For several months the Trump administration has been talking about a “V-Shaped recovery,” meaning the COVID-19 rebound would be as strong as the preceding quarter contraction. Today the Bureau of Economic Analysis (BEA) released the third-quarter economic stats reflecting exactly that, a V-shaped recovery.

The 3rd quarter rebound in GDP growth was 33.1 percent, larger than the 2nd quarter contraction of 31.4 percent. And keep in mind this is with a major part of the U.S. leisure and hospitality sector remaining severely impacted. [See Table 3, Line 20]

Despite several blue states attempting to stall their economic recovery, overall the economy is rebounding as expected. Obviously the threat of COVID has been weaponized as an election strategy. It is against the interests of the administration’s political opposition to support a more honest, open and engaged economic recovery.

All of these economic indicators highlight the visible reality on the ground. Despite the ongoing challenges there is good news for the most heavily impacted sectors of the economy: leisure and hospitality. Well over half of those jobs lost have been recovered. In the past four months 3.6 million jobs have been gained in this sector. Employment in food services and drinking places is still down by down by 2.5 million since the peak in February but the gain is significant and reflects a “V-shaped” recovery ongoing.

All sectors of the economy are gaining jobs back at a remarkable rate; and the key demographics are benefiting in proportion to the initial COVID-19 impact. [BLS Report HERE] With the expiration of the “extra” federal unemployment benefits at the end of July/August, the negative incentive has been removed; more people are stepping back into the workforce.

A September 2020 comparison to September 2019 [LINK HERE] – [PDF HERE] shows last month’s retail sales jumped a whopping 5.4 percent year-over-year. That means last month saw consumer spending 5.4% higher than consumer spending before COVID-19 hit the U.S. economy. Keep in mind two-thirds of U.S. GDP is driven by retail sales and consumer spending.

As many of you know I have been traveling extensively throughout the country as I continue to brief groups on background DC, DOJ and FBI information from my years of research. During these travels I make a point to visit sector-specific businesses to inquire about their economic and business growth status.

The disconnect amid a ground reality compared to business reporting and financial media is actually stunning. However, perhaps that is because my physical ‘on-the-ground’ inquires and reports are ahead of the natural lag in the economic data rolling up to the accounting level. Here’s what I can tell you with absolute certainty.

The disconnect amid a ground reality compared to business reporting and financial media is actually stunning. However, perhaps that is because my physical ‘on-the-ground’ inquires and reports are ahead of the natural lag in the economic data rolling up to the accounting level. Here’s what I can tell you with absolute certainty.

The amount of heavy equipment, industrial equipment, hardware and goods being moved around the country is more than I have ever witnessed or seen in decades of travel. The mid-west, mid-atlantic, southeast, and more specifically the south in general, has more haulers and semi-trucks on the road than I have ever witnessed…. ever…. by a substantial margin. The same is true for rail freight and cargo vessels.

Regardless of what financial pundits and economic media might be saying, the underlying economic activity in the U.S. right now is explosive and moving at a much more rapid pace than before the COVID crisis [statistically confirmed today]. Regionally, business owners and operators all report the same thing, and the same need for a larger workforce. All of them are hiring; however, some sector specifics and regional specifics are much more intense.

Thank you, Lord, for Pres Trump and his amazing team.??❤️??

This is excellent news by any measure, but the math feels funny here….

Let’s say our GDP is $100 pre-covid….A contraction of 31% would mean Q2 GDP is now $69. A rebound of 33% would mean Q3 GDP ~ $92. Close to where we were, but not quite. Am I wrong in this understanding?

It depends on the basis of growth calculation. Year to year is a bottom line. Employment and hiring are also important metrics.

That’s correct ssd. Also we should remember that these numbers represent an “annualized” rate, which means they multiply real quarterly change by 4. I don’t think many people get this. The real decrease in the three months of Q2 would have been a little less than 8%, and the Q3 recovery a bit more than 8% up from the end of Q2. Imagining a swing down to 69% of our usual economy around June-ish would be shocking!…and thankfully not true.

Actually I’m going to amend this a bit. Maybe the economy really did get down to 69% the usual daily rate of GDP at the end of Q1. But it was just for the time being. Since it didn’t stay down for a year, it won’t ever have dinged our economy on an annual basis, the full 31% over the year. But I’m going to ask that no one quote me on my comment above because it is mostly wrong. Sorry. Putting myself in commenting time-out for now.

Are you mad? On the internet you are supposed to double down twice on anything you say that might be a little stupid. AND USE ALL CAPS so people know you’re right!!

What in the Wide World of Sports are you guys talking about?

Yes, I’m afraid you’re wrong. Try re-doing your arithmetic: $100-$31=$69+$33=$102 (not $92)!

made me giggle…I love the minimalist approach….it’s %, not $…but either way, the V has been accomplished…going for my 5th beer…MAGA

5th beer from alum can. The trade war prophets said the can cost would go outa sight.

No, you are wrong. You don’t add $69+$33. You add $69 plus 33% of $69, which is another $23, and $69+$23=$92.

Unfortunately, the original post was wrong as well, because the numbers announced are annualized rates of change, compounding four times (which is not the same as multiplying the quarterly change by 4, as someone else suggested).

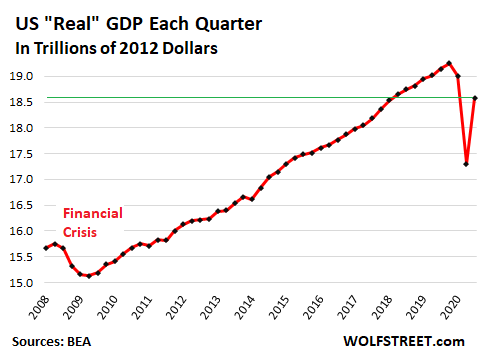

All the changes in question relate to real GDP, that is, GDP adjusted for inflation. (I prefer to focus on real GDP per capita, or real disposable personal income per capita, but I don’t write the headlines.)

The simplest way to understand the changes is simply to use the absolute number for real GDP, which you can find on the FRED website. Here they are for the most recent quarters:

2019Q4: $19.25 trillion… Call this index = 100.0

2020Q1: $19.01 trillion… index = 98.7

2020Q2: $17.30 trillion… index = 89.9

2020Q3: $18.58 trillion… index = 96.5

We are most of the way back, but we definitely need VSG PDJT for 4 more years to clinch the win.

OMG…. Where in the HELL were YOU when I was suffering in Macroecononics course?? ? Do you realize, apparently, that FEW can EVER teach macro this well?? ? Dammit….had YOU been my instructor…. I could have banked an A! Thanx for simplying things…. ?

Not sure what you’re asking. Having almost pre-CCPv numbers is probably miraculous considering that so many blue states have intentionally destroyed their economies.??♀️

V for Victory!

Or . . . 5 more beers!! Sorry, couldn’t resist 🙂

?? That’s right….. AND this is when a CORONA is always WELCOME! ??

Now if only the markets would react in a positive matter.

Don’t worry. Next Wednesday the markets will be just fine.

Markets right now are nothing more than gamblers using any excuse to manipulate the market. They make money every time it moves, up or down, but it HAS to move.

Actually its a great buying opportunity.

Wish I had some cash to put in, I see deals deals deals. American airlines 10-11 bucks, that’s going to be 50 in a month. Maybe 2, but the gubmint is going to be cutting them a big check soon. I like nclh at 15 but that’s a long term position, like I think it hits 60 again in 2 years. I just got up a little while ago so I’m still catching up but when I crashed that was happening.

A close friend who has been playing the market for years said he was taking his out until after the election just in case Biden wins.

If President Trump wins he’ll re-invest it. I don’t think he’s the only one doing this either.

Everyone moves to defensive trading positions before an election. Maybe hedge fund contrarians roll the dice.

He’s going to be too late. The bold are getting in now at the dip and banking on President Trump to win. It might even go up before Tuesday as it starts to become more and more obvious.

If the economy is in fact going to continue to recover ( not a given – we may slowdown sharply in the next couple of quarters) – interest rates will rise, the Dollar will strengthen . And most important, the Fed will take its foot off the gas. And the big tech stocks – Apple, Amzn etc are hugely overvalued. Apple is trading at a PE of 40X , very high for a company with slightly declining revenues/profits over the past couple of years. Probably a decent investment at a PE of 15X.

But the main thing is – a very strong real economy is not necessarily good for the stock market. Although we may see nice returns in the industrial, energy etc (old economy ) stocks. Problem is the “market” is dominated by the handful of mega-cap tech stocks.

For stocks who sell air for a living, and want to get rid of affordable energy?

Suspect growth plan!

Inventories are DEPLETED. That means OVERTIME, 3 $hifts, and HIRING.

What Sundance is describing, IMHO, is that the economy is doing pretty much what Sundance WAS predicting it would be doing, at this point, BEFORE the china virus.

The switch from a Wall Street dominated economy, to a Main St. dominated economy is ONGOING, and hardly affected by the Virus.

In fact, the PPP was distributed, to a significant extent, by the alternate financial network of smaller banks and credit unions.

MAGAnomics is ongoing, the virus was NOT able to stop it, or even really slow its momentum.

New car sales up 1200 percent! Thats UNHEARD of. Housing starts as well are WAY up, and low inventory.

Next year, again RIGHT ON SCHEDULE, the Economy is going to get another shot of Nitro. MOST of the factories that have been brought here, will be going “on line” next year.

All this despite a number of LARGE, productive States remain shut down. The economy can only go up when those States open up, which they must and will do, after the election.

Bet on America and President Donald J. Trump, and you can’t lose.

Love this winning!

You have to pay $$$ for quality and Apple Computer is the cream of the cream when it comes to quality. Every teenager in the world wants an Apple iPhone and tablet. They want Apple music and will have their parents subscribe to Apple TV. On top of everything Apple investors don’t sell their shares and Tim Cook buys back millions of Apple shares each quarter with it’s billion dollar cash horde. Go to the mall and walk buy an Apple Store…its always packed with customers. At $115 a share it’s a steal.

It is not unusual for the markets to go down at the end of the year. This is because investors will want to take losses on some loser stocks for a tax benefit. Also the election is having a lot of uncertainty this year, so that adds to it. January will be a great month for the stock market, and maybe sooner.

True. Also if our DJT wins ( pray hard!) – we will probably get an industrial rennaisance – so all the old forgotten sectors – like heavy industry, infrastructure, energy , metals etc should come to life . The overpriced, over-loved tech stocks may have a decent decline.

people will realize there is more to life than fancy overpriced phones and gossip chat sites!

Again, its the steady parting of the ways, of Wall st. vs. Main st. At this point, its inevitable, can’t be stopped and the consequences are foreseeable.

Anyone who hasn’t “taken the coarse” on Sundances MAGAnomics 101 yet, need to ASAP.

Just go on CTH home site, find the search box for the archives. Type in “Lemons or widgets”, “exfiltration of wealth”, should get you to his archived series.

Word to the wise; I read the material over and over, only getting a couple of paragraphs farther (each time) before my eyes glased over. But, I kept with it, until I had my “Ah, HAH!” moment.

Economic Security IS National Security;

It innoculated us against a bio-weopon attack, which is really an attack on our ECONOMY.

Notice how ours, is so much better than anyone elses. Its like antibodies for our economic body.

The market reaction is good. Market believed the polls. Now it knows Biden isn’t a guaranteed victory like press has been saying. Markets hate uncertainty. Let’s just see what happens over the next week.

Nancy has already taken credit for it. Biden will be next.

Followed by Zero.

You know it.

The real estate market on Long Island is firing on all cylinders as people flee from New York City, and the underlying fundamentals of the economy strengthen.

2021 is going to be an amazing year to kick off President Trump’s second term.

I heard today that is the case here in Westchester County as well. People are snapping homes up to get out of Manhattan.

We have a housing shortage in Charlotte, NC. Builders haven’t missed a day.

TrVmp.

Hey, I like that!

That is a hat that will sell in MASS amounts.

Yes

Bigly ! Yuuuge !

I hope someone tells them. As they say that MADMAN will sell it!

Love it!

And anyone that thinks a Biden/Harris administration will let this recovery continue is deaf to what they have been saying (or is intellectually dishonest).

Or just plain stupid.

All of the above.

All of the above.

Don’t worry…We will be back to normal on Nov 4.

BTW…I caught a moment of Sleepy Joe talking ( screaming actually, LOL) in Fl & I was amazed at one point he made which says it all about his campaign’s position to defeat Trump….

He said…”If Fl goes RED it is all over….” (paraphrasing but pretty close to a quote).

I am amazed that his spokespeople haven’t “corrected” this position as yet. He states that IF the Dems lose Fl it is over for for them…That speaks volumes as to their chances for a win.

Think about that….Biden says if the Dems lose Fl they have no path to 270….He said that out loud! WOW, time for an IV Cocktail for this boy & off to nappy time….

Well at least he spoke truth this time. IMHO, even with Fl they have zero chance to win the race.

Yet another Irony. Only NOW, when he’s getting dementia, is Joe Biden starting to speak the truth.

Looking into the camera, and wirh “PREPARED REMARKS” mind you, assuring viewers that he had the largest vote rigging operation ever assembled, the one Barack used, and now saying if he loses Florida, its over.

And, he admitted he’ll kill oil. We should get a list of times when Joe hasn’t just ‘gaffed’, (too many) but specifically where he has inadvertently told the TRUTH.

This! I was thinking the same thoughts.

Wow.

Apparently the part of the brain that determines whether a person will be a habitual and talented liar has been affected by his two brain aneurysms and incipient dementia.

His lie-meter is slowing down or breaking?

I’m surprised there aren’t research scientists beating down the door to reserve a specimen for study on the future day he checks out…

He promised the Great American Comeback and he is delivering!

https://www.donaldjtrump.com/landingpage/greatamericancomeback

I work in an investment advisor firm and I have been listening to my boss (uber elite liberal) stating for months there will be no V recovery. He walked into his office today and closed his door so I could not hear him talking to his clients.

You need the patience of a saint. God Bless you.

Thank you. I have been listening to him for four years call our President “Fat Donny” to my other coworker (another misinformed liberal). He knows I am conservative, but I say nothing. Oh….he watches CNBC all day long too!

Yes it is obnoxious how the uber stupid feel entitled to spew their ignorance and hate and we smile and carry on.

So how as his investment advice been holding up ? Maybe he should try Newsmax or OAN just for perspective . LOL Good luck around that office.

You may be the boss in short order.

The dumb and stupid are his clients. Never do business with a Libtard investment advisor. It is a sure way to eventually lose your ass or at the very least underperform.

Libtards are psychologically insecure with huge egos….a horrible combination. Libtards can only see what they believe and cannot believe what they see. Who in the World would entrust their money with someone who has the common sense of a barnyard turkey?

Libtards are easily manipulated, allowing their emotions to get “triggered”.

A strong enough emotional responce causes the critical thinking part of our brain, the part that QUESTIONS EVERYTHING, to go dormant.

This has been proven with PET scans, although “con” artists have known it, forever.

Once you mute the critical thinking part of the brain, you can convince them of ANYTHING.

Fear, Hope, Sympathy, Greed, ANY emotional responce, if STRONG enough, will have this effect, on EVERYONE.

Believing something, because you are manipulated into WANTING to believe it is true, STARTS with triggering such a STRONG emotional responce.

Then, a “good line” of B.S., and your there, getting the mark to sign away their life savings, or freedom and heritage.

Manipulation, 102 and 102. And you LEARN how it works, so you can try to RESIST it.

And that starts with taking control of, and even tamping down your emotional responces.

If you are “hearing” the critical thinking part of your brain, questioning, challenging, then you know its not “mute”; its like “feedback”, to let you know its working.

The old snake oil salesman of a long time ago would have had a field day with todays ding-bat Libtards.

fanbeav, for years I used to watch CNBC from market opening to closing until PT was elected. CNBC’s “despisement” of PT and Larry Kudlow has been despicable the last four years! They don’t even try to hide it. I keep hoping some of these people in the industry might recognize how great PT’s policies are for our economy and vote for him and Republicans. Or are the majority on Wall Street die hard globalists who are hell-bent on selling America for their personal and professional gain, fanbeav?

President Trump’s policies are good for Main Street (US workers) and Wall Street. I don’t believe anyone on CNBC could care less about Main Street. My advisor has been shorting the market for his personal accounts since President Trump was elected (triple shorts SPXU). His return is now -37%. Luckily he hasn’t done that for his clients!

Hahahahaha! Thank you fanbeav!

Like a rocket ship.

????❤

California Illinois New York Michigan in lockdown!

if they opened even after riots and China Virus, we would’ve been better than January 2020!

Don’t leave out the drag of resistance areas in RED states, like Texas. We have democrat county commissioners of major urban population centers (Dallas, Houston, San Antonio and El Paso) doing their part to crash the economy and crush small business in their jurisdictions. The saving grace here as in many Red States is the “collar counties” with economic engines and populations that match or exceed the those in the big cites proper.

With respect to California and some extent Washington State, the lemmings who vote in the democrats still do not recognize that the high tech economic engines located in their states DO NOT need them to thrive, so the Big Tech owning puppet masters are happy to allow them to destroy themselves and shackle themselves with totalitarian state as well as municipal governments lead by politicians owned by the Tech Puppet Masters.

The green card high tech labor is just happy to be here, while living environment and the totalitarian rule of state and municipal leaders in CA and WA pales in comparison to their former homes.

Big tech are the biggest beneficiaries during this lock down. Amazon Netflix etc. They would prefer the lockdown forever.

Big Tech (especially in Seattle) are the biggest benefactors, is 100% right.. Amazon is hiring 100k new workers for the holidays. Their cloud business is their biggest cash generator. Same for Microsoft. Stay at home workers and shoppers are making these 2 companies (and many others) money at a staggering rate. Probably a good time to buy stock.

Allot of those new hires actually work in off-shore call centers or high tech versions of sweat shops.

Colorado also locked down. Just went back to level 3 yesterday. 25% capacity, etc. Had been at level 2. 50% capacity. New cases……

Boom, recession over……..mic drop.

What ya got now Biden??

Orange Man is responsible for every Covid death was what he said today. So did Governor Cuomo. These people with the help of the lap dog media can lie straight out with any consequences!

Thank you for all you do Sundance

The 2nd Wave of China Virus, with 1,000’s dropping like flies or being shipped to hospitals is the antithesis of the recovery in the business sectors cited. People are buying stuff, working their jobs on-site and making the overt effort to become active outside the home.

The demand is real! We are getting People from around the world pouring in to USA!

who wants hong kong? Paris?? Rome???

Raleigh Durham could double if only they’d fully open!

Make America Great Again, Again – MAGA,A

And that’s with Governor from states like CA, OR, MI, CT, NY, MA, PA, NJ, and few others keeping their state economies forcefully suppressed (each to varying degrees).

You can’t hide the growth though. To back Sundance’s point on the road activity:

My family and I were on a road trip that took us past NYC. It’s a trip we took many times since my in-laws are still south. This particular trip was in 2018. As we drove by I asked them to look at the cityscape and tell me what’s different (I noticed it right away as we came around the bend and you get a glimpse of the city on your left)? What’s different about NYC right now compared to the previous 6 or 7 years of taking this trip?

My one son noticed right away- cranes dad. Cranes on the buildings and new buildings too.

I said yes, cranes on buildings = great economy. And he was (is) right, there were a lot of cranes. Dozens. And they are still there…

I maybe saw two, four at most at any given time during the Obama administration.

sorry, just sharing my little anecdote…I will believe my eyes over what the msm “experts” try to sell me.

I still think small businesses are hurting maybe a bit more than what’s being reported but what’s clear is, the administration’s plan is WORKING. Everything they have been saying the box is being checked. The fact that half the country is stuck on and obsessed with case counts is shameful. And I’m sorry but if you are 25, asymptomatic and test positive that is not a case!!!!!!!!! Wake up America.

This is all fine and dandy, but there’s a lot of work to do. Let me offer some suggestions. First, time to get busy with some serious antitrust. Secondly, how about a small annual wealth tax. Say 75% of assets over ten billion dollars. Every single year. You can print money at the Fed and force it into the markets, but when Jeff Bezos ex-wife gets 30 billion dollars (30,000 million dollars) of it just this year through stock appreciation, we still have a lot of work to do to restore sanity to the system. How about a Marshall Plan for small business? Model it after the Pigford settlement. Take a trillion dollars and lend it out for next to nothing, to start or reinforce small business and start-ups. Bust up the REIT’s. You can’t fix America until you fix housing. If we don’t have in America where young couples can buy a home and start a family easily, the recovery is heading nowhere. We can’t keep importing third worlders to make up for our lack of family formation. Looking for a big landslide next week, and upward and onward, Mr. President. Oh yeah, one more thing. Fix your DOJ.

Love this post Star!

Thank you Rip Tide.

Oh and another record:

“The shortest recession between the mid-1940s and 2007 lasted only six months, from January to July 1980. The two longest recessions during the period lasted 16 months each, one extending from November 1973 to March 1975, and the other from July 1981 to November 1982.”

This kind of information is not making to the American people because we lack a voice.

It’s almost like PTrump has a foresight to see the future. All things he said that is going to happen that came true.

Or, he just understands that the free-market self corrects when left alone. That’s what free market economies do.

Especially an economy that was just starting to take off due to Trump’s policies. We were doing very well before COVID. COVID was not the cause of the economy tanking. COVID was a reason for humans (lawmakers- Democrats) to suppress the market by forcing quarantines and mandating ridiculous protocols.

And since the economy was forcefully suppressed it reversed itself quickly once the shackles were removed.

The only thing in the way now: CA, CT, NY, MA, PA, MI, NJ, and a few others.

We are weekend away from full recovery and more. Find someone who hasn’t voted yet and get them to.

THIS IS WHAT MATTERS!

“V-Shaped Recovery Achieved – Third Quarter GDP Growth a Record Breaking 33.1 Percent…”

Only 33.1 %!

Joe Biden has achieved an astounding Third Quarter Personal Dementia Growth of a record breaking 72% !!!

V for Victory!

https://images.app.goo.gl/EUePfbzcuMb6rn6b7

Fake Commie News:

“Trump lied he said GDP growth would be 37%”

Ummm,,, Fake Commie News correction, PDJT said repeatedly the Atlanta Fed PREDICTED 37%. BTW, 33% is still an amazing number for recovery. Imagine if all those Dim Governors would have opened their states.

And, Trump’s numbers are always adjusted up. Whereas Obama’s had to be adjusted down. So there’s that.

Wait until he wins. It’ll unleash a tsunami of investments, manufacturing, home building (already on fire), restaurants re-opening, innovations flourishing, and optimism off the charts. I FEEL it building and brewing. Look out libs, you’re about to get crushed by awesome American ACTION.

Yup!!!

There was a time not long ago when I would’ve expected the stock market to rally around such great news, but Wall Street has a different agenda than MAGA has.

Wall street hates competition.

One area that is not recovering is Hollywood. Disney owned everything last year, but it is laying of by the tens of thousands right now. Disney has theme parks, movies, cruise ships, it is almost like the virus was specifically targeting them. And it isn’t just COVID, the woke virus is ravaging the industry too. The industry will be down for the next several years probably. .

Doesn’t break my heart one bit. There are some really good young foreign actors and actresses who have been in foreign produced films and combination live-animated films made for TV and screen. They are NOT woke, do not have TDS and seem more interested in working than succumbing to TDS or Wokeness.

Plus all those woke and TDS suffering idiots better wake up because Digital Graphics have gotten pretty darn life like . Live cast members are not necessarily required anymore, as there are now massive digital libraries of anatomic motion available for a staff of computer geeks, good writers and production team to use to make good films.

I have seen it mentioned a couple of times that because Hollywood is holding back their blockbusters because people aren’t going to the theaters, it is giving local producers around the world a chance to promote their own films. While our theaters are going out of business, one film in Japan is breaking Japanese records.

Exactly what they deserve. They are guilty of some very bad things, and some have already paid the price for it. They are largely un-American, and propped up by big purses behind the scenes.

My ground report: Everyone I know has been upgrading vehicles (in case they need an all wheel drive truck to Get Out of Dodge), refinancing to minimize financial drain, or selling to get out of urban areas, stockpiling freezers, food, water, medical supplies, clothing, guns, ammo, generators, you name it, etc. In many cases, people are stockpiling for the long haul, which means they are buying supplies for several years and longer. This has given a huge boost to the otherwise horrible drag of covid on the economy. You can’t even find a freezer right now. You can’t get trades people out to your home for upgrades or fixes (for the purpose of selling or something you bought that needs some work). Real estate has gone bananas here where I live in Idaho. It’s crazy. So, it’s possible that there will be a bit of a lull on consumer goods if Trump should not win because people will be hunkering down after initial panic buying. I believe it’s a Trump landslide next week. However, the Left has promised to burn cities down. So, a lot of folks feel like damned if you do, damned if you don’t, so they’re not taking chances. I believe this year of chaos has affected the American psyche like no other event in the last 3-4 generations. And we can thank utterly insane Nancy Pelosi for the fear mongering, hate, and division we’ve seen. She has the power to calm people down and cooperate with the current Administration – but no, she’s capitalized on people’s fear and made things worse. Despicable! The people who are not in the position financially to prepare are aware of their predicament, and are *very* stressed out – so be kind to your neighbor. I’ve heard, in a lot of Christian groups, “get ready – it’s Revelations”, which I don’t hold to – at least not at the moment. We make jokes in my large extended family. Instead of “What’s for dinner tonight?”, we joke about making “Apocalypse Dinner” which is made from the food pantry.

P.S. The joke out here is: “Due to the ammo shortage, we will not be firing a warning shot.”

Speaking of the ammo shortage and the stock market, I have been following a small publicly traded ammunition company. Early in the month they announced their earnings, and they announced a year over year quarterly gain of 300% and a backlog of $80 million. About two weeks later they announced the backlog was up to $100 million and that they were buying more manufacturing equipment. Today they announced they have almost doubled their capacity.

boom

So, what is the name and symbol of the ammo company? I usually buy Winchester White Box but I can try another American manufacturer!

Ammo Inc. (POWW)

sg,

Where do you live? Just curious where all this serious prepping is occurring.

Thanks!

Rob

This can’t be right? The all-knowing news pundits have been telling us that our current economy is in a shambles. It’s a terrible, no good, unstable, failing hot mess… and it’s all Donald Trump’s fault. Surely they can’t be ALL wrong. “CNN SUX. CNN SUX. CNN SUX. CNN SUX.” Well yes they can be wrong and it’s not by accident.

“Obviously the threat of COVID has been weaponized as an election strategy.”

Did COVID weaponization come as the result of a plan or an election strategy to stop Trump? On one hand we have a Soros company selling a costly treatment for COVID in the United States after discovering shortly after COVID surfaced in China that it treated the virius. The same virus said to be created in a Chinese lab, funded in part by Soros and Obama.

We have all been made aware of the pay offs to prominent members of the Democratic party (i.e., Biden family) from China. So is it such a stretch to believe that China, Soros, Obama and Democratic party leadership have a common interests.

Add to this that Soros continues to fund terrorist organizations like Antifa and far left wing politicians.

Soros is the bag man and his foundations are the strings for the puppet masters.he is not the big cheese in charge, just the action vector into the democrat party. That is why Wall Street and Billionaires puppet masters like democrats. The party is very easy control and finance due to the obedience to the party command structure.

The puppet masters also deal with the GOPe but that is a more expensive proposition as they have to make deals to buy republicans on more an individual basis.

And in a week, even Blue states will start to open … they need the tax revenue they’ve been missing.

I just went to Virginia Beach from Oklahoma City and back to visit my son who is in the Marine Corps. My wife and I could not believe how many semi trucks were on the road. They were EVERYWHERE! From the Carolinas through Tennesee to Little Rock, the road was packed with truckers moving freight. It was unbelieveable.

Is Hillary Clinton on the electoral college of NY? Is this new? My mom just told me ?

Yes, from what I gather it’s some sort of psycho-sexual desire of her’s to be able to cast a vote that will defeat Donald Trump.

For the state of NY? – Perhaps

For our country? – I think not

Funny thing Clivus, cuz she thinks the electoral college shouldn’t exist. Maybe she is leading the way for cronies to all work the EC, what a nightmare that would be. Anyway- it will come up more in the open thread I’m sure ?

Covid-19 was not an accident! China released the virus to destroy President Trump and they almost did. Infecting the rest of the world was just cover for them. Collateral damage!

The uprising in HongKong was the other primary target of the Chinavirus. The CCP was halfway successful; in that they ended HongKong’s independence without a going through with a major military maneuver. Sending troops into the streets would have been a public relations nightmare for Peking.

Oil and gas is going to take longer to recover. Hotels still lagging is evidence of that, since we are so travel intensive. I’ve got millions of dollars of orders sitting on the shelf until after the election. That’s great, but right now the bank is calling me daily wanting me to pay my truck payment, and I’m feeding my kids with credit cards.

I’m pretty sure that come November 4th the shutdowns will magically end and you can return to your job. The money behind the Democrats and the shutdown don’t like losing money needlessly or throwing good money after bad!

V for you

V for me

V will be our VICTORY‼️

PDJT definitely got the policy to weaponize the China Flu panic. At Tampa rally today he played videos of Como, NY Gov. and Nesome, CA Gov. praising White House support during the panic. They praise PDJT when they need aid and bash after they get the aid.

Observations from a Smaller limb.

When calculating GDP a formula is used for chained and unchained calculations. Unchained is also called Current dollar. That is the actual value in today’s spending value (yes oversimplification to make a point). Real GDP in current dollar was up 38% or $1.64 trillion for the 3rd quarter. Furthermore expect unreported revisions upward over the next 9 months.

Cue the Rolcons: ?

When the hospitality industry comes back the impact will be even greater. That won’t be the case if Biden is installed; they’ll continue with their social covid nonsense because they can.

I’ve been a career professional in hospitality for over 35 years. I’m on unemployment for the first time in my life. I have made the best of it but I don’t like it. Tomorrow I have an interview, the first callback I’ve had since July. It will be a 19% cut in pay if I get the job but I will take it if they offer. I live in Oregon, our unemployment rate is 10.6%. President Trump has to win. These crazy democrats are determined to ruin our economy.

I put in a prayer for you. God Bless.

I firmly believe they have suppressed hospitality solely because it is largely the TRUMP’s business.

Recovery, yes, but fueled for now by massive amounts of new debt.

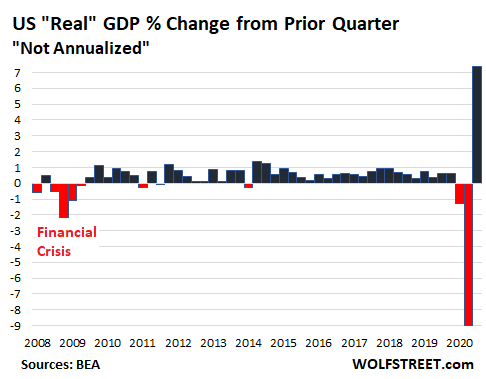

No, GDP Didn’t Jump “33.1%” in Q3, But 7.4%, after Plunging 9% in Q2: Time to Kill “Annualized” Growth Rates.

29 Oct 2020

https://wolfstreet.com/2020/10/29/no-gdp-didnt-jump-33-1-in-q3-but-7-4-after-plunging-9-in-q2-time-to-kill-annualized-growth-rates-stimulus-fattened-imports-were-a-huge-drag-on-gdp/

The spectacular spectacle of an absurd creature called the “annualized” growth rate of GDP appeared again this morning, and the headlines screamed that GDP, adjusted for inflation, surged by a record of “33.1%” in Q3. On the face of it, this would mean that the economy increased by one-third from Q2. But that’s the magic of “annualized” rates. And it’s time to kill them in headline reporting.

That “33.1%” reflected the jump in Q3 from Q2 but roughly multiplied by 4 to produce a theoretical figure of what GDP for the whole year would be if it kept surging four quarters in a row like this. And that’s not going to happen, just like the plunge in Q2 wasn’t actually “31.4%” and wasn’t repeated four quarters in a row. Deeper down in its GDP report this morning, the Bureau of Economic Analysis also reported “not annualized” figures. And not annualized, GDP jumped by a record of 7.4% from Q2, after the record 9.0% plunge in Q2 from Q1:

STILL buying from the CCP rather than punishing it SEVERELY by INDIVIDUALS boycotting “Made in China” as much as possible. “Oh, did you get the latest (HDTV, laptop, smart phone…) THAT YOU DON’T ACTUALLY NEED?”

“Hey, I’ve got a great idea! Let’s move iPhone production to a communist country so we can eventually cash in on their market. They won’t just steal the production technology as they ALWAYS do and make their own via CCP-linked companies, thereby strengthening a mortal enemy of the US.”

Morons deserve what they get:

Apple Plunges After iPhone Sales Miss, China Revenues Plummet, Lack Of Forecast

https://www.zerohedge.com/markets/aapl-plunges-after-iphone-sales-miss-china-revenues-plummet-lack-forecast

Another backfire, their manufactured recession. It hurt a lot of people that now they pretend to care about.

TRUMP should play this at his rallies too. And remember, these are the same people censoring anything positive and pushing and promoting riots in your cities and towns. They lie daily, by the minute, about President TRUMP and his administration, and ignore, withhold and suppress all information on major fraud and corruption on the DIM side.

MSNBC anchor on possible economic downturn : ‘About time we get a recession’

by Nick Givas

19 Aug 2019

https://www.foxnews.com/media/recession-dow-jones-trump-economy-msnbc

https://twitter.com/realDonaldTrump/status/1163169730477395968