Well, well, well…. though financial media will say this is remarkably unexpected, it is something CTH specifically predicted we would see – and it is happening exactly on the timeline CTH anticipated.

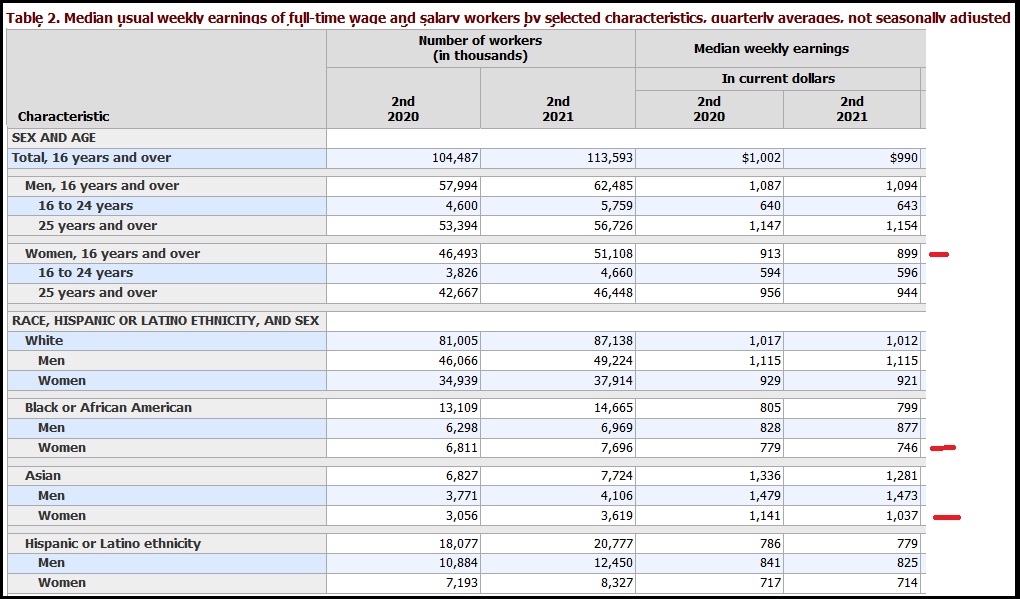

The Bureau of Labor Statistics releases the second quarter national wage rate data today {BLS DATA HERE}. U.S. wages DECLINED 1.2% in the second quarter of 2021 compared to last year. When reviewing the data [Table 2], look at the negative impact to women, specifically Black and Asian women:

TOP LINE – Combine a 1.2% decline in earned wages with a 5.4% overall inflation rate recently reported {Go Deep}, and what you get is a 6.6% drop in real income amid the working class. That, my friends, is exactly what we said should be expected. That is also why the JoeBama administration needs to pump more money into the system (human infrastructure spending) in order to stop people from realizing just how bad it is.

You cannot have declining wages and massive inflation and expect the middle-class to survive. Additionally, when I said six weeks ago that we had just passed peak home value, this is another data point to bolster that prediction. We are in a plateau period on macro-level real home values, from this point they start dropping. You cannot have near double digit drops in real income and simultaneously expect people to afford high mortgages. It just doesn’t happen.

The declining wage rates, and the more substantive drop in real wage rates due to massive inflation, are specifically hitting the lower tier of the working class harder. Yet despite this, Biden is intent on importing even more economic migrants to put even more downward pressure on wages for the working class.

The declining wage rates, and the more substantive drop in real wage rates due to massive inflation, are specifically hitting the lower tier of the working class harder. Yet despite this, Biden is intent on importing even more economic migrants to put even more downward pressure on wages for the working class.

These are very real outcomes of policy. Working class Blacks and Latinos will feel this even more, yet this is the special interest group that Democrats claim to support. The reality is exactly opposite from the narrative sold by the Biden administration.

The Democrats know this. These outcomes are not accidental; they are a feature not a flaw in their policy. This is why they need to keep spending to retain the ruse.

There’s no way around this. Despite the pundit and financial class selling a counter-narrative, home prices will crash and unemployment will go up. I know this is directly against the current talking points, but the statistical reality is clear. CTH was the first place who said two months ago that home sales will plummet, that is starting to happen right now. There’s no way for it not to happen, the big picture tells us why.

May 2021 – “It will be very interesting to watch how the housing market responds over the next few months. If the trendline continues we should see a considerable softening in home sales, again depending on region, as the inflation hits the working class.” Imagine what happens when they stop pumping money into the economy.

“You will own nothing and be happy” Says it all really.

Saturday afternoon they pick the lice out of each others hair so when they wear their Sunday whites the next day they don’t have little black things crawling around on their shirts. They have nothing and they are happy!

Don’t forget, they are lending massive to sub-prime borrowers… AGAIN!

Some lenders are also extending more credit to people with low credit scores. Some 1.4 million general-purpose credit cards were given to subprime borrowers in March, up 28% from last year and 25% from 2019.

Roughly 602,000 subprime auto loans and leases were originated in March, up 31% from a year before. Balances on those auto loans and leases totaled $11.7 billion, the highest on record.

https://mishtalk.com/economics/the-consumer-is-back-well-yes-and-no-and-misleadingly-so

Yet interest rates on credit cards have never been higher.

Pay off your credit card debt and use cash when able.

Don’t charge something to a credit card that you can’t pay off in full at the end of the month.

Bingo – treat it as a utility bill – you do not pay part of it EVER

Indeed, we got out of revolving debt several years ago on our own.

But now have some big medical bills because Obamacare happened and it still hasn’t been repealed. Insurance is still crap and the plan given gets worse each year. I swear, we are paying for all those illegals that don’t pay a damn dime, it has to come from somewhere. Hoping to work out a payment plan for the bills. Can’t squeeze blood from a turnip. I can’t tell you also how many medical procedures we keep kicking down the road until we have some money. One thing, braces for the kids, and one is now graduated. Haven’t had a vacation in years. Things felt like they were lightening up under President Trump, then the pandemic happened, and then this nightmare junta.

We are in the same boat. Medical debt is drowning us.

One minor ER trip, you are in debt for a year at least. Can’t believe the costs. But it was unavoidable, unfortunately.

I hope you can figure out a way to crawl out of it, too.

Small tip from sister in law who worked for doctor’s office. Offer to pay almost anything direct to them and they will usually take it because it saves them cost of collecting, paperwork, bad debt.

Just walk away. Most places will work out a plan. They can also lower the total if you were overcharged and they can write it off on their taxes.

It takes nerve because they will try to bully you into paying the full amount but if you are spending all your money on debt then you don’t have a life anyway. Let them try to collect. Many times the cost of collecting discourages the debt owner from continuing to pursue the debt and will offer a deal. It goes counter to what you were taught to pay your debts but sometimes you just can’t keep it up.

Exactly. Use credit cards as a buffer from your bank account.

Never use your debit card online because that’s connected to your checking account.

Charge the purchase to your cc then within the same billing cycle payoff the full cc balance. Zero interest.

And use a cc /ID fraud alert service like LifeLock or equivalent to protect those cards.

I’ve had lifelock for years, been paying 20 bucks a month for them to basically tell me about my expensive rent payment a week after it happens. But it is good to have I suppose. An even better step I would recommend is to place a security freeze with the credit bureaus and ChexSystems, that way no one can inquire into your credit or debit history, and no one can open a credit card or checking/savings account in your name without your consent. Just be aware that if you want to open a new account or take out a loan, you have to contact the appropriate agency to lift the freeze first.

That’s ok, and each of us decides what we want to be protected and how much we are willing to pay for that protection. LL or an equivalent service can protect you on a far broader level covering far more aspects of your financial accounts and identities. I subscribe to their highest level of protection (“ultimate”) which does cost a bit more, but accordingly provides an amazingly comprehensive level of coverage.

As usual, caveat emptor….

If the .gov would not have made the social security number that was never going to be an identifier, no one would have to purchase protection from what the gov did to you. I will not pay life lock or anyone. Same with medical thanks to Oballah now your records are online and can be easily hacked. They can prove to me I openend the account there still is a responsibiblty from card issuers. Or they will wait a long time for their money.

You ultimately can’t fight government having access to your medical records if you go on medicare.

Which also translates to buying locally and ditching the big corporations. Yeh!!!

Before cash is no longer accepted. It’s coming. Wonder what the next crisis will be to force everyone to pay w digital.?

I have a suggestion. Remember when the hacking tools conjured by the NSA where let out into the wild? Ever since then we have had a series of ‘hacks’ that compromised infrastructure both small and large.

I dug into the recent hack on Colonial Pipeline and discovered that the actual flow in the Pipeline wasn’t stopped by the hack … only the ability of its owners to charge it’s customers so it was closed. Remember that when Colonial payed the ransome the FIB ended up with it?

As you stated, the FED is looking to convert our current monetary system into a fully digital dollar in the future. One way to do that suddenly would be to have a cyber attack on the banking system.

The FED will have the solution and people will beg for a digital crypto replacement.

And the reason for a no cash economy is control. they can see what everyone is doing and flag that which they want to examine more closely. They also can cut anyone off from there money in an instant.

Remember those dystopian movies where the hero(ine) becomes a non person because all their information has been modified or removed?

That’s what is coming. They won’t arrest anyone anymore. Prisons cost money. Better to just make it difficult if not impossible for those they wish to control or kill to buy food, gas, shelter, information (internet). With all that gone people won’t have time to try and march on the capitol.

If you’re already on SS and/or medicare/medicaid then you are already experiencing this. You are not getting all the health care you need. You are getting just enough so you don’t complain. I know there are therapies out there for some of my conditions but the drs won’t prescribe them or tell me about them because then they would get in trouble for sending a low paying patient to these places that do those tests.

But since they don’t tell you you don’t ask and your misery just continues when they could make your life better but wouldn’t get paid for it. They have to take basic patients because of the law but they don’t have to prescribe all the tests and procedures that would help you if you’re not at risk of dying without them.

See how that works. We’re just Government finance nodes to the health care providers. Only those wealthy enough to pay cash or have a good medical plan get the full treatment.

And all that’s because Government took over the health care system.

Gee what more could they ruin?

The China virus lockdown on medical care so that you could only get emergency care OR virus care was just a dress rehearsal, IMHAO.

As an example, Kaiser Permanente shut down all of its satellite offices throughout Colorado except for 4 major hospital & medical offices. You could not get appointments with your primary dr., lab work, xrays, diagnostic care or elective surgeries like hip/knee replacements. How many Americans died from non-care? And, of course, classified as China virus deaths….

It was 6 weeks to 4 months to do anything & that backlog has continued even with the re-opening of satellite offices.

But Kaiser got their monthly premium out of my SS like clockwork.

That’s the same thing fannie and freddie did last time.

These chumps never learn. That has been tried many times before with massive failures.

reparations

Yes, you hit the nail on the head. The government will assume the bad debt which means middle class citizens will be responsible once again. Last time the banks paid back the loan/ bailout dollars, the obama collectively gave this money to his pet activist groups. True

Correction…gment will assume bad debt on a certain class of people…

Don’t worry, Wall Street will once again financially engineer their way out of this! What’s a tranche between friends? Ignore those bank models that say home prices can never go down. We’ll be bailing them out again.

That’s the problem they won’t be able to with severe Inflation. You young people don’t get cavalier like this is just the way things go. This could be a major problem that brings this Civilization to its knees and is thrown entirely in your lap. STOP PRINTING MONEY.

Dodd Frank Act has a provision in it that says the taxpayer will not bailout the banks this time around. The solution is for the people who have accounts at the bankrupt banks lose their monies to the bank.

Pull your cash.

Don’t think they will do this? This was already tested in Cyprus. They took foreign monies first, then savings from citizens.

If they do this, how much will you lose? How much will they “freeze” on you until some unknown time in the future??

Consider and prepare.

IMO, this is not fear-mongering.

If you are only banking with a local or independent credit union, you are probably much safer from this potential money grab than those banking with national retail banks.

Talk with your credit union manager about this. Get their feedback.

You collapse an economy while manufacturing inflation and you’ve got serious problems. See these people are stupid, don’t ever forget that. It’s that aspect of them that believes their own bullshit.

The fiat money printing and borrowing is part of the plan. It was already growing out of control, then the plandemic started execution phase, which created the pretext to throw all restraint out and add trillions more in less than a year because “covid emergency”.

Everything is now blamed on covid, while the corrupt profit from the money printing and borrowing. (No coincidence that those are the ones steering the money printing and borrowing, and those they essentially bribe.)

The plan was conceived to turn the intractable US problems including declining industry, education and skills, middle class, and increasing debt, into opportunity: The goal is a (1) a culled herd with (2) increased supply of bottom tier labor driving all labor costs down and individual performance up by fear of job loss, followed by (3) extreme societal distress justifying imposition of totalitarian government. All for the benefit of the 1%. Remember: This group uses the “human biosphere” for their own power, they want a more efficient biosphere under tighter control, all of these things point to that end.

The bioweapons (virus and shots) are designed to yield (1) and (3). The flood of people coming over the southern borders serves (2). It is all part of the same Plan.

The elites have always been all about turning problems into opportunities. This is no different, to them.

Heard on the street, hard to say if I agree:

The psaki statements of the last couple days, and the Politico “news” about “biden-allied entities including the DNC egaging with SMS carriers”, about the government overtly manipulating and censoring private communications and expression using third-parties, are early signs of (3) on the horizon.

The “covid deaths” are used as the excuse for the increasingly audacious in-your-face censoring and propaganda. All part of the plan. Get the populace used to the idea as it is ramped up. After all, it’s for our own good, right?

(In using the justification of encroachment on liberty, “to prevent covid deaths”, they think we have forgotten this: “Give me liberty, or give me death”.)

Just wait until the deaths and morbidities increase substantially, due to “another variant” covid (possibly released on schedule from Wuhan labs, still operating), or due to long-term adverse effects of the “vaccines” (still unknown after only 7 months of the EUA de facto experimental trial). Or, most likely, both. (The “vaccines” coverage is about to go to ~100%, with the coming FDA approval and subsequent blanket “vaccine” mandates, despite data showing poor efficacy and great harm by the “vaccines” for this “existential hazard” covid with its flu-like survival rate of 99.9%, all of these things point to something much more nefarious than simply greed as the underlying driver.)

Combine with severe economic distress from hollowed out economy forced into slow-motion since early 2020, plus accelerating unsustainable debt and inflation due to borrowing and printing “because of covid emergency”, which will worsen to near-collapse with the coming mass deaths and morbidities.

Yield: Totalitarian control of a population culled of the weaker specimens. And the beauty of the “public health emergency” is that it also justifies suspension of civil liberties, this is exactly what has been going on since early 2020, and this will be used with the coming complete totalitarian control “because of combined public health emergency and economic emergency”.

This plan is still in the early stages of execution.

God help us if this is what is really happening. I am trying to think of a Plan B, but cannot come up with one.

What could possibly go wrong? /s

<“You will own nothing and be happy” Says it all really.>

Biden fiddles…while R F Burns 🙂

It’s called “deindustrialization”. The deliberate intent is to make us all poorer. Only by consuming less can be become more sustainable so that we can save the planet. It’s all a load of BS of course. The real purpose is to replace our liberties and freedoms with a one-party a totalitarian state. What a bunch of low-life scumbags.

Indeed.

The Bourgeois must be eliminated one job at a time if need be, in order to build that Marxist utopia.

The inner party members need to have the means to maintain their foreign auto collections at each of their three dachas so they can see to the business of taking care of the people you understand.

We do make a lot of trash…I see it on garbage day, overflowing trash cans. The answer is repurpose. Garage Sales, Thrift stores.

Modern packaging is responsible for much of the excess trash today.

Various types of plastic Foam, plastic containers, plastic wraps…. all have been very convenient for sellers and consumers but the materials have created a massive global problem that did not exist 50 years ago, despite the similar high level of consumption back then.

Food containers are probably number 1 among the causes of current excess trash.

The second reason is the consumption of cheap Chinese products that do not last and are routinely discarded and replaced.

Table fan stopped working? Toss it in the trash and buy a new one from Walmart for $15. Done. But in the Old days- unscrew the housing and replace a switch or rewind the motor armature if necessary. (My grandmother showed me how to do it; the local hardware store carried spools of enameled copper wire for just such an application. ). Result- a Westinghouse 12” fan bought in 1935 was still working fine in 1960.

Same goes for electronic entertainment and communication devices. Phones, radios, record players. Etc.

I don’t blame packaging, I blame government regulation. Pretty much all of those plastics are recyclable. But here in my corner of the Greater People’s Republic of Montgomery County located in the Lesser People’s Republic of Maryland, even though recycling is mandatory, you CAN’T put most of those recyclables in the recycling bin (especially the plastic bags they charge 5 cents each for to “reduce bird deaths caused by them swallowing the bags”). I recall someone from McDonald’s being interviewed about their trash rates. Turns out most local governments prohibit treating their recyclables as recyclable because it has touch food. Now it has to be treated as trash and go to the dump.

I hate the packaging for other reasons like the clamshell that you almost can’t open without gashing yourself on a sharp edge when you open along the perforated edge. Or the fact that they practically require a power shears to open. But you gotta cut down on theft from the factory floor somehow, right?

Oh government regulations caused the switch from waxed paper and cardboard packaging in fast food, then I guess I’d agree with you. But is that what occurred? I wasn’t aware that food sellers were forced to switch to plastic.

I totally agree with everything you described about plastic food containers and bags.

My wife loved her “designer” shopping bags I bought for her about 4 years ago. She stopped bringing home plastic bags; many stores had started charging for those plastic bags to discourage use.

But then the Plandemic hit and frightened, ill-informed stores and local government outlawed using personal shopping bags in the stores. Evil fools. Back to using the plant polluting plastic bags.

not “plant” polluting…. planet polluting. (spellcheck strikes again)

Chopped onions sold in one of those clear plastic clam shells. Ridiculous. I have asked my city council why they can’t force sellers of this stuff to take responsibility. How about all stores forced to have bins out front to recycle or take back all the junk they sell? How long do you think they will keep selling it?

Voting machines used once, done, throw them out.

Well, THAT’S a definite!

Those pieces of garbage technology are Untrustworthy Fraudulent Vote Manipulation Machines

It’s all about power.

You give them too much credit. They’re really just a crowd that’s crazy, stupid, and selfish, and can’t admit anything.

California is now planning to introduce a guaranteed income, state-wide. It has the support of both parties. The amount has yet to be determined, maybe $500 a month, maybe $1K, but it will be small. Not enough to rent an apartment, so the government will soon be required to supply (own and distribute) all housing.

Not a good idea to be a government critic if you want a roof over your head.

You know when the crash is happening because everyone will start saying the market is “tapping the brakes” before it will hit the accelerator again. When that seems to not happen, “all signs point to a soft landing”, which means it’s going down hard, soft landings aren’t a thing in asset markets.

The markets have most likely peaked. Why I say this is nobody is buying anything right now, homes and autosales are turning, which will lead to lower prices and soon to be New Deals/ Bargins, that’s when everyone will start cashing out 401k’s etc to buy the deals. I have recommended to everyone I know to cash out now relating to 401k, or roll it into high grade bonds. Take your profits while they exist.

Precious metals? No… I would invest in assets, or businesses (not equities, actual real business as a part owner.) that make a decent monthly return, or stream of income, some industry that you understand.

Not really, say if you cashed out and paid the tax now…. Market crashes you get back in, it will be easy to make your tax loss back. Say for instance I had my friend cash out his Aapl stock around 700 in 2012, he took a tax hit, but he rolled his money into AMZN @235 and is up ~1500 percent since then. A little tax loss is minuscule to a market crash loss, or market gain if invested right.

If you roll your money into the right stocks you can make more. I advised to move money between about 4 stocks since 2012. 2 of them were FB and AMZN … the others were smaller companies. Compound returns after capital gains tax if invested right would have been over 100X ROI in that 9 years, but that was with some of those stockings netting over 100% per annum gains. When you are up say 20X ROI, a 100% per annum gain on that would put you up 40X before tax…. that’s how you can get such good ROI, instead of just leaving it in one stock. It’s just like parlaying at the casino…. (without being at a real casino which I would not recommend.)

You lost me as client right here,no thanks,

“I advised to move money between about 4 stocks since 2012. 2 of them were FB and AMZN”

Well, my advice made one of my close friends who was a Doctor millions of dollars in that time with a total ROI of 100X+

I still remember my other friend from London laughing when I said FB was a Bargain at $18… in 2012 he said it wouldn’t even be a $50 stock… sitting at $341 today for ~19X compound. DO I recommend them now? NO… but they made a shit ton of money off the investments.

I had one billionaire add me on FB, his time on my page was 4 years, his networth rose from $2 billion to $10 billion now. He took some of my advice on stocks, albeit he also played the currency markets and made good returns.

You really are Mister Wright ?

Your doctor friend probably had a boatload of money to invest in the first place… not everyone has that much extra lying around or coming in with every paycheck.

Compound returns work the same compound regardless. If you can’t manage $100, you wouldn’t be able to manage $1 million. I know most people have no money, and there is a good reason for it… they don’t know how to save, they make bad money choices, buying the latest greatest phones, tvs, cars, etc.. My friend was in the military Service, he served and then got his education to be a Doctor. His mom left him a house and a little money. His daily driver was an old used van he paid less than $5000 for… he still drives it to work. (Yes he has a nice BMW in his garage too now.) That’s how he got his start, not much different than most avg. Americans… only he is Smarter and more Frugal.

Yes but you can also time it wrong. Why not just keep AAPL?

Because you get a higher ROI by buying other stocks. You have to churn your investments. Yes you could leave 10-20% in AAPL as a passive investor, but your returns will be better by investing in other industries with more growth potential. There is always a better investment… you just have to time it right.

YES! Phil from Phil’s Gang explains this philosophy. He buys and sells stocks/ETFs long and short. My son buys and sells “things” such as lawn and construction equipment and turns a pretty penny with each sale. Oftentimes he uses the equipment for a period of time to make more money and then sells. Everything was going great before the COVID shutdown. I had given him some cash to invest in some equipment. It took him a year to sell my investment, due to COVID. In the end, I made a 50% return.

Just because a company performed well in the past, does not guarantee future earnings, or something like that…

https://mobilesyrup.com/2021/07/16/xiaomi-surpasses-apple-global-smartphone-market-share/

That’s the way everything is, you have to time it right. Which is why passive investing generally does not work. Politics has a lot to do with investing to. You have to understand where the country/world is headed. If you can see out into the future and play your cards right, that is how you make good returns. One area that might be a good investment would be a Conservative Based Social media company if a Public stock offering came up. I would would put ~5% of my capital in one, if it looked like a fruitful opportunity. (Right now there is none.)

Well, I had about 20 billionaires on my FB before I shut it down, some are worth upwards of 10 billion now. Some were investment managers in NYC, LONDON, etc., so my advice is fairly solid and proven, that being said… I cannot recommend any stocks right now… because most are overvalued. I would recommend investing in some business with someone you know who is trustworthy (and has capital), where profits are capable of being made on a monthly basis. You would be like a managing partner, or just an investor without the management role… if you don’t want to manage it. Find an industry you understand that is profitable and in demand.

I recommended buying stocks since ~2010 to now…. As of now they are mostly overpriced, especially with Biden running our country into the ground. Therefore I would put hard cash to work in local industry around you. Where you can see your cash working and making an honest return, (not in housing related stuff, or companies with big inventories) this done properly will be liking earning dividends without the risk of losing all your capital in the stock market. Keep enough cash liquid that you can inject it into the markets if they do crash. Note they will crash eventually they always do, especially when the housing market rolls over.

I am no investment advisor. I would like to add to Sam’s advice. Phil from Phil’s Gang has a weekly youtube video each Friday discussing the market and its inevitable drop. (yes, he sells a service). However, his market philosophy is to understand how the FED’s actions impact various segments of the market for good or bad and how to mitigate financial risk. He is not a long-term buy-and-hold proponent. Phil is NOT a proponent of 401K plans. He encourages people to take control of their own finances. Just my 2 cents worth.

I have had a diversified pre-tax portfolio of about 10 or 12 mostly index funds along with some cash and a good spread of small, mid, large, growth, value, and bonds, in both domestic and international markets. I rebalance occasionally by selling portions of the winners and buying more of the others. This has returned an average 15% over the last 6 years with a -2.3% low and +28% high.

With the weak dollar I am expecting foreign stocks to do better while countering any fall in US stocks.

I am not a professional and only spend 10-20 hours a year on this. The key is to keep your costs low and cover all the markets as best you can so that if one goes belly up, another will thrive. I don’t look to maximize return but simply do better than the 4 to 6% that professional advisors aspire to.

You don’t need to cash it all out. Depending on your investment , you won’t lose everything if the market crashes.

So, according to your tax rate, take out what won’t move you into a much higher tax bracket. If you aren’t sure, take out 20 percent as profit for yourself, and let the rest ride in your 401k.

You will have extra cash on hand, slightly higher taxes and if you have a diverse portfolio, your whole 401k won’t suffer too much. You don’t need all the money right now anyway, right?

Or, just roll it over into an IRA money market fund. The money is safe there and you don’t pay taxes because it is still in a retirement fund. It won’t make money or lose money, like a bank account. Easy to do.

It is hard to make money in PM. You have your transaction cost each way and you are taxed at a collectable rate. If it kept even with inflation you would lose money after taxes. You are taxed gain in dollars so you could have a loss in purchasing power and still have to pay taxes.

You will never make a decent return on PM, with Rothchilds pricing the metal in London.

PMs have never been a primary investment but a HEDGE against inflation…their price will typically track CPI numbers

An IRA money market fund will hold the money for you without any tax penalty if you do a rollover. Your money can just sit there and be safe and preserve your profits. You also have the option to invest it in whatever you choose at some future time ..when you decide what to do.

It depends on how aggressive you want to be with your money. Are you well situated? Do you own your home and have enough to live on without your 401K money? If you are retired the 401 K money is a nest egg for an emergency, but you should use it to make your life better too.

You might want to spend some of it on something you would enjoy doing in your life.

Or, you can wait for the crash in the real estate market and invest it there.

If interest rates go up you will be able to get a good deal with your 401k cash on a property that you can rent out for income. This requires some work, but rental income can cover most expenses and you will always have a place to live if worse comes to worse. Rental income also goes up with inflation.

I am not a professional investor, I just think you should enjoy your money. It is yours, you earned it.

Please listen to Phil’s Gang. You will learn a lot. Just saying. There is a lot of advice in this thread and more education is always better. I think things are going to get worse in the market in the Fall.

All here have to remember if you cash out your ira & you are under 59 1/2 you will pay the taxes as income + 10% penalty

What’s the penalty of losing 60% of it in the event of a stock market collapse like 08, then paying taxes to cash out? YOU cash out at the top and buy it near the bottom… same rule applies to most things relative to making money. Taxes are taxes… until the population decides as a whole taxes aren’t gonna be paid…. like the Boston Tea Party (which is not gonna happen too many people on the dole and free handouts nowadays.)

My favorite target, JNJ…the market dropped almost 300 points yesterday. JNJ closed at 168.12(down .14%)…ED closed at 74.96, up 0.74%…if one goes long on either, it will take quite a few years to reach normalcy in your dividends. PG up 0.97%. Makes no sense.

I don’t pay attention to the market currently…. aside from looking up quotes on stocks I mentioned previously here just to see where they are for reference….. after the collapse is in the news then I might look into it.

Sounds like a classic “panic and puke” that you’re advising. Then again, I’m not at an age where it would be advantageous to take anything out of my 401k or Roth. I’d have to wait at least another 35 years before even considering it. Maybe we all won’t even be around in 35 years. Who knows.

When the last crash happens, I thought back to <I>It’s a Wonderful Life</I> and asked myself: What would Mr. Potter do? That’s easy, he was paying 50 cents on the dollar to buy property. You can’t do that directly with your retirement money so I put it in REITs. Made good returns on the rebound. I expect this time around will be more of the same. Catch is, having the cash to act on it when it happens.

My father put money into a REIT years ago, I’m pretty sure the REIT had something to do with the medical industry. Last I talked to him about it, it was just barely below the value that he had bought in at. Put me in the skeptical column when it comes to REITs.

I advise you to have cash or ability to churn your investments when the buying opportunity arrives. If you don’t have cash to invest you don’t get the opportunity to make the returns.

I fell for the RE hoopla hopium in 2006 and bought into a $650,000 home. Within one year the price was tapping the brakes, then by 2008 that soft landing destroyed my job and down I went. I managed keep it until Jan 2012 and short sold it for 412,000. My credit was destroyed and was un/under employed for 11 years.

One thing about being underemployed is…. you definitely learn from it. You actually may end up wiser afterwards and richer.

“Dead Cat Bounce”

I got my first major Dow Jones sell signal(July 2021) since last Dow Jones major sell signal(January 2020). Obviously, take it for what it worth. Nothing regarding the stock market is ever 100% correct.

The biggest sign is politics… when it shifts, the market usually adjusts. Also the insiders are selling massive chunks of their stocks EVERYDAY…. not once a week, or month.

Funny how the entire media frenzy regarding “war on women” just disappeared. The media liars deserve so much blow back. They have literally aided the destruction of a country.

Most of the women I know are making far more money than the average man. They are also going on vacation far more often, Driving nicer cars and eating higher end food than the typical man.

Interesting, As an artist most of my clients are women, years back it was couples..

Women got all the money, Lol.

When I heard of the return of crazy bidding wars, I knew the crash was right around the corner.

This don’t mean squat when there isn’t election integrity ???

Good graph showing the cratering of existing home sales here:

https://tradingeconomics.com/united-states/existing-home-sales

Set it to 5 years, and JoeBama getting installed in January jumps right out at you.

The cognitive dissonance in the link Sundance shared is striking. Out one side of their mouth, they report on bidding wars and insane price increases…sure signs of a bubble. Out the other side of their mouth they make the non sequitur argument that it can’t be a bubble because there aren’t bad loan practices any more.

Housing bubbles exist for many reasons, the criminally negligent Fed-subsidized, loan practices of the early 2000’s were a factor then, but America has had housing crashes before that had nothing to do with the Greenspan/Bernake criminal negligence at the Fed.

Keep in mind that the 2008 crash was fed by $4 gas and a recession. People went under because they couldn’t make the payments on their fabulously overpriced McMansion. My closest friend of 30-years literally packed up his belongings, left the keys in the kitchen, and walked away after he lost his job.

We are at war, folks. Hopefully more of our neighbors start to realize this. I think if it keeps getting worse, and it probably will, DC is going to wish they had build a wall around the city.

Hokkoda: DC is surrounded by a wall of lies. The wall may be tall, but it has no foundation.

I quickly read this as a “wall of tires”. Winnie Mandela’s “necklacing ” provokes a terrible image.

Who will the sheeple hear the negative numbers from? In 18 – 24 mos when it can’t be denied it’ll be too late for the steeple as they will not have a choice as to whether or not they want to be shorn……if you’re not in government or contracted, you get a haircut???

The thing about inflation is that you don’t have to “hear the negative numbers” because you’re living it. You cannot go to the grocery store right now and not notice that you’re paying a lot more and getting a lot less. You can’t buy a house because large corporations are buying up inventory, inflating prices, and making it so you cannot afford to buy unless you mortgage your soul.

They can’t hide inflation. They can lie about it, but they can’t hide it.

I regard the current Fed rate since The Big 0 took office as a repeat of their prior criminal negligence prior to 2008. And they’ll try to do the same thing again. Only this time it will be worse.

I think it was on Twitchy the other day I saw a post where one of the *Clinton* economic guys was listing out how this time is different than last time and how those differences will make this one all that much worse. One of the big ones was deficit (not debt which is even bigger) as a percent of GDP: back then it was 3%, today it is 15%. I suppose I shouldn’t say big ones because the others were as bad or worse for individuals. But even Dementia Joe will notice when the interest on debt starts eviscerating what passes for a federal budget these days.

The one he didn’t really list is that The Fed doesn’t have tools to fix it this time. Japan found out you can’t really run negative interest rates for the banks. So when the recession hits they are stuck with 0% as a lower limit, but it won’t matter if there is nothing to buy.

My friend who manufactures lumber products said the bottom has dropped out. He said someone in the lumber business had a $900K box car of lumber that was now worth about $300K. Some product back to near run up prices. As he is in the business, he has had to buy thru the run up and now he does have stock that is worth less than when he bought it.

He says perhaps some reasons are some folks getting back to work and so aren’t doing as much house work as before. I didn’t ask how this will effect house prices. He did say he thought bounce and go back up some. He had hoped it wouldn’t drop as quick as it did. Will update as things go along.

Lumber never should have been as high as it was… it was a short-term scarcity brought on by logistical problems. Plenty of videos showing massive stockpiles at the Canadian border, waiting for processing into distribution.

It got scarce because school was ending, and we were beginning the summer home repair / construction / moving season. And many citizens want to get out of cities, to the exurbs, into new construction for a better quality of life. Especially if the government puts us in another lock-down.

Same thing going on with pool construction. People are not returning to traveling vacations, they are instead investing the capital in their homes as improvements and pools, preparing for staycations.

I agree, Relative to any lumber business during this mania…. they should have only bought what was already spoken for…. and paid for in advance.

Given the nature of JIT deliveries across all businesses these days, they might have been following your advice and still be stuck with massive losses.

Aside from a life of crime, are these guys competent at anything?

No

If you dig deep enough into Biden’s past and his old govt’ employees, speech writers, etc. They are truly a big Organized Crime outfit…. you would be surprised at the wealth he has surrounding him… that his employees have/had. They stay under the radar, but some were making hundreds of millions in Oil and gas Pipelines, etc. It’s the same for others, most notably Clinton’s, they line there old partners up as strawmen/strawwomen they are the ones who become Billionaires, but much of the cash is actually not theirs… it’s Clinton/Obama/Biden and Companies cash. That’s why when you see Obama say jump, or Clinton say Jump these big Companies do as they are told. Cheryl Sandberg comes to mind… she runs Facebook, Zuckerberg is just the Face of the Company.

And what an ugly, monstrous face it is.

Home prices will never crash. Blackrock will keep pumping the price up with funny money.

It doesn’t matter if real families can’t afford them; that’s actually the intention.

They will crash, just like 2008. Only worse this time as it will be accelerated by boomers all trying to cash out and heading for the exit at the same time.

Titler cycle. They turn em to rentals. Push the cities to suburbs. Drive the value to crap.

Sundance is correct. It has already begun.

I have been looking at houses on Zillow almost daily, as I am trying to figure out what state to move to and there are many houses that recently have had price reductions and many that are pre-foreclosures (including many Inns and B&B’s being sold as homes).

People weren’t allowed to work in many places and an estimated 30% of small businesses closed. How are these people supposed to pay their mortgage and property taxes? It takes time for the defaults to work their way through the system. It’s going to be ugly again.

We bought at the peak of the market before the last crash, foolishly believing it wouldn’t hit in the Puget Sound because of all the tech companies. My area has had low inventory and houses selling just days after listing (we were being invaded by locusts fleeing Seattle) but things have slowed considerably here too.

Zillow doesn’t know squat…very general, values are based on a market algorithm.

Bottom line…Blue States down, Red States Up…

Every house in my neighborhood and it’s perimeter has sold for the Zestimate or above. But that really has nothing to do with my point.

The point about the price drops is that the LISTING PRICE for many houses CURRENTLY FOR SALE have decreased in many states and preforeclosures are popping up. I save specific houses and get alerts. And I live in the PNW very blue state and prices and homes have been flying because our inventory is low but are steadying now.

That has absolutely nothing to do with Zillow. They are a platform that lists the sale price an owner puts his house on the market for. No different than if you went to a realtor’s website.

Also, your analysis is incorrect because the state I am seeing pre-foreclosures begin to pop up and price drops occurring in is Ohio (red). As I stated above, states that were locked down, which includes red states, are going to have problems.

“The average weekly share of homes for sale with a price drop passed 4% for the first time since September, another signal that the hyper-competitive housing market is cooling. Other indicators corroborate the slowdown: the share of homes sold over list price, the share of homes sold within a week and median days on market are all also either cooling off or plateauing.

Pending sales were up 11% from a year ago, but down 11% from the 2021 peak, and asking prices have been relatively flat since late May. Even amid this shift, sellers remain in the driver’s seat, as home prices continued to rise more than 20% from a year ago and the number of homes for sale sits 30% below the same time last year.

Asking prices are still high, but the share of listings with price drops is rising steadily and could soon reach pre-pandemic levels,” said Redfin Chief Economist Daryl Fairweather. “That’s an early indication that we are past the peak for this intense seller’s market. Buyers may begin to regain some negotiating power on properties that have been on the market for more than a week.”

Key housing market takeaways for 400+ U.S. metro areas:Data based on homes listed and/or sold during the period:

https://www.redfin.com/news/?p=72923

Don’t worry. Parents of anchor babies will be getting $250 in child credit monthly per child and $300 if they’re under 6. I know that’s not very much but they’ll be OK as long as they still get their mediCal and Calfresh, so again, please don’t lose any sleep over this.

negasht7: CA Gov. Nussolini still has more of our money to give away before he gets recalled.

I rent a room to a person who needs support staff. The evening staff is also in the union for SEIU local 99 for school special Ed assistants. They had speaker phone on for union meeting this evening. They were strategizing how to fight the recall. Newsome is great for first tier California welfare recipients aka LAUSD employees. How many of them are there? How many state-funded employees total? Their COLAs will be great if Newsome survives.

Retired: Not just the POCs, but the entire rainbow of diversity will be disappointed, not just by the elites, but, more fundamentally, by reality.

“people that are demoralized are incapable of assessing facts”

I could swear she must uh have taken and uh a public uh speaking course with uh and uh Gavin Newsom.

Like that turd Rahm said never let a “crisis go to waste”. I know this sounds brutal but the Stupid Party can capitalize on Human Trafficker Joes plan to make America a province of Red China. Dont help him,dont support any bills sucking money into “infrastructure “. Of course the Demonic Pedo DemCong will portray the weak kneed Repubs as heartless. Wage a counter Psyop. Oh who am I kidding? The Party of Capitulation will…..capitulate.

“You cannot have declining wages and massive inflation and expect the middle-class to survive”.

TPTB don’t want a middle class to survive and thrive. We did for a bit. They need us to think we ‘need’ government to keep us alive and that includes the money/salary/housing/health issues.

That is why, IMHO, there is such a massive push for control in almost every aspect of our lives. We have so many ‘slippery slopes’, the Vail resort organizations should be jealous.

The main ‘chart’ I look at, is my own personal bank balance. And that says it all. However, inflation and declining wages…what really gets my goat, is the “shrinkflation” tactics of these big multinational corps that sell stuff we need…

For example, my toilet paper holders (1994), in the bathrooms…have an inch of exposed roller now…I mean really? TP is made from recycled paper…how much does that cost to make?

I refuse to move them and put holes in my drywall.

Aggiegirl I so echo your sentiments, especially about the shrinkage of TP size. It’s not just that the existing hardware is too large, it’s also that the Globalist Multinational manufacturers have not cut the costs for the small sheet size. And we won’t even go into the reduced utility/ effectiveness of the smaller sheets………?

Same goes for ice cream (cant find a real half gallon anymore, now it’s 1.5L) or many bottled liquid food items (can’t find a real quart anymore, now it’s something less than 800 mL). But the price is higher.

Important info. Thanks, as always.

country is going Really wrong Direction just like it fauilure Obama years,

sure Because joe B administration are most people from Obama admins and Now CCP Big Tech are running The our country,

i can’t hardly wait 3’more years To pass with fake president America last joe B,

He is an worst president in Down history of America,

There’s this quote attributed to Bill Gates–true, apocryphal, false or whatever–that has been in the back of my head for weeks and I can’t shake it. Supposedly, he said the Covid vaccine is the, “operating system“.

So what if Gates actually said that and the next round of mandatory “vaccines” will turn us into happy little drones? What if it made intolerable economic conditions quite tolerable as the elites plundered what is left of the middle-class.

How else is the government supposed to keep us from rioting due to unacceptable conditions–shoot us all?

We still have the problem of the millions of people in this country who will sit in front of their tvs or computers and soak up every bit of lies about how great the country and economy are doing under the Biden junta even as their cupboards and bank accounts dwindle to near nothing and their house value plummets.

Remember the “summer of recovery” during the Obama years? I talked to people in my own family about how bad it was and how the government was just faking it and the response was always, well, the stock market is up and things are looking good in other places so it will get to us eventually. (Which it did – when Trump was elected!)

Obama years were the most miserable and impoverishing years ever…. and I had a job, most people around me were unemployed for 2 solid years…. People who always had a job before. Biden years may be worse than Obama years. So far I’d reckon his inflation is far worse, without the Excessive Govt’ handouts…. it would be worse across the board for people trying to survive and eat. Ironically, the handouts are causing large parts of the inflation though, when combined with shortages of workers because most are on Welfare. So the rest of us are paying the higher price for this BS, but what else is new?

Sorry, but I don’t think this analysis is correct. The reason the median wage has decreased YOY is because of the rebound (even if modest) of lower-wage jobs in retail/hospitality. There was a similar spike in “wages” last year when those jobs were lost. We would need an actual “apples to apples” comparison to get at the real numbers. The Federal Reserve Bank of Atlanta has a metric that reports median wages for those employed in the same job for at least a year and that data shows wages up about 3 percent since last year.

I agree with the broader premise but we need to be accurate about data.

You do make a good point. Also, is that in area covered by Atlanta Fed only…because wage discussions now have to be discussed regionally as well as by category.

One size fits all “national” statistics have never been good measures due to regionally driven economic environments, even in the best of times. Now that the demo-fascists have physically divided the country, the differences are even worse.

How about we skip last year and look at 2Q2019 versus 2Q2021?

A full Trump economy in its 3rd year versus a Biden/Covid economy in its 2nd quarter ?

https://www.macrotrends.net/2497/historical-inflation-rate-by-year

Zoom in on this graph so that you can see 2000-2020. The current spike cannot be explained by a return from covid because prices didn’t drop all that much YOY during covid.

On the flip side, before people get too carried away, current inflation is pretty mild historically. Not that I want a return to the double-digit inflation of the 70’s, but 5-6% sustained inflation is going to force the Fed to start raising interest rates. That’s a good thing, in my opinion. As a society, we are addicted to cheap money.

One-term President George HW Bush presided over 6% inflation in 1990 prior to his defeat in 1992. A little inflation to get rid of Biden/Harris will be quite welcome if we can get a handle on the election fraud.

The real inflation rate at the cash register is not 5-6%.

With hamburger flipper – entry level jobs on the rise and real jobs with growth on the decline, your assessment falls apart.

Gas alone is up 70% in 7 months locally… just went up another 10 cents yesterday, that’s ~ another 6% increase from where it was. Food is mostly higher, somewhere in range of 30%, paints are all higher, almost everything is higher. 5-6% is a BIG LIE.

They’ll just blame it on republicans and then propose some race/sex based tax. The media will cheer it and the idiots that vote for these people and consume mainstream media will eat it up.

Yes all true. However, there are fewer “Useful Idiots” as transparent Truth reaches a greater awareness everyday.

Corporatist, not capitalist. There is a difference

I recommend the average person who is not a sophisticated investor to invest in something as the Dow Jones Index. This way you are investing an average of 30-stock companies and not getting involved in having to “pick a stock”.

It is simply buying and selling an average Dow Jones price up or down.

If inflation is high one needs to invest, however if you are worried stocks are overvalued and realize that bonds are not not paying anything, the question becomes to put your money. One avenue is commodities which typically rise when there is inflation. If you consider this road it may be worth working with a financial agent who specializes in such.

Economic Sector Reports do not lie.

The losers are companies focused on domestic “production” capabilities, which means; skilled labor, blue collar, professional and white collar jobs being either lost or re-made at lower labor rates after job position consolidation or replacement by immigrant.

It also means very low numbers of domestic production related IPO’s, declining domestic capital investments = a REAL decline in GDP.

The US Labor Department so far has not gone completely into obfuscate mode…record quit rate with NO rentry plans, growing rate of Social Security Disability claims, early retirements beginning to climb again, etc.

ALL indicators of middle-class shrinkage and increased rate in growth of the Government created “INCOME GAP” via removing high middle-class paydays from the data set.

The objective is to rid the middle class (Main Street).

Correct as in the USSR. There is no middle class…it’s the Have’s…per graft or the lower class ie factory workers or poors.

In some markets the home builders may be skinned. In other markets we will see housing wealth go to “money heaven” but those surrendering it will not miss it as they voluntarily downshift their housing needs from the McMansions and enter retirement mode.

The first time buyers will benefit as will those looking to trade up.

Estimated that 3 million illegal aliens will have come into the USA by end of December 2021.

More draining of resources, more competition for jobs. And bringing in Visa workers to take good paying jobs from American citizens.

In my town this became very visible during obamination.

Middle class means Republican.

The middle class is being punished, hard and fast, for supporting Trump.

Poor people vote Democrat (or at least, support the Democrats. The voter turnout for Biden in Detroit was very low, but when all the mail-in ballots were added up, whaddaya know, Biden racked up a huge vote total).

The perverse reality is that a poorer America benefits the Democrats. Open borders is supplying the poor people required to justify a burgeoning bureaucracy. Obama handed out big raises to his bureaucrats during the 2009 recession; that had two huge consequences. Bureaucrat is now a synonym for passionate Democrat, and bureaucrats regard themselves as immune to the business cycle. Government workers expect to receive raises even during an economic depression. So sick, so dangerous.

How does this benefit the Republican Party establishment? The eternal question. It’s hard not to suspect that the GOP has become the longest-running, most elaborate hoax in American history.

1977 all over again.

1977…Interesting.

2 years before the Crap hit the fan with oil prices, foreign policy debacles…Iran …and Russia in Afghanistan.

Bright light i this was Ronald Reagan rising to power as a result…short term pain, long term gain..

The left has manufactured a number of crisis here. They are so stupid that they think a plan to fix it will be accepted by Americans. Their downfall will come from stupidity in that they can’t accept the great things that Trump did for the economy and working class. This makes them still believe that their methods will work.

More proof of their stupidity is not accepting the trend of minorities voting for Trump/Republicans in larger than ever margins. This has been proven and yet the left continues to want more immigration they think will vote for them.

I have to say that Trump should get more credit for frying the brains of democrats to the point they won’t accept reality.

A Correction as I have stated before…Home prices will soften considerably in blue states…yet will remain stable in Red States.

All of the Blue’s moving in…

Xiden loves it when a plan comes together.

This is what is called stagflation. It was something that happened during Carter’s admin. This is where the prices are high yet wages are low. It is very difficult to get out of yet there’s a simple solution. Just difficult to get it done.

First do the opposite of what Biden is doing. He immediately throttled our energy surplus. This made waves down the line beyond just the oil industry altho that accounts for a lot of money, jobs and future jobs and money.

Then other areas of business retracted because they saw that costs would increase due to the shrinking of the oil industry and then more and more places that were already hurting from the hysteric lockdowns but trying to recover. Some collapsed which accounted for other price increases and other’s retracted and there are some who are experiencing problem from some parts being in short supply.

The entire economy is shrinking and retracting. But the left loves that because then more people are dependent on government. And they plan more emergencies about other things they want to control.

2022 is important but 2024 will be vital or we are gone as a viable nation.

…stop mayorkas….Sundance…w a k e u p…..

Wake tf UP!

While I agree with the sentiment in the article, there is a mis-reading of the Table 2. The weekly average earnings have already been corrected for inflation. These figures are expressed in 1982-1984 dollars as indicated in the original Table 2 on the BLS website.

Of course, these numbers are quite concerning as the base comparison quarter was Q2 2020 the absolute trough of the shutdown. To see weekly earnings at basically at the same level in what should be relatively far along in a recovery reflects bad economic performance.

If we had experience real 6% negative growth in weekly earnings this would be an economic contraction that would be disastrous on a scale even MSM would have to lead with that story every day.

Well, they already stripped them of their right to vote (one woman, one vote, shall not be abridged), and it only took them 100 years, OR LESS.

They have taken away their voice, their bathrooms, their locker rooms, their spas, their place in the home, and in their children’s lives, and their sports.

What is left?