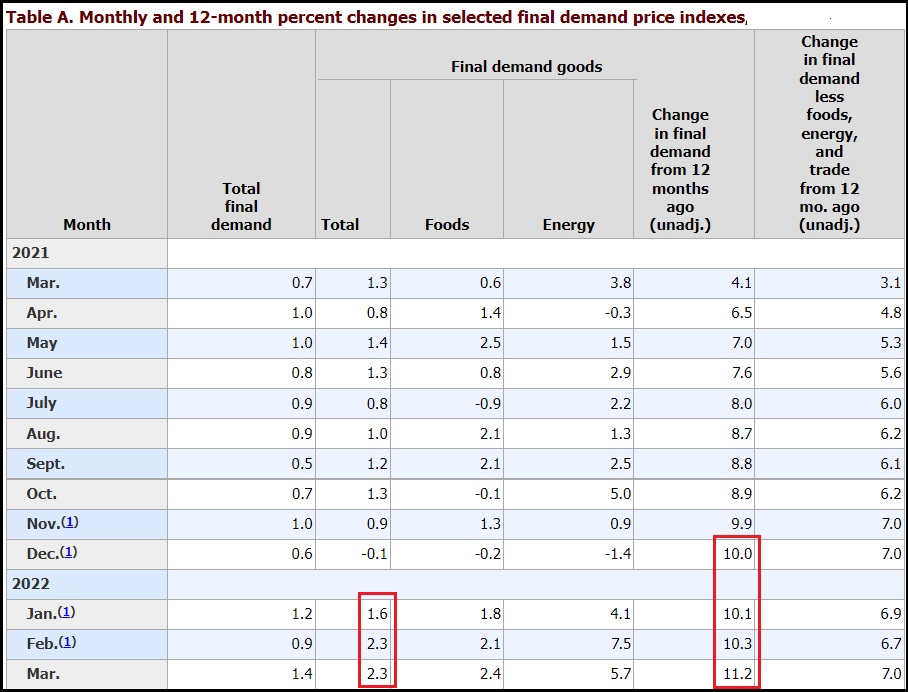

The “Producer Price Index” (PPI) is essentially the tracking of wholesale prices at three stages: Origination (commodity), Intermediate (processing), and then Final (to wholesale). Today, the Bureau of Labor and Statistics (BLS) released March price data [Available Here] showing a dramatic 11.2% increase year-over-year in Final Demand products at the wholesale level. This is the fifth consecutive month with the highest rate of inflation the PPI ever recorded.

The single month increase in wholesale prices of 2.3% was driven by inflation built into the supply chain at every level that shows up in the final wholesale price. Those price increases then get passed along to consumers along with the additional costs for warehousing, transportation and delivery. I modified Table-A (FINAL DEMAND) to take out some of the noise.

Wholesale prices of goods jumped 2.3 percent in March, and the wholesale price of food products jumped 2.4 percent. The total demand inflation compared to last year is 11.2 percent, the highest rate ever recorded since the PPI tracking was first started.

The total final demand monthly calculation (1.4%) is lower than the final demand goods (2.3%), because final demand services are offsetting. You may remember the discussion/analysis about prices beginning to stabilize after this month due to a contraction in demand for goods and services. I see support for that thesis within this data.

The three phases of wholesale product creation: (1) origination, (2) intermediate, and (3) final, cycle through the economic analysis in reverse chronological order. Roughly speaking, the flow of goods quantified is done in 30-day sequences. Final demand this month is comparing to final demand in March 2021. The intermediate demand goods this month will become final demand goods next month (April).

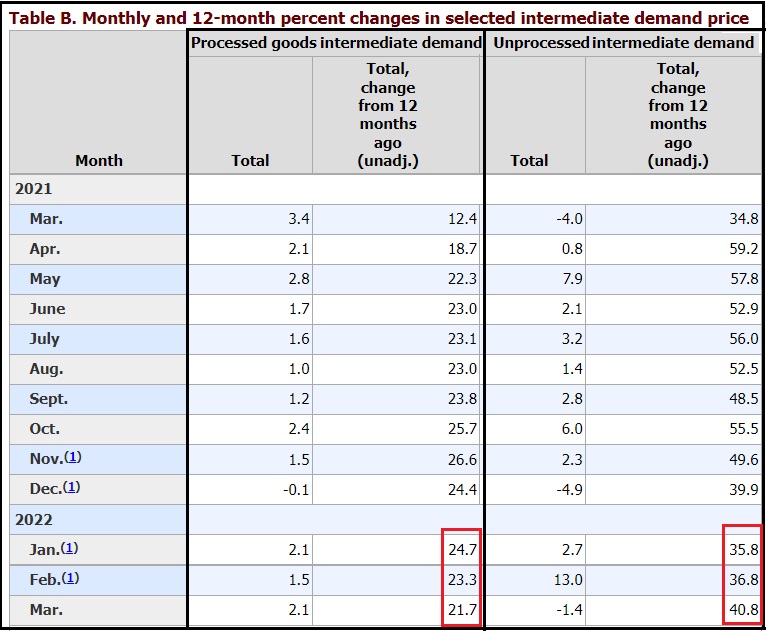

The rate of inflation behind this set of final demand goods is beginning to soften. See Table B, Intermediate goods. Again, modified to take out the noise:

While the yearly comparison for both processed and unprocessed intermedia goods is eye dropping, in the unprocessed intermediate demand goods, we are starting to see a lessening of monthly price increases.

In essence, prices have been rising so fast and for such an extended period of time, that we are now cycling through the rate of increase and starting to compare it to last year when the rate of increase was originally going high. As a consequence, the rate of price increase will likely lessen, even though the actual price may still keep climbing within the manufacturing process.

The price of raw materials, and the wholesale energy costs to process those materials into finished goods, are still rising. In addition to the consumer prices reported yesterday, this wholesale price data is showing the most recent increases (March) in fuel and transportation costs. For the next report these figures should now plateau.

♦ BOTTOM LINE – We have not yet reached PEAK INFLATION – However, the price increases from wholesalers to retailers are now at parity. The increased price of things coming into the supply chain are now at similar rates of increase when compared to the stuff on the shelves.

Inflation from field to fork is now fully matriculated and embedded in the total economy as a result of two massive price waves (July to October 2021 and November to March 2022). Those prices will never fall.

Highly consumable goods like food, fuel and energy will remain at approximately the price today for a period of around five months, then we will see the third wave kick in as the new higher harvest prices hit the processors in late summer.

The prices for non-essential durable goods, like cars, electronics, appliances etc. from this moment forth will now be determined by demand. Highly sought after goods will increase in price as more customers chase fewer products. However, ordinary or widely available durable goods will likely start to come down in price very soon as inventories climb because consumer spending has prioritized and dropped non essential goods from their shopping lists.

To put it more succinctly: The stuff we need will cost more. The stuff we don’t need will cost less.

Let’s Go Brandon

FJB

One of the stupid things MSM said was not to buy in bulk to keep your grocery bill down…

When does this end?

When we are serious about telling the government who is in charge.

When we start putting heads on pikes.

It is time we stop accepting the things we cannot change, and start changing the things we cannot accept. MAGA 2022

I think for the average person none of this has really sunk in. I think it has been one of these, “It will get back to normal soon”. There is way too much apathy and complacency and not near enough “pain”. There is way too much fluff and not yet enough “nitty-gritty”. There is too much Kamala cackle entertainment and Biden flub a dub giggle.

The Politicians are in their own World and it is their self-interest which is all that matters at this point. IMO, there has not been any accountability which has to be answered. I have come to the juncture until there is serious accountability, I am done with showtime.

I know lots of folks who think this is all still a temporary deal. They refuse to accept reality. I cannot help them, though I’ve tried. These same folks also think there will be plenty of food from now on. Refuse to believe the combination of circumstances will create havoc with food supplies as we move forward.

I don’t see food shortage being a factor here in the United States. I don’t know of one farmer planning to plant one less acre.

Irrigation could eventually be an issue here in California. We call it the Political Drought. California has plenty of water, however, it is so mismanaged it is criminal. The same for California forestry.

The “Big Hurt” I see coming is energy, inflation, housing and stock market crash.

Maybe, The housing crunch will be an interesting one.

Around here. Greater Vancouver B.C. the demand is extremely high, and many wise individuals late last year locked in 5 year fixed rates at little more than 1.5%

So a big hurt there may be a while off.

Stocks though are an interesting one.

Canadian Banks ( usually a pillar) are way down this month.

That may be a foreboding of things to come.

Many agree that discretionary spending will be hammered. Devastated even.

Cheers! Your insights are always appreciated.

Thank you

I bought my house a year and a half ago at a ridiculously low rate and it has already appreciated by 25%. I’m in a VERY high demand area.

As to paraphrase Ace of Spades today, things won’t change until educated white wimmin winos notice that wine and “Live, Laugh, Love” wall art are getting too pricey and have to borrow more money from their driving mocassin/REI hatted/stubble faced/scalped male partner’s bank account.

Bon mot.

When it all collapses.

They’re only getting started.

When Christ returns.

When a political party is formed that is TRULY conservative, operates exclusively for the benefit of America, vets and filters their candidates, adheres to a set of moral conduct, etc. NONE of the current Democrat, RINO and few Republican office holders could pass the vetting process. Until then, PAY DEARLY FOR VOTING IN TRUMP AS POTUS!

Any political party once formed is a monster that lives to feed itself.

“Feed me, Seymour.”

It ends when the Federal Reserve is handcuffed by disallowing this engine of inflation to purchase more assets.

Yes, it really is that simple.

It will end when Democrats are destroyed and no longer in a position of power in our government.

How could it get better with Democrats and Rino’s goal is to destroy?

Just about everyone I know believes this all gonna go away in a few months.

Dream on.

Say it ain’t so, Joe.

No further comment necessary.

It is astounding how accurate Sundance is.

Every. Step. Of. The. Way.

It would be natural to wonder why the government agencies can not figure this stuff out.

They have abandoned any pretense of purpose other than politics.

They have it figured out completely and have decided that it is the price we are to pay for their “green” society. We haven’t seen the final bill yet as we are no where near their destination.

Exactly. This is all on purpose. They hate us.

I don’t think they “hate” us as much as it is we are “In their way”.

I really wish they could pool their billions, buy some parkland somewhere, build pretentious houses, virtue signal to each other, and leave us alone! They can call it Utopia for all I care. I would even donate a national park if we could put an electrified fence around it so they would never escape.

Government agencies probably come here to find out what’s really happening, and then adjust accordingly.

Unfortunately, their adjustments are to change instruments of torture, instead of making things right.

Their cause is hopeless as they do not understand those that oppose them, nor would they deign to even attempt to do so in order to defeat us.

Likewise for God.

They have it figured out…to the penny. They Do NOT Care about us or how much things cost. It does NOT affect them the way it does us.

They can lie about Anything and Everything and are NEVER held accountable….So they Do NOT Care!

“Accountability” is the big deal. Until and if ever when, it is just further destruction.

Yes. Imagine a nation of laws where the leaders a) were accountable under the law and b) spent their time ways actually improving the lives of its citizens.

Hypothetically, if I were the “Pretender in Chief” and I was bent on 666 (I mean bbb), I would:

Blame everything on Putin.

Drive up inflation so that, even if there are no food shortages in the US, the Middle Class will not be able to afford that food.

Open the borders and allow millions of starving people to flood into the country. Put them on planes, trains, and buses to spread them out across the land.

Pay farmers not to plant. Sell US farmland off to foreign interests.

Accidentally, burn down the fertilizer plants. Make the price of fertilizer cost prohibitive by blocking natural gas exploration and production.

Limit meat processing plants with over-regulation. Sell US produce overseas. Insist that Covid (I mean Bird Flu) be tested with a faulty test like PCR. Then, kill all of the birds immediately. Do not wait for the test results of an alternate, more reliable test.

Make an Executive Order raising the fuel content of ethanol to 20%. Heck, push for 50%. Insist that it will decrease the price of fuel and save the planet. That should destroy more of those gas cars.

Use increased Geo-engineering. Get planes up there 24-7 dumping aluminum nano-particles to block out the sun. Use Haarp weather control to decrease the rainfall in the Corn Belt.

And that is just the beginning.

We cannot rebuild unless we first destroy everything./s

Inflation reduces the real value of govt obligations and in turn allows for more debt. Do not think our current situation is by accident.

It only allows for more debt as long as you are the World Reserve Currency.

Otherwise, you can print Cuban, Venezuelan, and Zimbabwean money all you want but, no country will buy that money debt because it has nothing backing it. It is an IOU with no backing.

Because the US froze the Russian Central Bank 1 month ago, we lost World Reserve Currency standing.

Only an idiot would trust us in the future.

No country will buy our debt.

All of it intentional. The pain is intentional. The collapse is intentional. I have a fantasy I would love to see which would tell we are finally waking up……I want to see an event where FJB and Kammy are introduced and everyone in attendance turns their back to them…..silent….no expression. Can you imagine the message it eould send to the nation and the world? The sheer disgust and revulsion I have for DC is reaching Olympian levels.

My fantasies (there are several):

I have a million iterations in my mind…

86/46 because he isn’t

I think you have Joe Biden’s IQ bracketed.

Love the use of Alcoholic’s Anonymous motto (kind of/sort of), with a MAGA twist!

Am example of the stuff I don’t need and won’t be buying for the foreseeable future: Aldi has pots of tulips, Easter lilies and hyacinths for $4.99 today. I skipped on them and bought vegetables to eat instead. Same thing with flowers at the local nurseries. I feel sorry for the growers but I’m being very thoughtful with my money.

I did get some free flower and vegetable seeds from a little seed library, though. Free is a good price.

Except the flower growing businesses are small , mom , pop businesses I will support them and flowers make me happy , which is sorely missing in this world.

some flowers are edible and nutritious too!

Edible Flowers: Beautiful, but Are They Nutritious? – Selene River Press

I bought lots of sunflower seeds. Flowers make me happy too.

Sunflowers make birds happy when the seeds ripen. This makes the burden of bird feeding more bearable.

Thank you….some nice plants for the yard or garden make life much more enjoyable too 😀

Bravo!

ALDI? French conglomerate owned business.

11.2 isn’t that much.

Joe Biden’s IQ is 6 times that.

Does this suggest cars/trucks, appliances will go down or up in price? I figured they were essential??

How about real estate? Homes prices?

Hotels and airbnb rates?

Airplane prices?

The continuance of consumer goods depends for its existence on the maintenance of capital goods.

Inflation is destructive of capital.

Therefore, these consumer goods you list (and housing is a consumer good!) will A.) become more costly to produce, B.) be offered at the same price by replacing the existing components with cheaper substitutes or C.) be completely dropped from production.

Whichever way the cat jumps, tomorrow will become more nasty, brutish and short.

Gentlemen, we are on the threshold of Hobbes’ jungle.

I am working on MAGA 2022, Sundance! Thank you for you and the CTH team. I can’t tell you how much I’ve learned from you and how much I appreciate you all.

It was entirely “accidental” that someone shared one of your posts back in 2016 and I’ve been “hooked” ever since! I share your posts far and wide!

I am adopting your motto as above:

It is time we stop accepting the things we cannot change, and start changing the things we cannot accept! I’m there.

Employment in the stuff we don’t need is going to start falling. Except for government as usual, we’re paying for more of that no matter what.

STOP PRINTING DOLLARS

Stop running a deficit, which fuels the printing of dollars.

Do you see the problem?

Everyone wants a free lunch, which Uncle Sap promises will be provided in limitless quantities.

They can’t.

Great summary of our current dilemma, crude is the wild card in the mix. There is no shortage of “experts” calling for $150-$200 barrel.

“Experts” my right eye! A word I’ve come with to despise.

Dunning-Kruger Effect

–a type of cognitive bias where people with little expertise or ability assume they have superior expertise or ability. This overestimation occurs as a result of the fact that they don’t have enough knowledge to know they don’t have enough knowledge.

Yep…sums it up perfectly.

So this Dunning-Kruger test is something that is used to qualify for government service?

I actually believe it’s the only test that they have to take. Or so it seems.

“Experts” my right eye!

My definition of an “expert”…….

…..an “ex” is a has-been, and a “spert” is a quick dribble.

I cut the cable today….and I’m quite Proud of myself too!!

Good for you! I did that around that time there was a Marxist in the White House and I couldn’t stomach the nonstop propaganda any more.

Well done!

Welcome to the club! I cut it the cord in 2005!!!

Life will be fun again!!! ⛱️ Go to the beach!

We got rid of our 12 years ago.

All of my married kids live without it just fine.

More and more seem to be doing this, so glad to see it.

👏 👏 👏 You won’t regret it. We cut ours almost 6 yrs. ago, and you can find most of you favorite shows on YouTube by doing simple searches.

but doesn’t that kinda mean you are giving $$’s to the Google Eye of Sauron instead of Concast?

But BOOKS might be the alternative!

Roku for streaming.

Yes!

And then I got Philo! 20.00 month. All the DYI shows,yeah..Hallmark,food channels…and a lot more!

No news channels and no sports channels. Makes it cheap.

Weather Nation instead of flakie fake Weather Channel….

Ah….life is so much better!

Shockingly exhilarating, isn’t it?

I actually feel a lot better! Thanks!!

😁👍

Good on ya!

We did as well over a year ago and have not regretted or missed it at all. It’s also great saving $180 a month!

What’s a cable that’s being cut ?

I shut down the cable tv, “cutting the cable”. Even worse, I quit smoking three weeks ago! Next I’ll settle down and get married…….for the 3rd time! 🙂

Great news… 👍

Excellent Rick, just excellent.

If the reporting body BLS is part of the us government it is lying and reality is far more than BLS gives out. 11.2% inflation probably over 25%.

Like the FBI, DOJ, CIA, FDA, CDC, NIH and the DHS the BLS is nothing more than a department of the Democrat Party!

Like FJB polling numbers in the 40s. It is all lies. Made up stuff. If a real poll were taken brandon might get 8%.

I suspect THIS is the number that “Circle-back Psaki” was hinting at last week…the inflation numbers were definitely bad but these are the “Worst Ever Recorded”!

Joe’s approval ratings continue to plunge as everyone is now feeling it at the gas pump and at the grocery store. And as people start to plan their summer vacations and/or projects around the house and realize they can’t afford either one, the anger is going to go nowhere but up – and Donald Trump has been gone too long for anyone to believe it’s his fault while the Putin narrative is sinking faster than Joebama’s polling numbers.

We are in dangerous territory here, Treepers…they cannot let the elections happen in November because they know that they will be absolutely destroyed at the polls, even with all the fraud and phony ballots!

“LORD, we do not know what to do. Our eyes are on You.” II Chronicles 20:12

Just use a little commonsense. Why would Putin and Xi want to destroy America? They want America to be able to buy their stuff. You can’t expect to get any money from a “poor man”. Biden and company want Control of the people and in order to accomplish control they have to create dependency.

War is about taking real estate and resources.

Quinnipiac poll (for whatever that’s worth) has Hispanic support for Geriatric Joe a 26% only.

Now that’s one poll I’d like to believe. Cue heavy drinking by the DNC.

Was the AI Dominion Algorithm polled? That’s the one that matters.

socialism Joe Biden and Democratics stop destroying our country,American are can’t take it anymore,

people get Rid of every Democratic’s coming Nov 2022 Election,

The only way to stop Joe Biden and Democrats to stop destroying American is to destroy Joe Biden and Democrats. You candidly don’t think they are going to stop doing what is working for them do you?

I knew the communists would place the blame either on putin or Trump:

https://www.breitbart.com/politics/2022/04/13/white-house-refuses-to-take-responsibility-for-historic-inflation-we-had-to-spend-trillions-to-prevent-economic-spiral/

“White House press secretary Jen Psaki blamed inflation on the pandemic, snarled supply chains, and Russian President Vladimir Putin for forcing energy prices higher by invading Ukraine.”

So how many ignorant Americans actually believe this crap?

most of them?

Any and all Libtards. Why would you expect anything else from those who lack; Rationale, Judgment, Commonsense?

It’s jus Transitory Flation folks

None of these economic disaster reports seem to bother the Democrats at all? It’s like every disaster is Teflon!

“[T]he the yearly comparison for both processed and unprocessed intermedia goods is EYE DROPPING…”

Eye popping…jaw dropping??

Does the data make you drowsy??

eyes popped out so far that they dropped onto the keyboard

Finally! My 1970s WIN and SIN buttons are appreciating.

(“Whip Inflation Now” and “Stop Inflation Now”)

Stop Inflation Now=SIN.

This is why the Federal Reserve continues to inflate—Stop Inflation Now is a sin!

Worst. President. Ever.

That is incorrect. For Biden to be the worst, he’d have to be a legitimate president and not the figurehead of a coup.

The worst is still Obama and all the same people behind him are really calling the shots now.

The Seven Stages of Empire

Historically a civilization lasts approx 250 years, they have always collapsed for the above reasons except for being invaded.

Breaking!

“According to preliminary information, the flagship of the Russian Black Sea Fleet, the cruiser Moskva, was indeed attacked by the Neptun missile launcher from the coastline between Odessa and Nikolayev. The missiles struck the port side, causing the ship to roll heavily. The crew of about 500 were evacuated after the threat of detonation of the ammunition. The buoyancy of the cruiser was made difficult by the sea weather conditions. As a result of all the cumulative factors, according to preliminary information, the cruiser sank.”

https://southfront.org/breaking-russian-black-sea-fleets-flagship-moskva-cruiser-experienced-explosion-of-ammunition-serious-damage-sustained-crew-evacuated/

Nothing Bothers Joe

This is proof of how the government manipulates the numbers, in order to fool the public. Overall CPI does not even approach any of the individual numbers.

When he gets too loopy to be useful, his wife will stick him in a home.

He’ll eat pureed food the rest of his short life while his wife lives it up on his crooked money.

First off the Republicans need to develop a message explaining why all this is happening then every Republican should be getting in front of any camera they can find and deliver that message. But what have we heard? Crickets, not a word from any of them. I guess they are too busy raising money for their reelection. It’s going to be up to US to put a stop to this insanity – and waiting for the 2022 election won’t get it done because they are already planning on the next wave of COVID, Bird Flu or whatever to go to mass mail in ballots and another steal.

I remember the Jimmy years, dad was in the middle of building a house and could not sell it with 18% mortgage rates.

It all fell apart from there too.

Hard/bad times for most/many of us. I remember it well. Government cheese, anyone?

And the 2,000 pound gorilla in the room is the US dollar, whose ongoing decline will further stimulate inflation. Logically, we should soon arrive at a point where the dollar is no longer accepted by merchants– and we all know what lies on the far side of that particular cliff.

Idiot Gov.

Kamala weighs in:

……..“I acknowledge one must acknowledge that prices are going up, and that people are working hard and, in many cases, are worried about whether they can get through the end of the month and make it all work,” Harris said.

What I can say is that people deserve to know that their president, that our administration, is concerned enough to do something about it, so that is what we are doing,” she added.”……

vid at link

https://www.thegatewaypundit.com/2022/04/listen-kamala-harris-brilliant-answer-asked-biden-admin-combat-inflation/

Idiot.

Always ask when purchasing something now…..

Is this a need

Or

Is this a want

If it is a want…..

Don’t buy.

Let’s Go Brandon.

Another 1st

Interesting little fun fact for my fellow treepers. This morning my daily cup of coffee cost me exactly 11.2% more than it did yesterday.

Hard to predict how high this inflation can go. People are already broke so to cause a great crisis much less is needed than a decade or longer ago. Now, it is more likely the government “lose” control of the economy than they can reverse the damage. They give the illusion they control it and to that extent they have been able to keep people relatively at ease. But if people panic, the Fed will discover how destructive the invisible hand could be to the arrogance and manipulation they thus far have been able to maintain. We have a few ceilings to reach as precedent: Wiemar Republic, Zimbabwe, Venezuela. One thing for sure, Deep State will not make it pass that collapse–they stay behind, buried under the ruins.

This will correct itself when, and only when, there are severe consequences for corrupt politicians. But as long as the democommie protection service (aka FBI) is still with us, it won’t happen. Corruption has ruined the great experiment.

Well, the hubs and I did our own inflation hedge today. We paid off our mortgage. We had a bunch of money laying around in our checking account, can’t earn any decent interest on it at all, didn’t want to invest in the market and buy at the highs, etc. So we decided to plow it into the house and eliminate our mortgage debt. That’s better to me than letting this runaway inflation decrease the value of the money sitting in our accounts.

Beware, you lose your mortgage exemption and they will tax you to the max depending upon where you live.

Best to have a small mortgage and low payments in exchange for the mortgage exemption(depending on where your located).

Check it out to find out what your local property tax rates will go to before they do it to you and make a judgement from there.

My Truck driver Grandson was home for his mandatory rest time and he brought 75 lbs of Rice and a couple of containers of the survival food. He and other truckers noticed that a lot of their normal food runs have been canceled. ie:chickens. Be prepared. Maybe our Republicans will grow a pair but don’t count on it.

Listen closely and you hear, you don’t need a house, a car, a 40-50 hr wk job/career.

Somebody working awfully hard against the American Dream, no?

Pretty much all plastic, wood and paper commodities are going up another 4-8% in April and May.