U.S. nonfarm productivity is a measure of economic activity within the engine of the U.S. economy. The U.S. productivity rate is a measure of how much value is produced by the economy through demand for the products and services, and the labor associated with the creation of those products and services.

I have often used the example of making bread {Go Deep}. If you are making 10 loaves of bread, there is a set amount of cost associated with each loaf created. The total cost of each loaf is the total cost to produce the entire batch divided by ten. However, if you have customers demanding 15 loaves of bread, you make more profit on the last five because it doesn’t cost 50% more in material or labor to make 50% more loaves.

I have often used the example of making bread {Go Deep}. If you are making 10 loaves of bread, there is a set amount of cost associated with each loaf created. The total cost of each loaf is the total cost to produce the entire batch divided by ten. However, if you have customers demanding 15 loaves of bread, you make more profit on the last five because it doesn’t cost 50% more in material or labor to make 50% more loaves.

Your productivity in the last five loaves is higher because the fixed costs of production (raw materials, energy) barely change, and the labor is only slightly higher. The opposite is also true. It costs more per loaf to make fewer than ten loaves because the fixed costs and your labor are pretty consistent, yet the finished value of 7 loaves is less than the finished value of ten.

Anecdotally, it has looked for quite some time that around May of this year the economy peaked, plateaued for a few weeks, and then began a slow downward progression. Today the Bureau of Labor statistics puts some revised data to that third quarter (July, August and Sept) economic activity {data here}. The quantified results align with what we sensed was taking place.

The value of all products and services generated increased by 1.8 percent. However, the labor cost of generating that small amount of added value increased by 7.4 percent. The difference between those two numbers is a drop in productivity of 5.2% over the entire quarter.

This is the largest quarterly drop in productivity since 1960 !

The Biden administration will blame the drop in productivity on a lack of material to produce the end product (ie. the COVID excuse). Which means employed people were sitting around waiting for goods to arrive and being less productive. There is a small amount of that which might be true. However, it is not the biggest factor, at least not on this scale. Keep in mind we are talking about both goods and services.

The more likely cause of such a massive decline in productivity is a genuine decline in demand. In the aggregate, consumers needed less goods and services. This likelihood aligns with the diminished and softened retail sales figures recently noted. It is a simple cause and effect. When gasoline, energy, and essential products like food cost more, consumers have less money for other stuff. Demand for the non-essential products drop.

As the demand drops, the productivity of the economic activity to generate those goods and services also drops. However, the scale of the decline is the part to pay attention to. A five percent drop in productivity is huge for a single quarter. Under normal circumstances this means more slack in the labor market, and that is what we saw recently in the retail sector of the employment figures from November {data here}.

During the month when retailers are customarily ramping up their employment to cope with increases in consumer demand, last month that didn’t happen. The ‘retail sector‘ lost 20,000 jobs in November. Think about that.

At the time of the November jobs report, the “national economists” were trying to figure out why the employment report missed expectations by 300,000+ jobs. We were not so surprised, because the actual result aligned with other data suggesting the Q3 economy overall was contracting. Consumers are being squeezed by inflation, that is creating a stagnant economy or “stagflation.”

Wage growth is currently at 3.9% {data}, and when combined with the loss in productivity, the unit labor costs for businesses at a macro level means a total cost of +9.6 percent in the third quarter. If employers do not start reducing their payroll costs as demand contracts, each unit produced will cost more money. Unfortunately, that dynamic adds to inflation and we grease the skids on this downward spiral.

I have not seen any financial pundits concerned about where this cycle naturally ends. Perhaps the media silence is because the White House knew the Q3 productivity data was alarming, and that stirred the administration to contact those pundits in advance in an effort to avoid widespread notice.

Regardless of reason for their avoidance, a drop in productivity of such a scale tells us to complete our economic preparations as soon as possible. The intensity of the inflation storm worsens with a weak employment outlook.

Leftists judge the success of their economic policy by how many people they can force into taxpayer funded government dependence = Economic Control / Tyranny.

Conservatives judge the success of their economic policy by how many folks they can liberate from welfare to become self-sufficient, productive Americans = Economic Freedom / Liberty.

If a bunch of white SUV’s roll up and loot your store, it might significantly affect your productivity.

IRS?!?

LOL! More likely a bunch of free lance socialists.

FWIW, Saddam’s guys drove those, too.

Well said!

America Firsters champion how many off food stamps and newly employed.

Global Collectivists champion how many newly unemployed and on food stamps.

Sure do miss me some “Promises Made, Promises Kept?”

I’m having a hard time finding conservatives, that truly believe in an economy with zero government interference, including taxes. I think they’re non-existent.

I can remember when there used to be real elected Conservative Republicans who said things like:

”Our government doesn’t have a revenue problem, it has a spending problem”

Well, sure, they SAID things like that but when was the last time they DID anything about it? Maybe Gingrich in the 90s. Since then? [Crickets]

We haven’t had a budget since 2008- BHO….he ushered in the era of Reconciliation and Congress has run with the open checkbook since.

Gingrich? Ha!

Maybe Ron Paul.

The original cause of our government’s spending problem is two-fold…

I realize that now the problem has evolved into a situation wherein our representatives go far beyond whatever might be requested by constituents; but, in my opinion, those two things are the origin of the problem.

It’s also clear that those two things still exist; and, our present problem will never be solved unless and until they cease to exist; i.e., we will never get government spending under control as long as We The People ASK for unconstitutional spending or continue to vote for those who promise the same.

When we kick NGO’s and lobbyists to the curb, we may get a handle on things.

Animals don’t have a concept of your or other’s property.

Neither do the vast majority of people.

If it is any consolation, I believe that there should be as little government interference as possible, and whatever governance there is, should be at the lowest level possible (i.e. municipal, county, state). The only thing I want the federal government to do is to provide for the common defense which they used to do pretty well. Not so much now.

And heck, even the common defense should have the smallest possible ground forces and each state a large militia.

Defense is good, but I’d be happy if they just prevented the

ongoing invasion by non-Americans across our southern border,

who are a drain on our social safety net !

Biden has failed, he SEES his failure,

and then doubles down on his failing policies.

One can “fix” ignorance…but there is no “fixing” STUPID !

OR…INTENTIONAL DESTRUCTION…OF OUR ECONOMY !

Biden’s advisors or directors must be ADMONISHED severely.

We did NOT elect his advisors or directors.

Biden is doing what Buraq and Xi Jinping tell him to do.

Biden has always been brain dead IMO, but he knows who owns his crime family.

Failure is based on the desired outcome. When the desired outcome is achieved, it is success.

Failure cannot be that widespread in an administration. Forget the words to spin the perception that they want the same thing you want. Focus on the actions, and the outcomes. They are very successful in achieving the outcomes they desire.

The Obama fundamental transformation laid the groundwork and seeded the entirety of the bureaucracy with their worldview. Trump was fertilizer to their groundwork. Brandon’s admin is merely cultivating and harvesting the crop.

They only have 2 things outside of their grasp. Wholesale federal control of elections and full implementation of the Green New Deal. So like the Obama admin, they will do everything behind the scenes. Fortifying the fields. Harvesting as much as they can.

That is not failure. Don’t underestimate the enemy.

I’m thinking that China owns more than just the democrat party.

IMO General Milley works for China, and there’s probably plenty more like him at the Pentagon.

The Wall Street economy is booming, but Main Street has been forced to shut down.

Mission accomplished.

Not non-existent.

Social Security had a cost of living increase of 5.9% for 2022, the largest increase since 1982. The viability of the SS fund will be hit hard by this increase. Obviously, stagflation is here.

A personal side note: My Social Security benefit increases 5.9% for 2022 while my Medicare insurance premium increases accordingly.

In other words, my net SS income for 2022 is EXACTLY the same as for 2021!

Let’s Go Brandon!

Please. Food stamps got a 25% increase in the same timeframe. I can tell you this, my mom’s Medicare went up 15%. That means that mom just got a 10% CUT in benefits she paid for in taxes over 50 years by working in this economy. They are destroying the elderly and making them lightening rods for hate by ONLY blaring to the world that seniors got a 5% increase in SS bennies. My elder deserves better. Doesn’t yours?

I deserve better. I’m an elder.

They’ll blame it on ChiCom19 and then explain that even more draconian lockdowns and jabbing are necessary to in order restore productivity.

Right you are. The death shots ARE the NEW economy. I heard someone admit this a month ago online. The leader of New Zealand maybe? If I find it I’ll post the interview. God help us all…

Positive spin coming from the Biden Regime and Corrupt Media. Trump social media and news platform can’t come fast enough.

Stock up on essentials. Get your car fixed right now, tires rotated, get whatever medical procedure you need done right now. If you need a new appliance, don’t wait. Just be prepared, commies are planing a completely new world.

Build back better calls for a new economic system.

The great RESET, destroy the current system.

They are openly saying it.

They want “energy to necessarily skyrocket.” They want pain and suffering so we accept their “help” to fix everything.

Good advice.

Even ants and squirrels know how to prepare for winter.

This is our time to be wise and gather summer fruits before a great winter sets in.

Theres a severe shortage of fruits and vegetables; they are all in D.C.

That depends on what you mean by fruits and vegetables. 🙂

Especially fruits😂

Stock up on: .22LR, .45ACP, 12g and….

Ain’t UTOPIA grand?

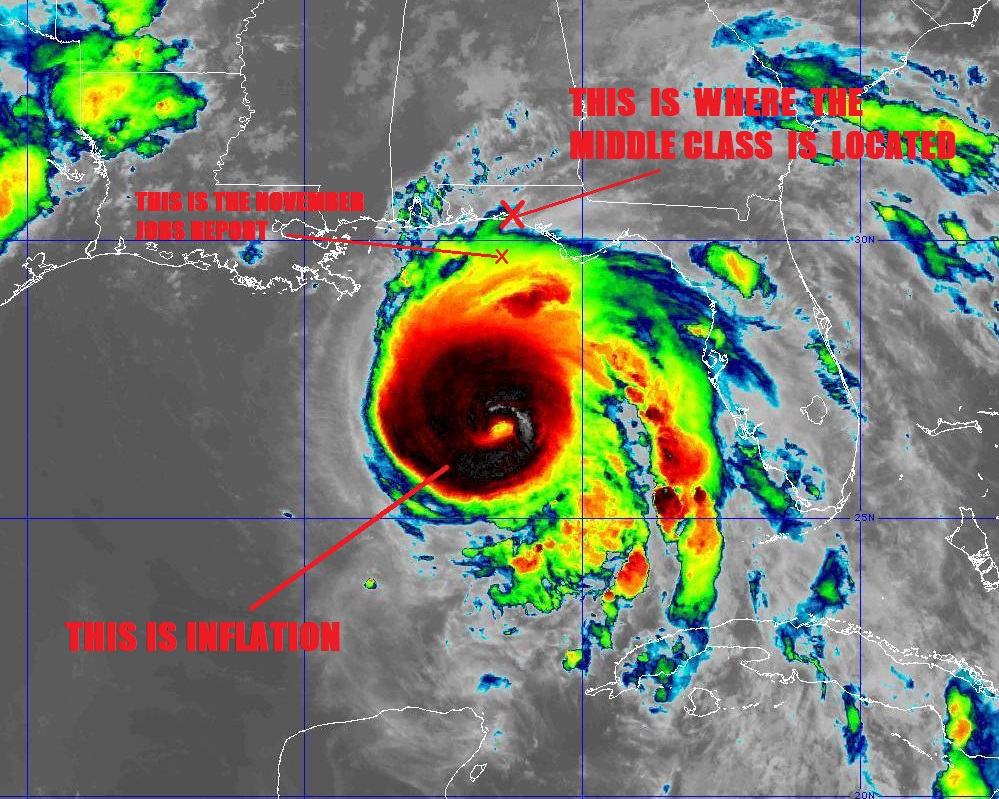

Yeah west side of a ‘cain always gets the most destruction. Doesn’t look as big as Katrina but a powerful one for sure.

A direct relationship between demand and economic productivity, as they say in ECON 101.

As a major hurricane survivor, it’s the NE quadrant that’s the worst.

Katrina, Rita and going way back, Camille.

West side would be left, so keep right?

clever, but the original comment is inaccurate. It’s the right side that causes the most damage.

Northern hemisphere hurricanes rotate counter clockwise, so the right side has the strongest energy as it moves forward. The right side is where the storm surge is worst, with the heaviest flooding and coastline damage.

In the Gulf of Mexico, that’s the East side. On the Atlantic coast, it’s the north side, generally, depending on the direction of the affected shoreline.

This economic hurricane surge is going to push a lot of crap and garbage on us and the back side is going to blow out a lot of wealth and stability. But we will recover. Permanently changed, but into a new paradigm.

You have to go to weather school. The storm is rotating counter-clockwise. If you are a Millennial or younger I can explain counter-clockwise:

In the old days we had round clocks with minute and hour hands that moved in a clockwise direction, which was the same as what you do to tighten a screw with your screwdriver. Screwdrivers are those handy tools that can help us put together the new stuff we get from Amazon. No offense here, I just thought this might be funny. 🙂

Righty tighty, lefty loocy.

I do not understand how the guy keeps his job. He lies like Raggedy Ann.

See right above you?

THATS how!

By saying WHATEVER he is told to say, and say it enthusiastically.

If told to, he would advise people to invest in excrement and death, he doesn’t CARE.

I know that he is just spouting propaganda. I still wonder why people listen or do they?

He keeps his job because people watch his show.

Re “I do not understand how the guy keeps his job. He lies like Raggedy Ann.”

Your second sentence is the answer to your first one…

This is the same idiot that said there should be a -national vax mandated and imposed by the Military – Actually said words to the effect on TV…

Cramer has mildly pushed back on some of the extremist socialist positions out there, but he is CERTAINLY in the pocket of the Dems and his employer.

“Strongest economy ever seen”….what horse crap. It’s been a strong stock market for sure, but the bulls ignore so many cliffside warnings as they scale ever higher up the mountain fueled by this Fed and Covid spendaholics.

Cramer needs his job as is evidenced by his doing what he is told where he works.

The Stock Market isn’t the economy.

IMO Mr. Cramer is not an economist.

You can tell the economy is going to hell in a hand basket by looking at how few extra workers were hired for the Christmas season.

I know some businesses hired more seasonal help, like UPS, but many didn’t hire any (or fewer than usual).

Was at a FL outlet mall not too long ago, empty shops for rent, I quit counting at 15. Few shoppers for Saturday at lunchtime.

1960 is 61 years ago, not 51. Which is correct, 1960 or 51 years?

Like it matters which one?

Yes. You have the math right.

Probably 1960 or 61 years ago.

They fixed it. 61 years and 1960.

I remember how we always used to judge the Soviet Union on their empty store shelves and attendant long lines of waiting people.

It was a hallmark of socialist economies.

It still is.

Southern Nevada here, cracker section in major grocery chain stacked two boxes deep, very limited selection. Across the aisle, no peanuts (Planters) anecdotal yes, but not the first time I’ve noticed shortages.

Economic inertia takes time to dissipate. This isn’t the artificial stop we saw due to lockdowns. Now it is for real.

Economic inertia takes time to dissipate. This isn’t the artificial stop we saw due to lockdowns. Now it is for real.

“Foreboding – U.S. Productivity Declined 5.2 Percent in Third Quarter, Largest Quarterly Drop in 51 Years”

—–

Unexpectedly.

Sundance:

You are talking Economics 101 perhaps to 303.

Common sense economics.

Newer commentor, but long time reader who has appreciated your economic knowledge of supply and demand and all the complications and politics in between that disrupt an even flow of both.

Thank you for this.

I know nobody else putting this out there like you do.

I’ve been through the worst hurricanes so I know why you post that image.

Brother of truth, don’t relent and give up one inch of what you say and present here on CTH!

The economy? I have the solution. FJB.

Now how is having sex with a demented octigenarian gonna help?

Jill won’t even “go there”.

Sundance i am sure you are getting tired of hearing this from me but i will say it anyway . THANK YOU for keeping us so well informed. blessings to you ad rem and everyone at C.T.H some times i wonder if you truly understand how much good will and prayers we send your way . hope you can feel how much we appreciate the time and effort you dedicate to growing this tree GOD BLESS be well my friend R.D.

Hear! Hear!!

I sometimes forget to THANK Sundance for all his work.. Thank You for the reminder.. However, I do NOT forget to *donate* on a regular basis as we all should do…

Clearly we must get into a war wit Russia over Ukraine to boast productivity. Or if not Ukraine, then Uganda.

How about war with Australia ! That way you get to play Trojan Horse ! a win, win , we get to defect we all kick the chings and commies out and onwards we march !

P.S. and Mungrel get 50 cal.

The ChiComs already have Australia penciled in for an invasion. The way things are in Australia now the Aussies will welcome them as liberators

I must’ve missed something. Why Uganda??

Russia may not take the bait and we we must have a war to boast productivity for Joe and Kamal. Who it is with is incidental.

If Joe sends any military equipment to Ukraine, I’d consider it a gift to Putin.

Just like the gift to Afghanistan. Now they want to get back to selling weapons to the world.$$$$$$$

And of course JoBama says we need to support the new taliban / government of Afghanistan.$$$$$

I’m sure it’s all in the new “Break the Back of America” bill. US tax dollars to taliban.

Plenty of amnesty stuff in the bill too, complete with reparations for illegal aliens.

AH! Ok. Thank you!

Cause there such idiots, that they get countries confused, that have same first letter.

Oh, you know THE THING!

Why Uganda??

The armchair generals are hoping for a win.

Because somebody has to restart the AIDS epidemic.

And those bodies aren’t going to eat themselves.

(Ref. to Idi Amin, for those not as ancient as I)

Heck we could just reinvade Afganistan.

Our Generals are now all claiming they never heard of it.

I heard they are complaining that the militants are too well armed in Afghanistan now. They are puzzled as to how the terrorists got so armed but they feel they can investigate and in 55 years let us know.

Didn’t I see that Biden was sending VA and WV National Guard troops to Southern Africa? I never was sure what that was about. I thought they were worried about the “new variant” coming from that part of the world. They use our troops like pawns on a chess board, and they are not very good at chess!

He’ll punish us all eventually.

We can defend Taiwan, Ukraine, Timbuktu, etc, etc, until the cows come home.

But we can’t stop the ongoing illegal invasion of the United States? That’s too important, we have to keep that going.

JoBama might think that China and Russia are afraid of him, but they’re not.

Russia already has over 120 thousand soldiers on the border with Ukraine.

The US military / General Milley is too concerned with gender pronouns, global warming, and white rage.

That’s why our military has tested Hypersonic weapons 9 times in the last 5 years.

China has more than 500 tests on Hypersonic weapons in the same time frame.

…and that’s why the Federal Reserve cannot tighten monetary policy or raise interest rates. Goldman Sachs, Blackrock, Janet Yellen, the tech billionaires and the Federal Reserve spent billions of dollars to get rid of President Trump they are not going to sabotage Biden and the Democrats anymore than Biden and the Democrats sabotage themselves!

Coincidentally the end of May is when the Equal Employment Opportunity Commission released its guidance that allows employers to set ‘vaccination’ as a requirement of employment. The 3rd quarter was when employers began deploying their mandates that employees be ‘vaccinated’. I see a definite correlation between dropping productivity and employers significantly alienating, anywhere from a quarter to a half of their workforces.

The financial pundits are unable (or unwilling) to grasp the effect that coercing workers into receiving experimental medical procedures under threat of destruction of their livelihoods is having on the economy. They’re flabbergasted that productivity is dropping and that there are millions who have willingly removed themselves from the labor pool.

They are like those two Dr’s in England that recognising the #of people being seen in ER’s for heart problems are skyrocketing,…

propose the COVID stress is causing it.

Many think they are gaslighting, but to me the more fearful and likely possibility is that they AREN’T.

They actually BELIEVE what they are saying and aren’t consciesly ignoring the obvious, they just don’t SEE it.

Same with these financial pundits.

Past = Lets not relitigate the past. C’mon man, Its been five days already, move on already

Present = Today we have the strongest economy, perhaps, I’ve ever seen.

Future = We are not in the prediction business, and wont be making any forecasts

Good summation of the FJB administration and enemedia.

I’ll add, if none of those are readily palatable, default to blame President Trump.

Thanks for the economics lesson Sundance.

I was thinking the remote work from home has something to do with the drop in productivity

Or the constant bombardment from the Biden Residency: “You need to pay more taxes” “You are racist.” “You are from henceforth and forevermore mandated to take the Clot-shot every 6 weeks”, ” You are homophobic, transphobic, xenophobic, islamophobic, and Lincoln projectphobic.

After a year of this crap maybe people are just giving up a bit.

Third party sellers online often selling stolen goods. Retail CEO’s want help from Congress to ensure better oversight and regulation for smash and grab and then sell online.

https://www.businessinsider.com/retail-ceos-congress-stores-theft-anonymous-online-retail-crime-2021-12

The extra $300 per week fed chicom cooties money ended with Q3. Not sure how it impacted productivity, but it would seem to impact demand.

I am not a business geek but somewhere in my cerebral meanderings, I hold to my hypothesis of jobs being available and ‘no applicants’: Business is not really hiring as that sounds better than lay-offs in an ailing economy. COVID schmoevid, it’s about balance sheets. Payroll is a huge aspect.

People are not working. My son works as a chef at a “retirement home.” This home is fully compatible with the older individual who needs 24-hour care. They also have a memory care ward. They also have an assisted living side and a non-assisted side. Lots of things going on there. I also have a family friend who owns two restaurants- one is a higher-end, make a reservation type, and the other is a pizzeria. In addition, I have a friend who is a landlord and owns over 600 units (single-family to apartment buildings). All have said the same thing:

No one is applying. People have quit.

At my son’s work- nurses have left, janitorial staff has left, kitchen assistants have left, etc. This is all because of vaccine mandates. One nurse told the VP at a “mandate standdown” she would never take it, called them all tyrants and fools, then quit. Another nurse walked out with her. That was two months ago. My son said more had left since, and no one answered the job postings.

The friend who owns the restaurants- same issue. My son, who works as the chef (the one mentioned above), helps her on his day off by working as a delivery driver for 8 hours. She said- no one is applying, but people are quitting, and she doesn’t require anything regarding the vaccine- but no takers.

The landlord- same issue. But he did say there are many new “Mexicans” available to help under the table. He and I live about 1/2 mile apart. We both hear the National Gaurd planes and helos that fly over for the past nine months now (more than we have ever seen). He says that since most Americans are not applying, those planes and helos are music to his ears. He said it never fails that usually a day or so after we hear heavy air traffic…..he sees a plethora of new faces at the place he goes to find “help.”

And, he hates going there for help, but as he said- FJB is forcing him to use them because legal citizens don’t want to work.

They bring in their illegal alien friends to vote democrat.

Then they try to make it legal, for the illegals to vote in OUR elections.

New York is leading the charge.

https://www.foxnews.com/politics/ny-republicans-vow-legal-action-non-citizens-voting

The obesity epidemic, opioid crisis, and plenty of freestuff are lowering productivity.

All thats needed now is a War to take people’s minds off the crummy economy….

…and to enact more of those special ‘Emergency Powers’ of which leftist government is so fond.

“It’s for the children.”

Great and pragmatic analysis from SD as usual. Speaking of productivity malaise, never has a nation been more studiously informed of its inexorable slide into a Marxist hellhole without taking productive countermeasures to reverse it. There was no pre-existing cautionary tale for Russia in 1917. America in 2021 has no such excuse. The Patriot malaise, to quote a Carterism, is astounding. A reprise of 70s stagflation is the least of our worries. Back then, they came for our purchasing power. Today, they come for a lot more. I’m coming less to blame the elites and point the finger more at the passivity of the populace who, a long time ago was charged with the weighty burden of self-determination, but clearly shirked it somewhere along the way. Why can’t Americans be more like the French? Too many thought-provoking blogs. Not enough Yellow Vests.

This article shows one of the reasons I value this site: pure facts, sound reasoning, and no BS. Thank you, Sundance!

Hear that the inderground economy is doing pretty good. 🤔

underground

We prefer the term parallel economy. 😂😂

Ah, yes, and as my economics professor called it “the tertiary economy.”

My productivity has significantly dropped since my employer has threatened to fire me over the notavax mandate.

For the life of me, I can’t quite figure out why….

The CCP waited out the U.S., and helped electorally defeat the great president, and the CCP has achieved victory without battle, with the assistance of legions of useful idiots and grifters.

“The greatest victory is that which requires no battle.”

― Sun Tzu, The Art of War

Taking Hong Kong without a battle? That is some kind of victory. To help the U.S. defeat itself? Priceless.

And now the CCP can fuel the inflation fire and watch the flames.

The econ phrase you are looking for is “economies of scale”.

People are so ignorant of history. During the Carter years there was massive inflation gone wild. Reagan appointed Paul Volcker to reign in the inflation monster with draconian interest rate rises, to tame it. People complained but it worked.

But it didn’t work. What worked was the Reagan tax rate cuts and the sunseting of the inflationary union, etc contractual rate increases above the rate of inflation. Massive unemployment took the leverage away from the unions.

Volcker’s interest rate increases just caused needless suffering. We all just sat there without jobs and no demand while price increases still kept happening.

Anarchy is now a mainstream Democrat attitude. Partly it is the very cynical recognition that poor people become dependent on the State, and thereby the Democrat Party. These monsters have turned poor blacks into their serfs.

And anarchy appeals to people full of anger and hate (Antifa, BLM). The tearing-down part is exactly what appeals.

The welfare state is more addictive than heroin. How did Trump’s attempt to inspire a revolution in Venezuela work out? People frankly adore all the free stuff, and when the free stuff inevitably peters out, they’d rather wait for the return of the free stuff than start anew. A cargo cult.

Entrepreneurs are becoming scarce on the ground in America. The lockdown crushed many, many entrepreneurs. How did door-to-door salesmen make out during the lockdown? Avon calling – ha!

@sundance – considering how bad Biden’s job numbers were for November, they would have been worse had it not been for conservative governors in key states. Something like 17 of the top 20 states seeing a recovery (by getting their people back to work) are Republicans.

So, without those Red State numbers in his job mix, and as bad as they are, JoeBama’s policies had absolutely no place to hide as the unmitigated disaster they truly are.

Another excellent and useful explanation on why we are where we are!

This just can’t be…The MSM say’s everything is beautiful…Economy is booming, gas down drastically by a whole two cents a gallon from being up a dollar or more, Mayor Lightfoot of Chicago says crime is way down, pfizer & Herr Fauchi have the cure for the Covid Omicron variant, (Only one more shot (Or maybe two)), blah…blah….blah…..

FTA:

“ The Biden administration will blame the drop in productivity on a lack of material to produce the end product (ie. the COVID excuse). ”

Not quite. With the help of their media sycophants, they’re actually trying to claim that Biden is presiding over the quickest and most successful economic recovery in 60 years. All that, despite the low workforce participation rate, high prices due to record inflation.

These jerks continue to gaslight the public while they cherry pick counterfeit FACTOIDS that are meaningless.

LETS GO BRANDON!

That’s not a bad looking dough ball on that cutting board, it sort of makes me want to make some bread. Hopefully most here have a modest supply of the basics so they can thrive under FJB’s second year.

I wrote several months ago that the goal would be rationing of all basics and maybe even some not-basic things, accompanied perhaps by government-issued permits to buy those rationed items.

In other words, a completely Sovietized, Stalinized economy which the Russians suffered under for most of the 20th century.

The twist is that supposedly knowledgeable pseudo-capitalists i.e. crypto-capitalists will be involved in the destruction of our economy. And why? Because they are the puppeteers at the top pulling the strings and milking what is left: a guaranteed slice of the world’s economic pie produced by miserable bakers working for a pittance and told to be happy with that pittance.

Check a silent German movie from the 1920’s called Metropolis which satirized the fledgling totalitarian states back then. Moloch, the baby-eating god, is alive and well today, his tentacles spreading now thanks to the DEMS and their crypto-Communist allies.