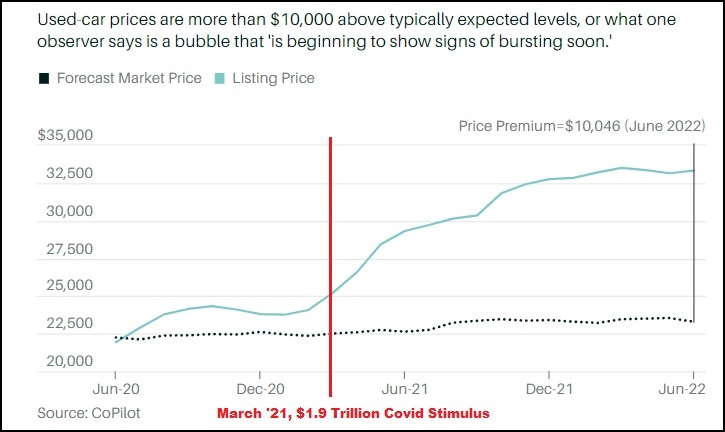

Barrons has an interesting article on an increase in bank auto repossession rates connected to defaults [see here]. Essentially, used car prices have surged significantly and the timeline seems to indicate the temporary covid-19 stimulus spending had a lot to do with the increase in demand.

According to data assembled by CoPilot, used cars are currently priced approximately 10,000 higher than they would be without any pandemic related influence, supply side or demand side. Banks and financial institutions loaned money into the climbing market price. However, the artificially inflated car prices now create a bubble where the liability on the books is significantly higher than the repossessed asset is worth.

A higher rate of auto loans are now defaulting for both sub-prime and prime borrowers (double for both), indicating the former buyers are under financial pressure and can no longer make their car payments. The loan to value ratio was as high as 140% when the banks made the loans, a more traditional or normal ratio is 80%.

The banks have a vested financial interest in limiting the number of repossessed vehicles they allow into the used car auction market in order to keep the book value of the cars as high as possible. Those banks and financial institutions have recently rented more storage space for the vehicles being repossessed.

Barrons – […] Lucky Lopez is a car dealer who has been in the business for about 20 years. In recent meetings with bankers, where he bids on repossessed vehicles before they go to auction, he has noticed some common characteristics of the defaulted loans. Most of the loans on recently repossessed cars originated during 2020 and 2021, whereas origination dates are normally scattered because people fall on hard times at different times; loan-to-value ratios, or the amount financed relative to the value of the vehicle, are around 140%, versus a more normal 80%; and many of the loans were extended to buyers who had temporary pops in income during the pandemic. Those monthly incomes fell—sometimes by half—as pandemic stimulus programs stopped, and now they look even worse on an inflation-adjusted basis and as the prices of basics in particular are climbing. (read more)

Somehow, I would hazzard a guess, if we are to follow recent precedent, that taxpayers are going to end up backstopping the financial institutions when the bubble in this asset class pops. However, that said… the scale of these loan defaults could also foretell a significant slipping in the housing market.

It would seem that Cloward & Piven has been revised to incl inflation as yet another way to implode this economy and destroy our constitutional republic… all by design. I read great post on zerohedge.com that avg mthly car payment = $710 and abt 50% r in a car loan they can’t afford, while voluntary repos are exploding. Will b great time to buy a car in abt 12mths when prices will b forced down.

As Sundance hinted, we will be bailing out the banks on this, one way or another. Probably subsidizing EVs at the same time.

They want us out of gasoline cars. At any cost – to us.

We’ve bailed out the banks in the past…..

and we should not ever. Capitalism fails if businesses making bad decisions are not allowed to go under. Thank you moron Scrub for setting that precedent on steroids in 2008.

One way or the other, I’m keeping my fossil fueled vehicles. The time for wind and solar has come and gone. The great reset will fail eventually…..all planned economies eventually do.

Pennies on the dollar. If there is a dollar.

“r” is not a word. What’d you save, two whole keystrokes? “ur” not texting.

Just waiting for the crash so I can take my pick at a huge discount.

We couldn’t bring in new employees for well over a year. They wouldn’t show up for the interview. They wouldn’t take the job. They would take the job then never show up. They would show up, work for a week and never return. Then about 2 or 3 months ago, we hired 5 people (expecting only 2 or 3 to show up, and all of them to be gone within the week). They all came in; all but 1 are still on the job. The free money has run out, and people have to actually work now, in my strongly Republican state at least.

I was laid off in 4/2020. My corporate employer decided to downsize. Took my unemployment and when it was up, My husband and I realized that we were able to live within our means with a one pay check family. So I decided that I was not going back to work. I was done with the rude public, the shitty bosses, and the crappy pay. Sometimes it has nothing to do with the free money.

Returning to a simpler and freer life. Well done!

That is the plan. Urban corridors. The Great Green Death March.

Screw the banks, charging high interest for loans and paying .14 on savings accounts. Thieves

Where are you getting .14%. I need to go there.

It is very simple. You want to buy something and you are willing to make the required payments. Make the payments to your own Bank account and when it is enough to pay for what you want pay cash and you incur no debt.

I have been doing that all my life and I have everything I want just like everyone else, with the exception of debt. I have zero sympathy for those strapped up their ass with personal debt.

I just deleted a detailed similar post Fangdog!

Now I can “like” yours.

My sentiments exactly.

Don’t know about you but none of this is shocking me one iota!

I agree it is not a shock at all. I drive around my neighborhood and everyone has “toys” in their garage and up to their eyeballs in debt. I use my credit card for convenience only.

I had a neighbor who was up to his eyeballs. I explained how to become debt free. It took him 18 months and he was golden. He thanks me every time I see him. I don’t know why more people don’t listen to Ramsey?

He is a lifesaver! So happy for your friend!

I tell most young folks “You never know how much money you make, until you stop paying someone 18% interest.

Albert Einstein once commented the best invention of man was “compound interest.” If you use it for yourself, that is great, if you allow the credit card companies to use it against you, it takes it’s toll on your spirit eventually.

I gave Dave’s first book to two young men graduating college. I guess they could read, but not follow directions. Unfortunately both buried themselves in debt until their late 30’s.

Or heed the sage advice of Poor Richard? Oh, that’s right…it can’t be relevant if it’s from some ancient playwright and repeated by a Founding Fogie from centuries ago!

“Neither a borrower nor a lender be”

It’s easy until you have to take a loan to pay rent. There is this middle ground between “making it” and “in flux” where things simply aren’t so simple. If you didn’t have the ability to build up wealth when things were good, you’re pretty much stuck in that debt-debt free limbo all of the time. Every company wants to hire you, but none want to pay what you’re really worth compared to costs of living. It’s really nuts right now.

It is an injustice but all of us have to suffer right alongside the Libtards who caused all this. None of this would be happening had Trump been in the Oval Office the past two years. In fact, one of his goals was no income tax by the end of his term. What do you think the price of gas would be right now?

There would be no war in Ukraine. Hillary and Biden would be in jail about now along with crooked democrats and crooked Rinos.

America helped throw a coup in the Ukraine in 2014 in which we helped the neo Nazis gain power. from 2014 onwards we have been giving 200-500 million dollars a year in military aid yearly and have been provoking and planning this war since.

I agree trump less likely to have continued these policies and he kept us out of wars but reality is that war mongering in the Ukraine didn’t stop when trump president. our deep state is all powerful

I told my kids at a young age that education was the key to the door. However, they would never have made it without help from me. I made sure in my younger days that I would be in the position to help them. However, I feel lady luck helped me achieve my goals in some ways. Both my kids are engineers and working at jobs paying 6 figures. I am retired with very little debt. Oh, I payed their college tuition, so when do I get a refund when the government begins to forgive college debt? I want my 250K back.

What’s sad is all the people who must use their credit cards to by gas to get to work. It will take them years to pay that off.

The only solace anyone can get out of this; Is the Biden voting Libtards have to suffer too.

It wont make any difference when the collapse comes. Also, the credit card companies will pass on the lose to people who pay, much like the IRS and hospitals.

Pay it off. Screw the central bankers. We are all in this together. Stop making credit card payments; because, in reality, there’s nothing the banks can do about it if done enmass.

That does not get paid off, ever. Else they would not have charged it in the first place unless planning to pay it at the end of the cycle.

that’s why I do it. cash back and air miles with a payment made paying in full before the cycle ends.

I use credit cards and pay them off immediately rather than minimum payments. cash back and air miles are basically free since I would have got whatever anyway and instead I used a cc and pay it off immediately.

People have been conditioned to believe that debt is normal and expected, and that “building credit” is important, but the “buy now, pay later” mentality has ruined the lives of so many people. Remember, you don’t manage debt, it manages you, and that’s exactly how the lenders want it.

Bottom line: avoid debt like your life depends on it, because it does.

That’s a proven strategy for financial independence.

Until your currency goes to sh@t.

Then you don’t leave your $$ in the bank, you buy things to protect against inflation and bank/government seizures.

You seem to have forgotten that the government shut down many of our businesses under color of law and some of us, myself included, sold off business assets to put food on the table and take care of bills that our business normally handled without issue.

They started this. Not us. And are continuing it with their monetary policies. If you want to rag on people who are suffering, go right ahead. I won’t mourn your death. You made the statement ‘I have zero sympathy’. Well right back atcha pal.

Out of curiosity, did you run your business with zero debt and an emergency fund to get you through the lean times? Because if you didn’t, that’s on you.

He is screwed because he screwed himself.

I was referring to “personal;” finances and not business finances…. There is a huge difference.

Personal and business finances are different in some ways, but the same in others. It is possible to run a cash-based business that doesn’t rely on debt to keep itself going from one year to the next. I know of too many business owners who make purchases based on what they expect to make in profit in the coming year and then get themselves into trouble when those expected profits don’t materialize. It’s the same attitude people have when managing their personal finances. They look at their monthly paycheck, say, “Eh, I can afford to pay $100 a month on my credit card for the next year,” but then their hours get cut, or they lose their job, and they suddenly find themselves with debt they can’t pay that gets bigger every month because of interest.

The secret to financial freedom is surprisingly simple: 1) Keep an emergency fund; 2) Spend less than you earn; 3) Avoid debt like your life depends on it.

Bowering money can be a great tool for running your business. One thing borrowed money is tax-free. However, you have to exercise the same discipline and prudent rules as though it was your own money.

ONE OF THE FEW THINGS I BOUGHT OVER MY LIFE, THE ADULT PART THAT IS. MY 87 NISSAN HARD BODY. OVER 295K. MISSES, DIESELING BAD, SMOKY. TOP SPEED 65. I HAVE OFFERS OFTEN. NO WAY I SELL IT.

WITH IT MISSING, DIESELING. I FEEL THAT SOMEHOW I AM POURING SALT INTO AOC’S CLIMATE CONTROL MINDSET.

WHEN I AM ON THE INTERSTATE. CARS PASSING ME LOOKING, SPEEDING UP. WASTING GAS CUZ THEY PIZZED WHO IS GETTING LAST LAFF!!.

My father had a used Nissan Hard Body when he died in 2007. I used it for awhile until my brother needed it. When he was through driving it, my mother sold it to my sister for $2,000. After a couple of years, my sister sold it to her son for $2,000. A couple of years later, he sold it back to her for $2,000. Three years ago, I asked if she would take $2,000 for it. No way. She still drives it when she needs a little truck. It has over 200k miles on it. Runs fine.

I had to buy a different truck. I bought a used 2015 Nissan Frontier. It is the model that replaced the Hard Body. Good truck and handy to have.

So our banks are staring at the abyss just as the Russians are poised to choke out Europe’s economy (read banks,) the collapse of which will bring down our banks.

Are we so different from Sri Lanka?

Yes. Our fall will have much larger global repercussions.

Some good thoughts here on how we HAVE to be (and can be) different from Sri Lanka, for our own sake and also for the rest of the world. https://conservative-daily.com/cd-livestream/what-happens-when-the-people-are-fed-up-uprisings-around-the-world

The Russians know that it is not about choking the life out of your opponent especially if they are useful to your ends. It’s about teaching them their place in the order of things. This is the lesson Putin has prepared for Biden, Zelinsky and the West.

I make my payments. All of them. But for the second time in my life, now making a salary well into 6 figures (finally), I’m on the bubble. It’s like I am in my 20s again. Worked hard, kept my nose clean, moved up the salary ladder as it were. And it feels like being back to square one. I can’t even imagine what it’s like making what I did 10 years ago. Couldn’t even make rent with what things cost now with the piddly 60k I made back then.

I’m leaving the DC area finally and moving to the Midwest, just because cost of living is terrible here. And what do I find? Renting a smaller place costs near as much as here now…in the middle of nowhere not in a city. Totally unheard of a few years ago. Movers? Forget it. easily 10k. Literally started at 2k and started adding $1000 for each peice of furniture. Like $1k for a couch we got at Big Lots for like $200. To just put it in a truck and then take it off again.

Wanted to try Penske instead of UHaul because UHaul tried to screw us bad last time and UHaul is $1k for a truck here. Looked at Penske…$4k for a truck. Are you kidding me? I asked the guy twice if that was buying some old fleet vehicle, and he said “no just rent it for 2 days”. 4 grand? Insane.

If we aren’t headed for something, I dunno what is going on then. Something is definitely going downhill fast.

Yes, you got a treasonous totalitarian government led by a criminal imbecilic surrounded by nothing but crooks and incompetents. There is going to be a total disaster before the people actually learn a lesson….. Libtards and I don’t care if they sit at your kitchen table. They are your enemy.

My friend, while you and I likely agree a lot on political views and views in general, it is far more complicated than that. This is not merely ideology at work. This is the wheels coming off a machine that has been plugging down the track for generations. I don’t think what is coming was even predicted, much less designed, by the powers behind causing it.

If things truly go where they seem to be going, those who caused it will be eaten alive. I doubt that was their plan. You can push all kinds of political chicanery, but once you make people starve and homeless, you aren’t getting out a live if history has anything to say about it.

Of course, it was not their plan. It is why they are doing and have been doing everything possible to get rid of Trump. Trump studied this for years and years before he came down the escalator. Trump hoped someone else would drain the swamp so he wouldn’t have to do it.

This is one big giant “sting” operation, the biggest in history. The “Bad Guys” are ultimately doomed. They are cornered cats and fighting for their lives. If it means America goes down with them, so be it from their point of view. What is anything they are doing that is good for America?

The bad guys are cool enough to be cats. They are cornered traitors fighting for their lives.

I hope you get to decompress now that you have relocated. It may take a while.

Breathe the air, go outside and look at the stars. Listen to the crickets and accept that you have found the real world. You are in a better place.

I had a couple of friends with pickup trucks last time. Cost? 2 hamburgers fries and coke. We had fun and laffed at each others old backs. Lol

When I moved from Ohio to DC, I had a ton of friends and it cost some pizza and beer. I have no friends in DC. You don’t make friends here. You make “contacts”. Horrible place.

I lasted six months in DC..moved back home broke. It took me five years to get back on my feet. I was young and stupid. You are correct..it’s a horrible place.

If I were me, I’d buy a used cube truck and resell it after my move.

Look at the market for vehicles right now…

I do … constantly. I’m always looking at 1 ton E350 Ford Supervans and Dodge B350 Maxivans. Where I look always has ads for those vans with cubes and also the next bigger models. I bought a ’91 B350 exactly a year ago with 87K for $1,500. Other than the doors , it is practically rust free. No matter.

The theory is to look around for the best deal you can find, buy it, use it and then re-sell it. If the used truck market makes you pay more than you wanted up front then you’ll most likely get back most or all of what you paid. This high priced used car market will be here longer than the time it takes for you to move.

There has been an ongoing scam now for about 20 years. Movers won’t deliver your stuff unless you agree to pay more than what you agreed to. You might want to research this online and you might want to consider hiring your own movers, “Hire” as in NO moving company involved.

how about playing their game against them….. buy a cube truck from a dealer. put a down payment of about half of the cost of hireing a mover/renting a uhaul. make your move, then let the dealer/bank repo the truck.. you take a credit hit, but can easily make that back with the lower cost of living in your new abode.

Here’s a link to the same auction I posted above a couple of minutes ago. You might find a vehicle worth buying. There is another auction to be posted soon.

https://www.nuttauction.com/auctions/4364-ONLINE-ONLY-Bus-and-Vehicle-Auction?page=1&search=&sort=&lotsTotal=11&pageSize=25

Keln, when I saw the notice for this auction in my email, I thought of you. Poke around and see if you might wish to bid. The physical site is outside of Texarkana, Texas.

For example: https://www.nuttauction.com/auctions/4364/lot/1-2017-Ford-E-450-StarCraft

Great idea. Afterwards, turn it into a tiny home and rent it out. Propane tanks. PortaPotty, maybe solar for electrical.

I’m a floor covering installer so I need a long van. I work for all types of people and for a few slum lords. I got a lot of great stories ….

There were times in my younger days when a van that was 6 foot wide inside and 13 foot long behind the engine cover would have seemed like a mansion. My current Dodge B350 MaxiVan is this size! It is not a cube van, just a regular van. It used to belong to a day care.

Go to NC and rent a Penske. If you are lucky maybe find someone needing cargo moved up I95. Still bet you can cut the price in half.

https://www.upack.com/

this is what we did. I was super suspicious about everyone of these companies.

These guy’s not only were honest but they got to our new home a day earlier.

really good job.

If you’re talking about a one way rental from DC to the Midwest they charge that much because nobody wants to move from the Midwest to DC so they don’t get their truck back right away. I bet the reverse trip would cost 1/2 what you need to pay. Same with moving out of New York or California. High demand from people wanting to get out, low demand for the reverse trip.

Penske is more for businesses to rent whereas U-Haul for is focused more on individuals

I thought joe byedone resembled a used car salesman.

People getting “free” money often make very poor financial decisions.

Look at lottery winners…Usually broke 2 years later.

Star athletes often find themselves in the same trouble.

REPO, REPO man. I’ve got to be a REPO man.

REPO, REPO man. I’ve got to be a REPO.

Well something has to give. Ford claims their truck sales are up? To who exactly? The last time gas was this expensive the entire truck market crashed. So much so, it took “Cash for Clunkers” to clean it up. With F-150’s costing up to 80 thousand dollars today, there is no clunkers bail out this time around. So people are losing them instead. The same thing the would’ve happened the last time. And where do you get loans for 140% of the value of the car? I’ve never seen that since the Community Reinvestment act for homes. You remember, the act that wiped out the entire housing industry back in 08?

In another year we will also see a glut of off-lease vehicles hitting the market with artificially high residuals.

The auto industry knows what’s coming.

And it ain’t pretty.

Soon these repressed reports will hit the public in the face and then we will have some real peaceful protests.

Can they hold this info from the public until after the election?

Indeed, car repo’s are an omen for the housing market in the near future. Houses are being sold to people who cannot afford them in this super heated housing market. History repeating itself once more, reminds of the Barney Frank housing collapse of 15 years or so ago.

This is our opportunity, take the battle to the financial institutions, drain all assets from them, stop paying debt, task their soldiers, defend property, go to the mat on all fronts. Time to inflict pain and suffering on the soldiers of the devil. They made their choice. I don’t mourn their deaths. They are the enemy.

However, what Americans will really do, being their greedy self involved selves, will be to seek to capitilize and increase their own wealth on the backs of other’s suffering. That’s the American way and who and what we are. Watch and see how the discussion goes. Patriots are ignored, destroyed or killed while others smile and enjoy their profits. America.

The sand in the machinery is a nice thought but how many are really throwing sand in the machinery? Doing what needs to be done? Following the convoys has really opened my eyes to who and what Americans really are, the cross section of the country. I understand better why 3% fought the Revolution while 97% stood by with many profiting from it. I doubt even 3% would stand up today. Profit is king. All worship the king.

There all ready is a recession numb nuts Biteme you old fool and liar child molester.We should just call this old foolliar Chester .Chester the molester nice ring I say.

The tell is Lowes garden market. Usually sold out to a few sickly plants by June 15 at the latest. This year it’s almost fully stocked in mid July… Wonder why no one is buying flowers???

Maybe they are selling a lot of flowers and continue to restock.

Are people being like me and buying edible plants instead? Flowers are for some time when I can afford to think about beauty.

Unemployment bought those cars. Fabulous. I don’t fault anyone who has had to use unemployment, just doesn’t seem like a wise time to be getting loans. How does that loan even get approved?

Once Putin uses a Nuke because we have him pushed into a corner all this nonsense of man-made global warming will be gone

The sooner it is burned down, the sooner we can rebuild…..

I’m going to add the insurance companies to this mix. How long until insurance rates go up 50% to cover a used vehicle bought at 20 thousand which is now valued at 30 thousand?

Then there’s going to be a huge jump in adjustment settlements from fender benders if parts to repair are even available.

1) as the article says, it’s an income bubble from 2020/2021 ppp, which means only a subset of folks

2) car prices remain high; won’t pop or collapse although may ease

3) none of this will cause or exaggerate a recession

We are already in a recession, inflation is rising and causing issue for the average consumer. Auto loans are just one indicator with more trouble ahead.

Lets Go brandon !!!