps claims in the past few years have been higher; however, I suspect the issue amid the reinsurers is partly connected to the issue that surrounds banks and bond rates.

Back when interest rates were near zero, banks and reinsurers likely scooped up lots of Treasuries and bonds. As the Federal Reserve hikes rates those bonds have declined in value. When interest rates rise, newly issued bonds start paying higher returns to investors, which makes the older bonds with lower rates less attractive/valuable. The result is that most banks, and I suspect big reinsurance houses, have some amount of unrealized losses on their books.

Back when interest rates were near zero, banks and reinsurers likely scooped up lots of Treasuries and bonds. As the Federal Reserve hikes rates those bonds have declined in value. When interest rates rise, newly issued bonds start paying higher returns to investors, which makes the older bonds with lower rates less attractive/valuable. The result is that most banks, and I suspect big reinsurance houses, have some amount of unrealized losses on their books.

Whatever the reason, the big reinsurance companies are now telling the insurance carriers their catastrophe rates are going up as high as 50%. Those insurance companies will then pass those rate hikes to the individual policy holders for commercial buildings, residential homes, cars, RV’s etc. Bottom line, homeowner insurance rates are about to go up again with policy renewals, especially in Florida and California.

LONDON, July 3 (Reuters) – U.S. property catastrophe reinsurance rates rose by as much as 50% at a key July 1 renewal date, broker Gallagher Re said in a report on Monday, with states such as California and Florida increasingly hit by wildfires and hurricanes.

Reinsurers insure insurance companies, and have been raising rates in recent years because of steepening losses, which industry players put down in part to the impact of climate change. Higher reinsurance rates can affect the premiums which insurers charge to their customers.

U.S. reinsurance rates for policies which previously faced claims for natural catastrophes rose 30-50%, Gallagher Re said.

Reinsurance rates for similar policies in Florida rose 30-40%, the broker added.

Some insurance firms have pulled out because of the risk of heavy losses. State Farm said in May it would stop selling new insurance policies to homeowners in California.

In Florida, “all the major carriers (insurers) left and so you ended up with this market which is populated by a large number of very small, very thinly capitalised insurers which is exactly what you don’t want,” James Vickers, chairman international, reinsurance, at Gallagher Re told Reuters. (keep reading)

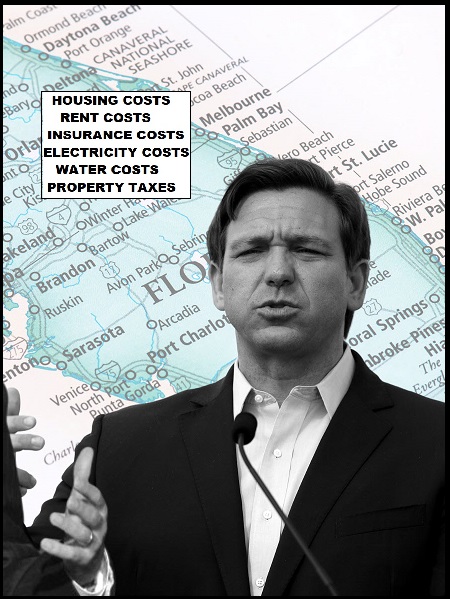

In Florida specifically, homeowners insurance costs have now generally risen higher than the mortgage payment for a middle-class family. This is not sustainable.

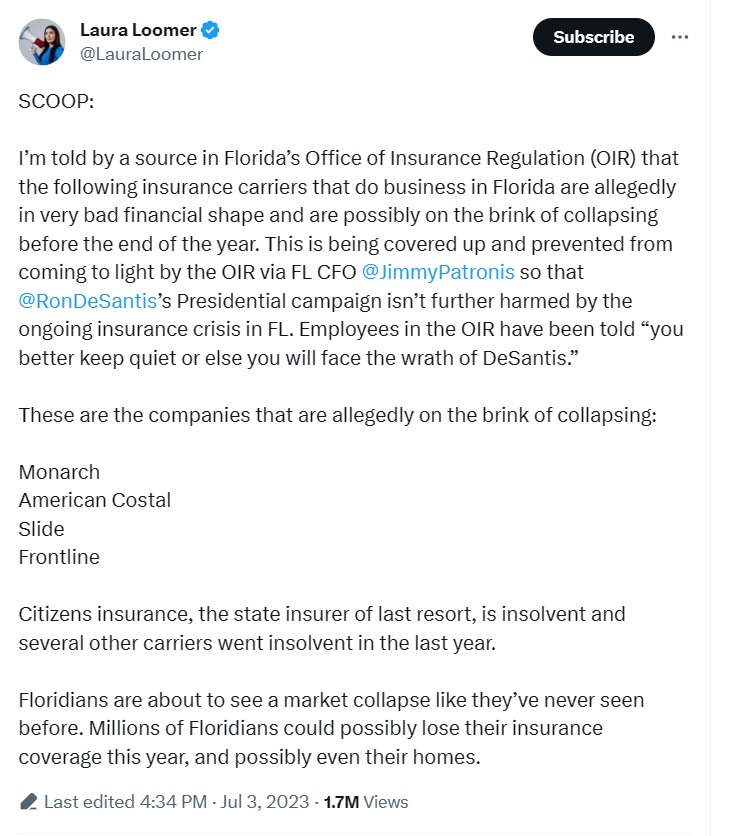

SCOOP:

I’m told by a source in Florida’s Office of Insurance Regulation (OIR) that the following insurance carriers that do business in Florida are allegedly in very bad financial shape and are possibly on the brink of collapsing before the end of the year. This is being covered…

— Laura Loomer (@LauraLoomer) July 3, 2023

If Laura says so, I believe it.

And you would be….? Reading at the wrong site?

Take large bucket.

Fill with water.

Insert head.

You are learning something here whether you like it or not!

Richard Cranium a dos!

Sundance?

FU

Pithy and to the point.

Random, I am assuming that you did not randomly insert Sundance into your post. Thus, I am wondering how you came to include Sundance in your not so random thinking.

I’m NOT a writer, so I always have problems expressing my thoughts on paper, but I’ll take a stab at it!

IMO, what Random is saying is that the 1st 4 individuals are known universally as “being on the side of Global Warming (Climate Change) & they are always “preaching such ideas”! Sundance on the other hand, is excellent at “explaining what they do” in a language that the Common Man can comprehend!

I hope this helps!

BTW: No matter where you choose to live in the World currently, the same problems are going to be there eventually!

NOTHING is going to change, until we get rid of this “Climate Change BS”, that’s being used to control people… almost since the “Dawn of Time”!

Love Loomer…..during the Obama years she was one of the few intrepid journalists telling the truth.

Why are you here? Slow day at HEADQUARTERS???

hyper inflation is coming

the zombie banksters are looking for bail ins

now is a good time, while Credit Card King Joe Bidan is the (s)elected occupant

and while Ron DeSanctis is looking for campaign “donations” aka bribes

Later this year and early next year we’re going to see a bomb go off in the economy that will make 1929 and 2008 seem like the good ole days.

Commercial real estate is the ticking time bomb that will start the domino effect of economic collapse. Because of Covid, occupancy rates in commercial buildings, etc. in metropolitan areas is dramatically down–in some cities 50% or more. With reduced occupancy are reduced lease payments which building and property owners are dependent on for income to pay the mortgages for that property.

If those entities who are leasing office / building space cannot pay and default on the lease–or simply decide not to renew a lease–building owners suffer loss of income and then can’t pay mortgages to the banks on the property. So then, properties start being dumped on already weakened banks.

Voila` !

The walls come crumbling down.

But never fear, the Deep State never lets a crisis go to waste.

And some big economist said the other day that this work from home is here to stay. My son and daughter in law are still working from home.

My son was working from home, before, during and after covid. He set himself up nicely when being a contractor prevented him from buying in DC area, with a second child on the way, he moved his family back to Florida. He has been able to work deals to keep his job in DC and work in Florida with periodic trips North. All the grandparents EXCEPT my ex/2nd wife are DELIGHTED with this arrangement. All of his mother-in-laws daughters are local and raising great children. They have “adopted” me. Spending the fourth with them. God works in strange ways and mice and men are mostly irrelevant.

Those buildings used to be a staple of insurance company investing.

I’ve been saying this for months. I just went through this crisis within our own HOA in FL and there is going to be a huge crisis by next year here in FL. Many people will not be able to afford to live in the free state of Florida. There is no indication the Governor tried to acknowledge and attempt to fix this huge problem we have here.

It’s looking more and more like all Ron DeSantis was doing was putting on a performance so that he could replace Donald Trump on the ballot. I don’t think it’s gonna work for him.

I already made money shorting the reinsurers. They’re getting crushed with life insurance claims. Younger people pay less for life insurance because they don’t usually die so much.

Ed Dowd has been spreading the message around. You are smart to listen.

you sure about that? *died Suddenlies?*

Dies suddenly applies to the youth! See how the jab works??? Soon the injection of Pb starts!

Yes, I read the original report from the insurance industry when they were expressing great concern, this was before Ed Doud came out with His wake up call. Ed Doud reported on this same crisis. Very easy to look up the info.

No they’re not. Young people don’t buy individual life insurance. Only about 40 percent of the entire population has an individual life policy. Mortality rates for life insurance have not changed so far. I’ll let you know if they do.

What about the group policies through the employers?

Not sure I understand the question. Are you asking about claims or rates? Either way not seeing any changes so far. Group plans are typically term life and very low death benefit. Usually 10,000 to 25,000 on average. Group life rates have naturally increased over time as the group of individuals ages. Have not seen any changes on those rates either,

If I understand Ed Dowd correctly, he initially noticed a change in death rates among the working age insureds with group life through their employers.

===================

You prompted me to look at the US all cause mortality numbers for 2021 and 2022.

https://www.cdc.gov/mmwr/volumes/72/wr/mm7218a3.htm

Deaths were down overall for 2022 v 2021.

Deaths in absolute numbers and rates calculated in deaths / 100,000 in the age groups covering newborn through 14 y/o were up.

Deaths were down in all other age groups in 2022 v 2021.

When I say mortality rates I’m talking about the price of life insurance. Rate tables that insurance companies use have not changed in the market place. Mortality changes all the time. I have not seen an increase in the price of life insurance in the industry. I hope you can understand the difference. That’s all I’m saying. Just because mortality changes (short term) doesn’t mean there is a direct impact on mortality rates.

I do understand. Thanks for the clarification.

Exactly right. He’s a failure.

Ron’s “back door deals” with the insurance companies?? Try this on for size–the lege of La openly voted to GIVE insurance companies 45 million just to come here and write. The 45 million isn’t for roads, bridges, water trmnt plants; it’s for the POCKETS of insurance companies to come here and write, many of whom will go belly up in 2 years.

Geez. So disgusting.

And our present insurance commissioner thankfully will not be running again.

No problem then. The people who gamble that way and LOSE … will simply fall back on the Federal Govt. Make no mistake … disaster relief is coming to a neighborhood near you soon. Your fellow taxpayers will pick up your losses … because “we are a compassionate people” … and “because the wealthiest nation on the planet can afford to take care of disaster victims” … Right?

Federal Disaster INSURANCE will become like Obamakkare medical INSURANCE. … all those people who couldn’t (or wouldn’t) “afford” to buy health insurance … simply didn’t. And when they had a catastrophic crisis … they simply hid their assets and took the FREE government healthcare.

As I’m vacationing in FL currently, I can agree. I’ve seen non-stop litigation billboards all up and down the gulf coast touting everything from trucker cases and motorcycle cases as well as “billions recovered for storm damage”. Lawyers and insurance companies are bottom feeders. Period.

Just did a renewal electric bikes and electric scooters Burned down so many houses last year that they are now excluded from homeowner’s policies

You have a fire like that, you’re on your own (aka “naked”)

Every where I look I see a new neighbor w an electric bike, boy oh boy are they gonna be pissed about spending $5k on a new ebike then reading their new homeowners policy

According to a flyer put out by the FDNY, the ebike batteries should be taken inside to be charged. They should be plugged directly into a wall outlet, not on a surge protector strip, not with an extension cord.

Don’t go cheap when purchasing an ebike. The less expensive ebikes tend to use less expensive batteries and electronics.

I bought an ebike for my granddaughter’s 18th birthday / Christmas. My daughter bought one for herself. One of their ebikes has a Samsung battery and the other has a Bosch.

My granddaughter does not have a driver’s license yet. To add her to the auto insurance policy would cost an additional $3,000/year for bare bones coverage where they live. Not only will she be able to live at home and commute the mile or so to campus when she starts college this fall, she will be able to find a place to park.

These ebikes will pay for themselves rather quickly.

I like my 15 year old Raleigh. Pump air in the tires, off you go. Cost me $200, about $75 more than my 1973 Schwinn Sports Tourer. Neither caught on fire, but my brother did fall off the Seawall in Galveston with his girlfriend once….

Used it in college, back across UT Austin to Apartment in less than 10 minutes.

I just “inquired” about “renters” insurance,, almost Un Obtainium, being EAST of highway 17 in a doublewide home..

The problem is the batteries. They have a nasty habit of giving you all their energy all at once (as in catch fire and explode). The technology is not ready yet for widespread commercial deployment except for small batteries. Electric motor technology is improving but still need more development, i.e. room temperature superconductors). But the motors do not have the safety issues the batteries do. Batteries do not perform well at low temperatures below freezing and high temperatures, 100 F or higher. They tend to lose their charges. Also large lithium batteries are incredibly expense and the spent ones are a hazardous waste disposal issue.

My guess is the most practical next step will be a hybrid similar to diesel electric trains. A high efficiency gasoline or diesel engine running a generator which recharges a large capacitor which in turn sends power to multiple electric motors each powering a wheel with power distribution based on traction and demand.

Car insurance up over 100% in 2 years. No violations.

Home insurance last year 30%, don’t know about this year.

FEMA (surge) insurance up 20-30% last year, won’t know until October.

Goodness me!

All the best, but those are staggering increases.

That coupled with both inflation and interest rate hikes will obviously crash the economy.

Folks in the know ( not me) have been talking about Oct/Nov of this year as being a financial sh*tshow.

Who knows, but if we incurred increases like that we would have to revisit how we go about our retirement years.

Cheers!

Insurance on our condo in IL went from $480 to $980 (no claims)

Car is now $2200. 2 years ago was $1500 (no claims and same cars)

Yet the media and majority of idiot population continue to say Bidenflation is a myth while they kneel at the throne of king Pickster

CUT THE CORD

My car insurance renews every 6 months. Last July is was $586, in January it was $678 and the renewed I just paid was $760. No accidents and drive 2,700 miles in the past year. Shopping around hasn’t helped like it did in the past.

House insurance renews in late September. It went from $1325 to $1600 last year. It’s just about double what I paid in 2019.

I am so glad to know I am not the only one who drives less than 3000 miles a year!

What would $20 buy you under Trump, versus today. What has changed?

I just enrolled in USAA’s SafePilot auto program, which is an app downloaded to ones phone. While driving it tracks phone handling, hand-held calling, hands-free calling and harsh breaking. They have 14 days of a learning period where one can see any infractions on a trip. Thus far I haven’t had any and the learning timeframe has ended. Now it’s counts and a good report can lower one’s auto insurance policy.

I’m retired and don’t drive far and not even everyday. Travel is mostly on surface roads at low speed. This program should be of benefit for me although many who have different driving habits might not be interested in it.

I just would not want to consent to be monitored like that

If I weren’t retired I wouldn’t do it, but I don’t do any of the things they’re monitoring for safer driving so I’ll take the discount. I’m a safe driver and deserve topayless.

So go ahead, meekly accept the Orwellian control.

What could possibly go wrong?

They will soon find SOMETHING you are doing to justify preventing you from free movement.

While probably re-selling the data collected. Just keep in mind the tradeoffs. There are always trade offs in the digital data mine.

You’re monitored without your consent I assure you.

They do that not to drop your rate, you give them real-time access to everything you do in your car, speed, where you go, how long, etc – data brokers can buy that data….in an ‘anonymized’ form of course, even CIA/FBI/DOJ admitted they ate buying your data protected by the 4th Amendment. And they can raise your rate – you drive slower than local traffic, or whatever – then you have to fight it.

Thank you for the information.

I would think today’s newer models with all the high tech already have this information available for the taking. Would that be true? I really don’t know b/c my car is a 20 yo Honda Accord, highly maintained, looks like new inside (literally) and I’m keeping it, but it doesn’t have all the high-tech stuff and I don’t want it.

I go the speed limit as traffic allows on surface roads. In metro Atlanta that’s about 30. I go the speed limit on the interstate but not over it. I monitor myself. I get a ton of discounts from USAA as a 33 yr member for both auto & home. We’ll see what happens.

Fraudulent Elections have Consequences

Catastrophic consequences.

My auto insurance just went up $120 from six months ago–no tickets, no claims, no nothing.

Well, don’t forget that inflation drives insurance rates up because it’s driving up the replacement cost of the things being insured, even if everything else stays the same.

The insurance rates in Florida way exceeds inflation.

They rose here because of back room deals between DeSantis and the insurance industry.

And Surfside falling down. Ronnie told them to pay that claim quickly (PR for his campaign) even though it was the HOA that voted not to do the maintenance required to keep the building standing. They all thought they would die first of natural causes before they would have to pay the huge maintenance costs required to keep the building viable. Now, all HOAs have to adhere to more rigorous standards, especially buildings 3 stories and more and within a couple miles of the coastline, which also raises the HOA fees for everybody.

My old car rolled into another in ice, $3500 for repairs, all plastic, no air bag deployment. The Costs are what drive rates…to repair an ‘average’ $50,000 car….

Own car & house outright, am modifying car to drop collision if rates are too dear.

In Fl it no longer matters price wise so I carry full coverage.

Damn. I just sent this to my son in East TX. New homeowner with almost new wife and toddler. Glad his mortgage isn’t here in FL, as much as we’d like to have them closer. Fortunately we own our house, we couldn’t afford the insurance.

Just received my Homeowner’s Insurance Policy from Farmer’s for 2023, $3,882.00. 2022 was $1,821.00. Have never filed a claim.

I’m sure they will say it is due to Climate Change and all of the fires in California. Proper fire prevention and enforcing the law against those large companies who cause fires with regulation/law non-compliance would prevent this kind of thing, in addition to proper Forest Management and controlled burning.

My insurance agent says there is no end in site. He is also being told behind the closed door this is an effort by the CA Insurance Commissioner to cater to Insurance Companies for losses during Covid and adjust for Inflation.

Why haven’t local DA’s, the State AG, and Lawyers included in settlements with the utilities, who are the real culprits, pay the insurance increases for all effected by their negligence?

Better yet, some enterprising lawyer needs to start a class action to recover those increases from the bad guys (Electric Utilities in CA).

California hasn’t managed its forests right in 50 years. We stopped logging, stopped cattle grazing, then add in the Sierra Club… they actually sued to REMOVE LOGGING ROADS .. which also serve as access roads during fires. Gone. Then Newsom released a bunch of prisoners early during Covid, and many were trained fire fighters. You can’t make this stuff up.

Dr. Bill Wattenburg on KGO radio, a former Apollo scientist and Lawrence Livermore Labs researcher, talked about this for decades on Open Line to the West Coast. Neither he nor Jerry Brown made it a priority.

Tell him that you want to see the industry “climate change” causality studies from year to year, for the last five years, with actual actuarial calculations.

Watch their eyes get like deer in the headlines. Accept nothing less.

Ins companies will tell you that the increase is due to all kinds of things, than their other losses on bad investments (like USD Bonds) which have gone in the crapper.

And your higher premiums are NOT due to an increase in costs, but to make up for OTHER bad investments that went bad. I think that’s inherently dishonest.

If the insurance company loses money on bonds, but the insurance company needs to balance their returns somehow, they take money out of rate increases on YOUR POLICY, when it’s not related to insurance losses at all.

Get your state reps & senators, and state Insurance Commissioners involved. Make their lives miserable.

Is not going to work. Insurers, reinsurers were all doing business as they normally did with treasuries and other interest bearing instruments, when Biden’s policies pushed inflation to the moon and then, Powell raised interest rates making the treasuries they were holding worth less because the newer treasuries pay much higher interest rates. The insurers were hit from both ends and were squished in the middle. Most have no other option than to pass it on to consumers. Are insurers greedy? Yes. Do I detest them? Yes. But this actually is not entirely their fault, plus they are paying out on the mRNA deaths of young people who were in group policies and mandated into the jabs. Could insurers have handled this better, in many cases yes but it would not have been enough to change the outcome. Government and employers intervened in ways that were detrimental to the entire population.

You’re correct that this is not entirely their fault. But they, like all the other big players with direct phone numbers for their pet law-makers, chose to not speak up and resist the jabs, the lockdowns and the coup.

They chose which side they will be on. Every store, company, industry and government unit that went along is complicit in the harms caused.

Fair enough. The insane, incompetent, immature Biden people have NO IDEA of the ripple effects of their poor economic policies… 1st the banks (which never recovered from 2008), now the insurance companies.

Yes, they are evil and conniving, but I’ve been watching this crap from lefty politicians for 40+ years, and they are all so immature and ideologically bent that they can’t put together 2 and 2.

I’m going to my home in Mexico, where the corruption is similar, nobody has insurance, there are no hurricanes, and houses don’t burn. It can’t be worse than here.

California is so mismanaged that your Governor is trying to move out to DC, and a lot of it is his fault. So many of the wealthy have moved out that your tax revenues are down 25%

State Farm, Nationwide, Travelers and Allstate put a moratorium on writing auto and home in California. Nationwide is non renewing single policy holders of any kind. The next step for them if things don’t get better will be withdrawing from the state. That was the beginning of the end for Florida in 1990s. When insurance companies start these types of restrictions it effects everyone in that pool of business.

You are probably subsidizing free insurance for 2 illegal families, that are renting homes in your neighborhood with $3000/ month rent ‘vouchers’ CA is giving them.

When ideologues in govt mandate green energy, the R&D dollars have to come from somewhere. Maintenance $ get diverted, and the mandates continue to get steeper, so the maintenance never gets done as it needs to.

Climate change is the reason. The fact that agencies are mandating unrealistic targets for something that doesn’t exist is immaterial to them. But it is all in the name of climate change.

If you want a picture of the Florida disaster watch this guy, https://www.youtube.com/@MichaelBordenaro/videos

HOA’s will be going up by 300%, unless your building gets bought up by speculators, in which case you will be kicked out.

Live in a trailer park? Bye bye. Speculators are buying them up.

The Florida state-sponsored insurance agency (last resort for many people) will go under if another Cat 3 hurricane hits this year. After your insurance is gone your mortgage company will sign you up for a policy and then take your house when you can’t afford it.

Realtors are telling retirees and fixed-income people not to move to Florida.

Florida will be just like California: no middle class allowed.

Yeah, Alabama seems to be the destination for some leaving Florida.

When I had a condo, the HOA covered the roof.

One thing I learned about insurance with the first homeowners policy I bought 44 years ago. Seems obvious but most people don’t think about it.

You are insuring the structure(s) on the property and liability, NOT the land. So when someone pipes up that your property value increased 100% over the last year, for example, that 100% is not the cost of replacing the structure on the property.

Why does it matter? An example: I have a barn that I insure for $280,000 (as of last year) with replacement cost insurance. That same barn, if I built it this year, would probably cost $320,000 with materials and labor costs.

Should my insurance rise 100% ? Hell no!

You can always contest the value that an insurance company puts on your property. They use a percentage of increase for labor and materials in whatever territory you are in. If you have an agent ask them to do a replacement cost estimator. Many times I have lowered values for my clients doing this simple thing.

Yucatan, Mexico. Si….

… because of CLIMATE CHANGE?? WRF??!!

Am I missing something?

How about…

– historic inflation?

– commercial real estate issues?

– lockdowns?

– etc.?

I’m no expert… but blaming it on… CLIMATE CHANGE???

The left blames EVERYTHING on climate change . Sad part is there are people out there stupid enough to believe it.

One has as much chance of changing climate as I have of landing on the Moon!

That’s never been the goal of the left’s global warming/nuclear winter/ climate change hoax. Climate affects every nation in the world–hence the perfect weapon to control…er…the world.

You’re only angry because climate change is making it hot where you live.

We have a running joke in our family. When something goes wrong, we just chime in with… CLIMATE CHANGE caused it….

Anyone know where I can find more specific information – like rate hikes by state ? I would really like to know how much is due to losses from natural disasters and how much is due to vandalism/ theft/ general lawlessness.

Illinois is completely out of control in terms of car theft and vandalism, and Northern Illinois was always the car theft lead of the nation.

I actually saw a guy stealing a car once, filmed him and had an exciting time practicing my evasive maneuvers on city streets while he chased after me. It got a little sporting, but I had the presence of mind to maneuver to block a street so traffic piled up quickly in both directions. That gave me an audience (people cared then) big enough to keep him from attacking me — til I could scoot away. I was on the phone with 911 all the time and high tailed it to a well lit parking lot with lots of traffic where I met the Chicago cops. After hearing my statement and reviewing my (lawyer) credentials and photos of the theft in action they had one comment: “Lady, go back to Wisconsin.” I did. Listening more to a little voice in the back of my head which said “you know you are getting too old for this,” while he was out of his car coming after me with the tire iron. It’s exponentially worse now.

The cause of this is that the Reinsurers invested their money in bonds, as in US government bonds. As inflation raised bond rates, their bonds with lower rates are worth much less and cannot be sold for near what they paid for them. What I cannot understand is why national insurance companies even need reinsurers. I remember the days when major cities had skyscrapers named after insurance companies and a lot of that was rented out to other businesses.

They do that to lay off ‘unlimited risk’. Like a total clean-swept slab is all that is left. I’ll insure $200,000 re-construction costs, but over that (say another $100k) someone else can by the risk that it won’t be just a roof & half the house. Re-Insurer will get 50% of premium for that . For some reason, Reinsurer says I’ll do it for 150% of last years premium. Would guess they ‘lost $ at the track last year’, or their investments (value of 0.5% 30 year US Treasuries) got killed – down 30%. As such the pool of insurance Capital is lower, so existing companies raise rates or pull back. High rates will attract new entrants – over a few years.

Hi Bob, the liability or potential risk for a single skyscraper can easily wipe out an insurance company which is why the insurance company will seek a reinsurer with deep, deep pockets to offset the risk. So, the reinsurer offers to insure the insurance company.

A very real example was the day the two towers came down. The unanticipated exposure nearly took out a top global reinsurer.

In today’s world with additional exposure everywhere, reinsurers will look to offset their risk by retroceding which is working with additional reinsurers (reinsurer partnering idea). In the example of the skyscrapers, the first reinsurer will determine which tranche(s) of liability they want to keep and those they want to bring in other reinsurer(s). Very complex at times, but no one reinsurer wants to assume full liability for complicated exposures — one catastrophic event can wipe out the best of the best balance sheets.

Is there any chance someone who can access twitter can find the list of insurance companies that Laura Loomer’s tweet references (the last image in the post, it says READ MORE… and then to click on it still takes to the blank twitter page). If these insurers are in bad financial shape, it would be helpful to know who these insurers, re-insurers are).

Thanks

Thank you, Sundance.

Laura Loomer is a gem, a warrior and one brave American Patriot.

Prayers up for her.

🙏 🙏 🙏

And she was debanked for speaking out.

Same as some in Canada over the peaceful anti-jab protests. That was an eye opener!! It was a long time conspiracy theory… until it became reality and made a lot of people rethink a lot of things.

Like Brits are now doing to Nigel Farage.

NEWSFLASH: It has NOTHING to do with climate change !!!!!!!!!!!!!

These increases will drive more people to drive illegally w/out insurance. Adding to the mass of uninsured drivers on the roads already. Driving up the rates becomes an endless cycle of putting up a down payment and defaulting on the monthly payment. The insured will pay the price when they are involved in an accident with the uninsured driving up the rates again.

Not to mention all the illegals driving around, drunk and uninsured.

Yep, and all the NGO lawyers getting them organized and in-country are getting enriched at the same time, likely with taxpayer money. Interesting racket, isn’t it?

At some point I hope people will stop trying to contort themselves into pretzels for these scum and go kinetic. We are many and they are few and their enforcers have yet to be tested in full on combat. They’re used to citizens sucking their cock of ‘muh authoritah!’. The British were pretty cocky too. Well, it’s Independence Day. 🙂

France today…

Not in FL. They suspend your license if you drop insurance on a vehicle and do not turn in the tag.

Yes I know people do illegal things but with license plate readers, putting an unregistered tag on your car will get you pulled over pretty quickly.

Ultimately, while one can roll the dice on home insurance, rolling the dice on car insurance and uninsured/under insured motorists riders is NOT recommended. One accident can lead to disablement requiring much more lifelong expense than one can imagine. Especially now with so many jabbed people with spike proteins eating through their brains and hearts while driving. Its the same issue the pilots are having driving after putting the mandated mRNA into their veins. Add all the new illegals driving without licenses, without reading English signs, etc. It’s a recipe for disaster.

In my state, no insurance NO tag…. of course the illegals just borrow a tag from a friend 🙄

Adding insult to injury, NY has some sort of a new mandate that will randomly add $5 to our auto premium per year, unless we opt out by a written form. Just pure robbery.

My insurance agent had no idea where the money was going to, except the insurance company has to send the money to the NY Sate Board of Insurance Companies.

Ugh.

Here in LI NY My homeowners went from 1400 to 2500…

It took 10 years to go from 1050 to 1400

Oh, wow.

There IS no such thing as “insurance.”

What it is, is no more than a guaranteed loan, because, should you file a claim, you WILL pay it all back, plus.

Legalized usury.

Plus, blaming “climate change” lets the NEO/WEF

cover for the demise of another safeguard of personal liberty: private property, whose value goes away in the event of an uninsured catastrophe.

Their great desire… Take away all we own, and mock us as we stand shocked, and then we lose it, and then, it’s given to illegals.

For free.

They changed it from Global Warming to Climate Change for a reason. But I’ll go on a rant if I go on….🤬🤬🤬

That’s the truth!

Legalized extortion.

I live in TX and Allstate jumped my rates substantially on my homeowners. They did lose $1.3 billion in 2022 though, according to their annual report.

Lots of unverified numbers being written . About the be statement about HOA fees in Fl . being raised by 300% ,I say BS. Have gone up by 10% in each of last 2 years and am not happy with that. My NFIP (flood insurance) did go from 1400 to 1700 this year on 300,000 coverage. That is without cost of property which is another 300,000.My homeowners and hurricane insurance is $2000, through citizens. Show me where it is insolvent?Just renewed all policies through 07/2024.

Am not happy with these increases . In my case will keep me working at 70 for 18 more months and maybe adious to fl. to the gulf coast of al. or maybe just rent. Pray and help otbers

Fl certainly had a problem with under capitalized insurers in the past. They collect premiums and a major hurricane comes and they go byebye. Years ago a retired politician opened POPE insurance co. Collected millions In premiums ,hurricane came and Mr. Pope declared bankruptcy.

Hope they tightened regulations since then. Been in fl 25 years in Anna Maria island and sadly moved to Naples 3 years ago.ive your best life , pray, and help others.

There is another angle to this. It is not just Florida and California. States that have Gulf of Mexico frontage, as well as many of your Atlantic states have already had insurance go up more than double. This in part to offset the accumulated in the last major hurricane to hit Florida last year but there is another sinister plan afoot.

With only a hand full of companies such as Lincoln, Lloyd’s and AIG writing it within certain distances from a major body of water they can name their price. Hence the 50% to 75% in some cases. While some have the luxury to self insure if they chose because they outright own the home , those that hold a mortgage are required to have some fairly serious coverage.

You go from paying 12g one year to being told your only choice is a 24g policy you cannot afford, you better hope it sells quick. I think it is about prime real estate consolidation. Limiting home ownership from another angle, while forcing the middle class to a renters pool or to move to another market.

You even have a modest 2300 square foot home setting 30 feet above sea level but are within 400 yards of the gulf, you are looking at a Buick a year in Hurricane, wind and flood pool coverage.

“Limiting home ownership from another angle, while forcing the middle class to a renters pool or to move to another market.”

You will own nothing and be happy. Klaus Schwab, WEF, Biden, Trudeau, EU leaders, etc

There are a number of issues at work in the reinsurance and insurance market.

Last year, the property-casualty (P/C) industry in the U.S. caused 74% of worldwide insured losses, mostly due to Hurricane Ian. You might remember that storm as the worst Category 5 hurricane to hit Florida since 2018 in terms of wind speed and the deadliest since 1935. The P/C industry had a net underwriting loss (meaning they lost money on their core risk transfer function called underwriting) of around $27 billion because the industry suffered around $140 billion in insured losses in 2022. This is after multiple years of rate hikes beginning around 2017 or so and continuing every year since. I am grouping together personal lines and commercial lines. Most of you just know about your auto and homeowners business. The industry really hasn’t made money for several years. You probably remember State Farm and Allstate pulling out of California recently. There are economic and political reasons for that.

There are a host of other issues, too. The National Flood Insurance Program (NFIP) rolled out a new risk rating called 2.0 which brought rates closer to being actuarially sound (meaning they are closer to charging a rate that will be breakeven to making a small profit) but the rates are facing political pushback almost everywhere. The quick rise in interest rates also has an effect on investment income because most P/C insurance companies are half to 2/3rds invested in bonds. And for those insurers invested in the stock market, they usually take dividends over capital appreciation, so the upside and downside is limited because they need liquidity to pay claims quickly, hence the focus on bonds and blue chip stocks.

Most of the premiums that people pay are highly regulated by the politicians in the various state insurance departments. While that probably keeps rates more stable, it cannot take into account any year-over-year changes in losses and loss adjustment expenses. In other words, Florida suffered massive losses due to Hurricane Ian last year, but your individual homeowners rates probably didn’t go up more than 25% from last year–even though the losses suffered in Florida alone accounted for a large portion of worldwide total losses. You can thank the politicians for saving you money.

But here is the issue: that loss money is going to have to come from somewhere. In the short term, it comes from an insurance company’s policyholder’s surplus–the accumulated money set aside when the insurer guesses wrong on losses. Whether it is the State of Florida floating bonds to backstop reinsurance coverage for insurers, or premium increases, or investment income increases via a booming stock/bond market, someone, somewhere has to pay the claims and keep the insurer viable as a going concern. Watch the policy count at Citizens Insurance, the Florida insurer of last resort. P/C insurers industry surplus dropped last year.

Citizens is going to get a whole lot bigger sooner than you know. Yes, there are thinly capitalized insurers that are on the brink. Remember, reinsurers don’t have to reinsure insurance companies. They can walk away from a bad deal. Insurance companies are stuck. They can’t raise rates fast enough to cover their losses even over a few short years and reinsurers have already lost enough money in Florida. A number of reinsurance programs in Florida are not filled out, meaning the insurance company is keeping even more risk but insurers have no choice. If the private reinsurance market won’t provide the capital at the reinsurance rates deemed adequate, and the State can only provide some capital via “reinsurance” bonds, then insurers are stuck. Just remember those glorious 15 years of no hurricanes in Florida…yeah, might’ve been nice to create a nest egg over those years and not tax the “profits” of insurance companies so they could smooth out a rough patch like last year.

Just a few thoughts to provide some context for my CTH friends.

“ In other words, Florida suffered massive losses due to Hurricane Ian last year, but your individual homeowners rates probably didn’t go up more than 25% from last year”

100% not true.

My family has owned in a 1236 FL condo complex for decades. In the last 6-9 months owners were posting their 2022 & 2023 rate increases. 50-75% increases were the norm, if they weren’t outright cancelled.

My 166 condo cluster policy was not renewed. The Board was forced to go with Citizens (last resort insurer) and the cost is over $1MM, which is 5xs what we paid last year.

You are confusing commercial insurance for the condo property in total with the individual owners of condos (usually on an HO-6 policy form) and what I said was homeowners insurance. Those are three difference policies. I only commented on homeowners insurance (HO-1,2 or 3) because those rates are heavily regulated by insurance departments in all states. Whenever a large insurer wants to increase rates, the insurance department must approve the rate increase. When an insurance company cannot get the rate increase, they restrict coverages, restrict writing geographic areas, and eventually will stop writing new business, possibly pulling out of the state altogether.

I didn’t comment on commercial property rates because those have been increasing substantially for several years. Many states have a file and use system that doesn’t require approval from the insurance department. The reason is that business insurance buyers are considered more sophisticated than personal/individual insurance buyers, thus the rates and forms are less regulated for business insurance.

It depends on who the insurer is, of course, too. When the private business insurance market walks away from a policy, it is because the policy is underpriced for the risk of loss characteristics or actual losses. The fact your condo business was “forced” to go to the insurer of last resort (Citizens) demonstrates my exact point. You confused business insurance (multifamily condo business package policy) with homeowners insurance. Different insurance companies will ask for different rates based on their actual experience. The same is true for individual policyholders…if you’ve had a loss, your rates will go up faster than if you didn’t have a loss. My 25% is a general, over the whole market, observation, not based on one person’s individual experience on a non-homeowners product like commercial business insurance.

I wasn’t exclusively focused on Florida, either. That insurance market has been ripe for reform for a long time. Thankfully, some modest legal reforms were passed but it will take time to understand the full effect of the laws.

The insurance department doesn’t like to approve large rate increases due to the political position that puts an insurance commissioner who probably wants to be re-elected or go onto “greater” things.

An industry publication from March of this year, which highlights the overall rate increases and individual rate increases.

https://www.insurancejournal.com/news/southeast/2023/03/31/714518.htm

I realize my Cluster HOA has commercial insurance (we got canceled) and the new policy was over $!M, 5xs the prior one.

Individual homeowners (condos) in the complex are either being canceled or increased 50-75%.

No matter how you skin this cat no increases in FL are a mere 25% this year and my complex being 1236 units is a good cross-section of what’s occurring and innumerable owners took to our private facebook page and gave their policy costs.

Your theory might be working for you in PA, but not in FL. Not buying it since I’ve seen the numbers from 100s.

And everyone in FL is well aware of flood insurance which is the least of many owners’ worries since FL coastal condos are usually muti-stories and most above ground level aren’t going to have rising water ot least they are will to take that risk.

Your comment focused on FL. “In other words, Florida suffered massive losses due to Hurricane Ian last year, but your individual homeowners rates probably didn’t go up more than 25% from last year”

I was addressing the inaccuracy of that statement.

Actually, according to an article from Kin Insurance who quotes the Insurance Information Institute (a nonprofit focused on the insurance industry) and published in January 2023, the average rate increase in Florida was 30%. I said probably 25%, which was a guess, and apparently a pretty good guess. Here are the links: https://www.kin.com/blog/florida-homeowners-insurance-rates-increasing/ and https://www.iii.org/

I think part of not understanding the average rate increase for the entire state of Florida is the bias of one’s own personal experience. I don’t know where your condo is located, but based upon what you describe, I suspect it is in a coastal county and closer to the coast. There is a lot of Florida, and population of Florida, that is not on the coast and while those homes of inner Florida may have had rate increases, they were not nearly as extreme as the coasts faced. It would not surprise me if some personal lines rate increases on the coast are 50% to 100%, but keep in mind, your state government approved the rates before the insurance company could use them.

One must also factor in that your individual insurance premium may have been on the lower end of the average rate and now is on the higher end of what the insurance company can charge. Insurance underwriters can give and take credits in the rating process at each renewal, depending upon the insurance company’s appetite for your kind of risk/structure/location. An insurance company could write a risk 5 years ago that they wouldn’t touch today for many reasons, one being the ability to get an adequate rate for the exposure and the concentration of business in a geographic area.

So, actually, my statement was not so inaccurate as to be false, especially given I am just giving some broad thoughts and advice on the market in general. 25% vs. 30% is pretty darn close.

It’s a crap shoot for insurers. FL insured’s premiums don’t cover all hurricane damage. Neither does so AZ insured premiums cover all AZ fires, etc.

Pick your poison. There are catastrophic weather conditions anywhere in the country and it seems to be getting worse. Have you noticed the many tornadoes lately? Hardly mentioned in the news but I follow some storm chasers.

Insurers are keeping up. Can’t keep their coffers up to snuff. I don’t imagine it has to do with any of the catastrophic economic issues the Biden Admin is responsible for.

Thank you for the thorough and informative exclamation

Your welcome. I too appreciate when others answer my questions.

I have been in the P&C insurance business for 30 years and appreciate Repubican PA’s assessment of the current crisis. Spot on! Additionally, what made Hurricane Ian so devastating compared to other CAT 4 or 5 hurricanes in the past was how slow Ian moved across Florida. It’s why some buildings and bridge structures that had stood the test of time through multiple hurricanes in the past, finally succumbed and were destroyed by Ian. Ian just moved so slowly that it kept pounding an area for an extended time frame before slowly moving northward.

Since Reinsurers are “excess” property insurers over the underlying carrier like a State Farm, Allstate and others, typically, with normal hurricanes, the Reinsurers aren’t called upon to actually pay out huge losses. The underlying carriers, through their own surplus pay those claims. With Ian, Reinsurers had to come in as excess and pay out huge losses based on their position as excess over those underlying carriers. It has thrown the entire industry into turmoil.

Please understand, as bad as the P&C rates are in Florida, California and other coastal gulf coast states, this huge rate action is being felt all over the country, especially in eastern coastal states all the way to New York. Trying to find adequate wind insurance limits all the way up the coast on properties where the underlying insurance carrier excludes wind is drying up. Most of my clients are in Virginia and North Carolina and are now seeing property rate increases in the 300% range on commercial buildings as well. We are also seeing “self insurance” for the first time where you cannot find enough reinsurance out there available to fully insure for wind storm events. Whereas you can fully insure to 100% replacement cost for perils such as fire, lightning, water damage, etc, you may be only able to afford to buy 10% of full replacement cost for a hurricane wind event. If a CAT 4 or 5 hits certain coastal areas with properties this summer, many owners will be in trouble trying to rebuild for lack of insurance. What is being absorbed in Florida is drying up availability in other states north. It is the new normal until these reinsurers can have a few seasons to recover their losses.

You know I get tired of hearing about insurance company losses.

They collect money for years and years, invest and make dividends and capital gains, funds growing exponentially.

Then when a catastrophe comes and they have to pay out and those funds drop below to a level below what was projected or expected, they all shout losses and want bailouts thru one means or another.

And then the pay of these guys. I personally know of an executive a partnership that was bought out from a larger carrier. Was already making hundred of thousands of dollars a year.

After the buyout, he and the other partners were all receiving 7-8 digit payouts.

Just on that one agency with 6-7 partners, had their payouts been half of what they were, there would have been enough money, in principal alone, to have rebuilt completely destroyed homes at the average home price of somewhere between 50-70 homes.

As far as I am concerned, ‘professionals’ like this and similar (think health care administrators and university and school system administrators), & unnecessary government workers are way way over compensated.

And there are thousands of them.

After all, all they’re doing is selling a promissory note and investing the money.

As far as I’m concerned, insurance companies are nothing more than filthy prostituting thieves that the public is forced to pay, or have your property seized, your health care denied or go to jail (auto).

Screw them!

Set up a co-op with your neighbors to repair your houses if damaged. Ben Franklin did that. Contribute skilled labor, cash, lumber, shingles, wiring, appliances or whatever you want to cover. Adjust rates based on size of homes, Concrete vs wood, etc etc.

Screw those insurance bastards…

Ha! Yes, that’s exactly how the insurance business started in the US. In 1752, Ben Franklin and his firefighter friends started The Philadelphia Contributionship to so just that. Generally, those are called mutual insurance companies.

https://1752.com/about-us/history/

And then some Philadelphians were upset that The Contributionship voted in 1781 to stop insuring homes with shade trees. Policyholders would have to cut down their trees or lose coverage, so they formed their own insurer called The Mutual Assurance Company for Insuring Houses from Loss by Fire and used a firemark with a green tree symbol. Eventually, the company became known as The Green Tree Perpetual Assurance Society.

Across the country, there are hundreds of little mutual insurance companies that insure small farms and homes and mobile homes. These are great little companies located in many rural–and a few urban–areas. Some of these insurance companies maintain their own favored construction crew with construction supplies to fix policyholder’s damages. Very hometown.

Our ‘beach house’ south of Houston, in Sargent TX, 1 mile off the Gulf on Caney Creek, was insured by Slovonik Mutual out of Bay City TX. Our friends, the Smaisrtla’s, hooked us up with the Czech community that emigrated there in the 1800s.

History of Indianola, TX is interesting, near Victoria TX. Was the biggest port next to Galveston in the 1800s. Most lumber to build San Antonio came through there. Two hurricanes wiped it out, but JP Morgan rebuilt it. Was competing with Port of Galveston – Vanderbilt. JP Morgan was dying when the third leveled it, Jay Gould did not rebuild – nothing left of it – merchants moved up to Victoria – safer than the coast. History repeats.

Vanderbilt had Galveston, New Orleans, Mobile?; JP Morgan had Indianola, Morgan City LA, funding the consortium to dredge the Houston Ship Channel – Morgan’s cut.

Thank you. What you wrote in so little space adds flesh to the occasional news stories about the marine archeology projects at Indianola that went beyond the LaSalle connections.

Most of my comments are in regards to property-casualty insurance/reinsurance and not any other kind of insurance (i.e. life/health.)

MGAs, insurance agencies, and insurance brokerages don’t pay losses. They are the distribution force for the actual risk taking entity: the insurance company. The kinds of companies it sounds like you’re describing are typically paid some kind of commission by the insurance company for “producing” the insurance business on behalf of the insurance company. And, yes, some of those guys do quite well. That doesn’t mean the CEOs of large, publicly traded property-casualty insurance companies don’t make a lot of money; they do. Chubb’s CEO makes over $22M per year as the boss at the largest publicly traded P&C company. Most insurance company CEOs don’t make that kind of money, especially small mutual insurers–their compensation is usually more modest.

When a distribution force (as it appears you describe) is purchased from an existing set of owners, it is not uncommon for the owners to get 150% to 300% of the annual revenue as a purchase price. It depends on many things including the profitability of the brokerage, the type of business, the renewal rate, and the growth of the company. There are more factors, but yes, I can see a small $3M revenue agency be sold for $5M if the business is solid. The key here is that the person most insurance buyers deal with most of the time at policy renewal is an agent or a broker at one of these insurance company distribution partners (i.e. agent or broker.) There are direct writer insurers that have their own “agency” force but those, too, are captive agents and are paid on a commission-like formula.

When the insurance company pays a loss, it first comes out of their current cash flow of earned premiums, then short term investment income/investments, and then reinsurance. Most years, the insurance company can pay these losses without resorting to selling bonds and stocks that make up their policyholders’ surplus. In a bad year, the insurer can be forced to sell their longer term investment assets (think bonds for the most part, and some stocks) that may contain unrealized gains and losses. Imagine being an insurer having to sell their 3.5% coupon rate 10 year bonds to raise cash right now…they are taking a huge loss at the sale on the value of those bonds to pay current claims which reduces their policyholders’ surplus and may put the company in a more precarious financial position.

Then, the insurance company has to ask reinsurers for loss indemnity according to their reinsurance agreements. Hopefully, the reinsurance program has been structured properly, has been filled out completely, and the reinsurers are still in business. And if the insurance company gets into the back pocket of the reinsurers from this loss, good luck at renewal on January 1st. If the insurer has been a long time customer, has been a good partner, and buys a prudent amount of reinsurance, then in the most recent reinsurance market, the capacity should be available but at a much higher cost (think 50% – 150% increase in reinsurance costs.)

So, the insurance company now has an underwriting loss, investment losses, increased reinsurance costs, increased operational expenses to handle the rush of claims all at once, and actual paid and incurred losses and loss adjustment expenses for properties and homes damaged by a storm. And Florida has had a few of their insurers go out of business with more on the way. Generally, and in most states, it is pretty unusual for an insurance company to go out of business without some occurrence of fraud. Florida is different because of the spike in loss costs that make doing business as a newer insurance company very difficult (Louisiana is having issues, too.)

I am not familiar with government “bailing out” property-casualty insurance companies. There are two federal programs for flood and terrorism, and there are programs in LA and FL to provide a backstop in the absence of reinsurance capacity and to pay individuals’ claims of failed insurers. Those failed insurers have been liquidated because their liabilities (i.e. claims) are greater than their assets; the company is not “bailed out” but put out of business by the state and the Guarantee association pays as much of the outstanding claims as they can. There are some states with clawback statutes for senior execs of these failed insurers. All coastal states have some kind of Wind Plan and all states have FAIR Plans and Guarantee Associations. These are designed to protect and help policyholders. Insurance is a highly regulated business.

Let’s make sure we understand the difference between the risk taking entity-the insurance company-and the distribution force and their different roles in the insurance business.

You have my wholehearted agreement on administrators and bureaucrats in general, wherever they are.

There was a harbor club I heard about. After a nasty storm took out the place, members were lucky that they had good numbers and some influential people that had skin in the game. The group got everything paid out to put their place back and then some. Instead of going with what was there, and banking the overage for a rainy day, self insuring (they had been told they would never get that coverage again and what they would get was going to be outrageous and sub par), the decision makers built back big, big, big with no thought for a downturn.

The guy telling the story said, this particular situation was a glaring factor in shinning the light on everything around them.

The recomendation to overbuild, taking on a unnecessary bank note and refusing to practically self insure, while optioning excessively priced coverage that might not pay? Yep that was the bankers, insurance agents and lawyers at the table. To add insult to injury, each year they voted to wave their dues and doc fees, less food and beverage because their bad decisions needed to be compensated.

The situation is being run well and everything is in the black with room to spare, no problem with some offset. Being run into the ground? I got problems paying for that.

Then you had a manager off the rails being paid a fortune, while skimming. Can’t they fire him I asked? Uh no, manger knows where everyone’s secrets are. Yep, a leasure club being run on blackmail. What about members meetings? Why not go in with a show of force? Well, like so many other things the members just shrug and do not think it is important enough to attend and vote, or do not want to spend their energy fighting that battle. They just want a nice place to have a drink and some sub par food. Be able to dock their boat and bbq by a pool now and again.

After a few liability issues caused serious cash flow problems, members started exiting to other choices in large numbers. Before anyone could blink, the establishment of this operation found themselves in a battle for their overbuilt playground, paid for by other peoples money. They had to let people in they would never have considered worthy in the past to help pay for it. Their reality has changed in every way. Worse, the peoples they relied on to carry the financial responsibility have moved far beyond a club of this nature, being important enough to spend money on any more. Even those that have it to spend.

I did ask what the numbers were during the heyday. A waiting list 40 deep with 600. Now it is not even 1/6th that and they cant give away membership.

Hope springs eternal.

I guess my point is, this is another micro situation that is exactly what is going on across industry lines both in the private and government sector. It simplified a lot of issues for the person telling about the situation. Hopefully there is a lot more of this out there.

My family has a condo in Fl at a very large complex, over 1200 units broken into about 17 clusters. Our cluster is the largest, 166 condos. In February the Board received a Notice of Non-Renewal from our insurer. The Board was forced to go with Citizens and it cost over $1mm! It’s 5xs more that what we were paying. It’s a very time consuming process to try and get another commercial insurer, if even possible. In the meantime the monthly fees increased by $400+/month. The other clusters are holding their breath.

Where’s Gov DeSantis now??

He disappeared from fl.

Always, always not enough in the kitty after collecting for years and years to pay out on claims regardless of the premiums charged. They KNOW these claims are coming, we buy insurance precisely for them to prepare for them.

This is the issue right here. I can’t help but think that the bad Biden economic issues from energy to our proxy war from zero interest rates…has anything to do with insurers having bad investment risks.

Insurance companies seem to get less and less profitable as time wears on. Operational costs eat into the coverage promised to their insureds. Damage settlements are tough and payouts are eroded by exclusions, multiple deductions, depreciated value, etc,. etc. etc.

Perhaps too much $ spent on geckos and emus and fat Flo?

Don’t forget Mayhem

CA here. Last year’s insurance was $4,000. This year it is $10,000. Plenty of folks we know have simply been cancelled. Hard to find any coverage at all in some areas, in which case one must enroll in the CA Fair Plan which is run by the state. State Insurance Commissioner does nothing to help homeowners.

“This is not sustainable”.

Careful. Or you’ll get a gubbmint solution.

In addition to homes, Massive increases to insure a boat in Florida as well, along with other coastal states. Folks with boats not in hurricane zones have also seen big increases, which are no doubt in part due to the issues you raise.

But they are also due to the way risk mitigation works. I have some working knowledge of the marine insurance industry. The reality is that Great Lakes and other inland boaters are subsidizing the boaters in hurricane zones. Great Lakes boaters are paying much higher rates than they otherwise would (or have ever paid in the past as a % of total insurance revenues) which allows insurance companies to keep hurricane zone coverage lower than it otherwise would be.

I know nothing about the home insurance industry. I don’t own a house. But I have little doubt that homeowners insurance works the same way.

The #1 reason boats especially on trailers are so expensive to insure? Because their owners leave them in marinas and next to their houses as a hurricane approaches, instead of taking them inland or putting them in a garage.

I owned a 44’ sailboat for 18 years. Every time a hurricane or nor’easter threatened, I ran it up a creek. Literally. There are many such places in FL along the intercoastal waterway, nice mud-lined relatively narrow passages, and drop 2 or 3 anchors, remove the sails and all else on deck, etc.

After the winds passed, I’d retrieve it unscathed from wind and waves, while marinas would be devastated with boats piled up on docks and each other.

Just rank stupidity.

So, you will own nothing and be happy commences!

You will own nothing and pay for Black Rocks insurance premiums 🙂

I was in the thick of Hurricane Ian. Made out much better than most and thank God for it.

Condo damage assessment was $12,000. Car insurance up 25%. House insurance up 250%.

Not sure I will be able to stay for the long haul.

ron! the Radioactive Reptilian’s actions tell me that his only problem with Florida is it is full of Floridians. We are being squeezed out. Normals might spend this Fourth looking for new digs behind strip malls and Big Box Stores, the good spots go quick in Tent City.

Like the farmers in Netherlands…multinationals have got plans. Seriously, I think the NYers and Kalifornians are driving up demand/home prices. Here in TX too. Then they get the Shock of property tax and/or Insurance rates, and ACTUAL hurricanes, not just on the Weather Channel.

I think of how you would invest with a WEF or BlackRock in this situation – how would THEY make money with these high & going higher costs of property and operating expenses? Yet alone, where are the workers gonna live? I just don’t see Blackrock/Chinese owning everything. As Will Rogers said, ‘I am concerned about the return OF my money, let alone a Return on It’

Also didn’t Sundance have a piece, house assets up by the Fed to get 3% mortgage rates, so the homes BlackRock, etc own they want to cash out and move to the next grift. Freddie & Fannie put on a surcharge for High credit score borrowers to subsidize low ones (aka Illegals) – to boost their creditworthiness to buy these inflated homes/condos.

Oh Governor, Where art thou ?

It is certainly the case the issuers of health insurance don’t make money on the insurance but rather on the investments of the funds they hold. It stands to reason that this would hold for other forms of insurance.

The GOPe can go sod themselves. Forever.

Woke up to read this. We are in Sarasota today taking a weeklong trip around FL looking for an investment property (vrbo) to buy. Asked the Lord to guide us before we left. Can’t help thinking the Lord sent this post my way this morning. Happy 4th to all you Treepers. Keep the faith!

The VRBO market is drying up. Too many units came on to market in past two years and the travelers searching for property have dropped in numbers. Here in Phoenix many, many properties are not booked for the high season. Usually most Condo’s book a year out in advance for winter.

The real estate short term rental chatter is very concerned especially if one has a mortgage and HOA to maintain – not profitable.

“This is being covered up and prevented from

coming to light by the OIR via FL CFO @JimmyPatronis so that

@RonDeSantis’s Presidential campaign isn’t further harmed by the

ongoing insurance crisis in FL. Employees in the OIR have been told “you

better keep quiet or else you will face the wrath of DeSantis.””

Then the DeSantis political aspirations of becoming president are more important than the financial survivability of the population of the entire state of Florida.

This guy does not deserve to become president.

The Bible says something that can apply to this, and the simple logic is irrefutable even if one does not believe the Bible.

Luke 16:10:

“10 He that is faithful in that which is least is faithful also in much: and he that is unjust in the least is unjust also in much.”

If he will not take care of the people of Florida, the state for which he is governor, why should we think he will take care of the people of the entire country?

Riots, vacant office buildings, shopping malls and many commercial strips are over 50% vacant in many urban areas. Banking, commercial real estate and insurance killed themselves when they bought into the pandemic. Walgreens are closing in most urban locales; theft and arson. In their effort to unhorse Trump they all destroyed themselves. Wall St is/was no different that Bernie Madoff.

Karma is a bitch.

try being more informed

Keep in mind:

The biden regime has been driving inflation higher by intent, since day one in January 2021.

Driving this looming insurance cost inflation, and all manner of other economic juggernauts pushing the US down.

Just the US Bloc, though. Not China, Russia, or other BRICS+. Curious, no?

Wake up people.

Bless your heart!

Texas too.

Flood insurance 2020 $400, 2023 $800.

Home owners insurance 2022 $2,500, 2023 $4,000

From my independent insurance agent..

“Like I said rates have increased with all carriers, State Auto being one of the worst. They are trying to get out of Harris County.”

Perhaps a discussion of the history of ‘insurance’ in America would be instructive. There’s one central entity that all of this surrounds.

Lawyers.

We seem to get it with regard to ‘Lawfare’ against PDJT and other patriots but seem to miss the lawfare conducted daily against all of us, plus the brainwashing by that ilk of humans.

How did America, and the world, survive without ‘insurance’ for centuries? How did they thrive? Living in the poorhouse in the name of safety and security and filling the fuel tanks of private jets of a certain class of human isn’t my idea of freedom. Hence, I’m fighting it. Today. Some of us will fight, and die, alone. I’m OK with that. I’ve made my peace with God.

Count the piles and enjoy the fireworks. Today is Independence Day. 🙂

Well I live in SE WI & with 0 claims in 3 decades, my policy just renewed @ +30%

I own a home in FL and I can tell you the insurance rates are already bordering on unaffordable and another big increase is going to put people in a horrible situation, buy the insurance or buy food, especially for those of us on a fixed income. The home that was affordable 5 years ago is now close to being unaffordable.

I really wish our governor would stop his failing campaign for president, he cannot beat Trump no matter what, and focus on solving the insurance issues we have in Florida.

Yep, I foresaw condo assessments rising in the wake of Sunrise’s fall and Ian. So, glad I moved.

He does NOT care about you. Even if he pulled out of race NOW,he’s toast in FL. He has his future secure regardless …

Is that you Niki?

… with states such as California and Florida ‘increasingly‘ hit by wildfires and hurricanes…

My emphasis. Leave it to liberal-loving Reuters to spout ‘climate-change’ trash like that. There are no real stats that show there has been any increase in hurricanes or their intensity. NOAA loves to “predict” such, but their forecasts almost always exceed actual. Here in NC (where maps of the Outer Banks have been redrawn several times in the past 100 years) this senior citizen doesn’t worry a bit more about hurricanes or their intensity than I did when I was a young man.

Years ago, a firefighter told me that when the economy goes down, arson goes up.

—————

Arson is a copycat crime. Being able to blame wildfires on climate change makes it easy to avoid the topic of arson and the risk of inciting more.

Being able to blame wildfires on climate change also makes it easy to avoid the topic of POOR FOREST MANAGEMENT. (Looking at you, California.)

The scary version is the scum humans in government planned it that way through purposefully poor management and preventing traditional and successful methods of management and then let nature take its course. Talking to loggers with decades of forest husbandry under their belts is quite enlightening.

It ties in perfectly with soaring insurance rates, onerous building restrictions in the new ‘wildfire zones’ and the destruction of American property and freedom under color of law.

Covid was a game changer in a lot of ways, at least for humans who survived it and learned about the operation. If eyes were closed before, I hope they’re open now.

Another tidbit.

Apparently the models used for carbon credits through forestry are not compatible with healthy forestry practices. I’ve been told that the hedge funds object to removal of trees.

I recently walked and rode some plantation pine forest land. The ground had 6-8 inches of pine straw. There were dead and dying trees everywhere from an IPS pine bark beetle (engraver beetle) infestation. A good thinning probably would have saved that stand of trees.

Such a shame…and hazard.

It’s even worse as real wages continue to fall. Much of our disposable income has been eaten up by groceries and insurance. Consumer items and going out to eat are now luxuries.

Unjustified premium increases = Financial Rape of the masses.

Back in the day there was an insurance commissioner that licensed companies to do business in a state and advocated for consumer complaints and against insurer malfeasance. Welcome to the Soros world where Communists were slid not only into DA offices and judgeships but also into agencies like the insurance commissioner.

We’re on our own and the enemy is formidable. Plan accordingly.

My (Geico) auto insurance just went up 30% YOY

Mine has stayed still, but I am retired on SS and drive very little except this weekend, one birthday and the Fourth with my grandchildren and their cousins and all the inlaws but not my ex. God is good.

Is it possible to build for cash in unincorporated parts of Florida with a road attached?

Insurance has gotten too expensive, too low return vs self assurance and self insurance.

Valid claims are often stiffed one way or another.

Even if you self insure I’d still carry umbrella liability.

I got tired of being stiffed. I live in unincorporated and there are lots available to build with roads nearby but they are 100K and up for quarter acre. The closer/better road access runs the price tag up a lot, without road access, there are some acre lots in the 10-30k range.

Super! So now Ron De$anti$ and Gavin Newsom finally have something in common! They’ll BOTH do absolutely NOTHING about it. Oops! Wait. Gavin Newsom has actually done something about it. He’s done what leftist politicians do … he’s spent tax dollars he doesn’t have. Gavin has “given” (read: taken) $72M to purchase 24 new firefighting aircraft for CalFire to use in putting out wildfires started by eco-terrorists who want to “prove” global warming is burning down our State.

https://www.nbcbayarea.com/news/california/cal-fire-adds-aircraft-to-fleet/3264960/

Sad trombones … Ron De$anti$ LOSES again. More sad trombones.

Scary version is if the Communists install Gel Boy as their next dictator, then everyone gets to enjoy the Kalifornistan way of life 🙂

I retired last year from a 26 year career in the insurance industry which focused heavily on property catastrophe insurance and I doubt it is the interest rate increases that are driving this. It is true that large swings in interest rates can cause issues (see Interest Rates & Insurance) but higher interest rates are usually good for insurance profitability especially in “long tailed” lines like Workers’ Compensation.

When discussing insurance rate increases Reuters states that “states such as California and Florida increasingly hit by wildfires and hurricanes.” Do you see what is missing? California earthquake is a huge risk for insurers but rates aren’t going up for it. We were being pressured by the reinsurers and ratings agencies (Moody’s, S&P, Fitch, etc.) to account for “climate change” in the rates we were charging. Basically hurricanes and CA wildfire are projected to become more severe due to climate change and the insurers are pressured to increase rates to account for that. Of course it’s bunk but it’s a matter of faith among management.

Gallagher Re can project away but their projections are just model fed opinions. Projecting a 50% increase is like telling insurance executives scary stories around a camp fire. Unfortunately fear sells so we’ll have to wait and see what happens.

That’s because very few people buy earthquake coverage.

I’ve got none. Why? Because something I learned from the Oakland Hills fire is that if you are a victim of a MASS disaster … then the government will come to your rescue. Why insure? When my fellow taxpayers and every building materials supplier will make donations to all us poor victims. Insurance is for suckers! Yeah … it took me years to unlearn my instincts and teaching about personal responsibility … so now … I just say fkcu-it!! Go bare and roll the dice.

According to the State of California, in 2022 CA earthquake written premium was $2.099 Billion while CA fire written premium was only $1.578 Billion, earthquake premiums were substantially larger than fire premiums. Someone in California is buying earthquake insurance

10 percent

10 percent? I don’t know how you do math but CA EQ premium is 33% greater than the CA Fire premium, that is substantial. My point was, and is, the reinsurers are blaming the price increase on “climate change” and not interest rate increases.

Can be. Can also be endorsement on the homeowners as in my state.

Living at the beach comes at a premium. Usually our rates in flyover country increase as well to subsidize beach dwellers when their property gets destroyed

Not just happening in these “catastrophic” areas. My youngest daughter had opened a Homeowners Insurance claim for a hot water heater that leaked, she lives on the upper floor of a stacked flat condo in the Midwest. Her neighbor below had water come through the ceiling so she opened a claim. No cash was ever paid out on the claim.